How to Set Up Business Credit From Scratch (Step-by-Step for New Business Owners)

Business Credit Setup for Beginners: How to Start the Right Way Most new business owners don't know their business can have its own credit score. Separate from your personal credit. Built under your business name. Used to get funding, credit cards, and trade lines — without always relying on your personal SSN. That's what business credit is. And if you're starting fresh, this guide will walk you through the exact setup process — step by step. No fluff. Just what actually matters.

BUSINESS CREDITBUSINESS FUNDING

Douglas G. Marsh

5/21/20266 min read

Why Business Credit Matters More Than You Think

When you apply for a business loan or a business credit card, lenders don't just look at you. They look at your business.

They want to see: Does this business have its own credit history? Does it look like a real, established company?

If your business has no credit file, no history, and no credibility — most lenders will either deny you or ask for your personal credit and a personal guarantee. That means your personal finances are on the line.

But when your business has its own credit profile? You have more options. Higher limits. Better approval chances. And you protect your personal credit at the same time.

That's the real reason business credit setup matters for beginners.

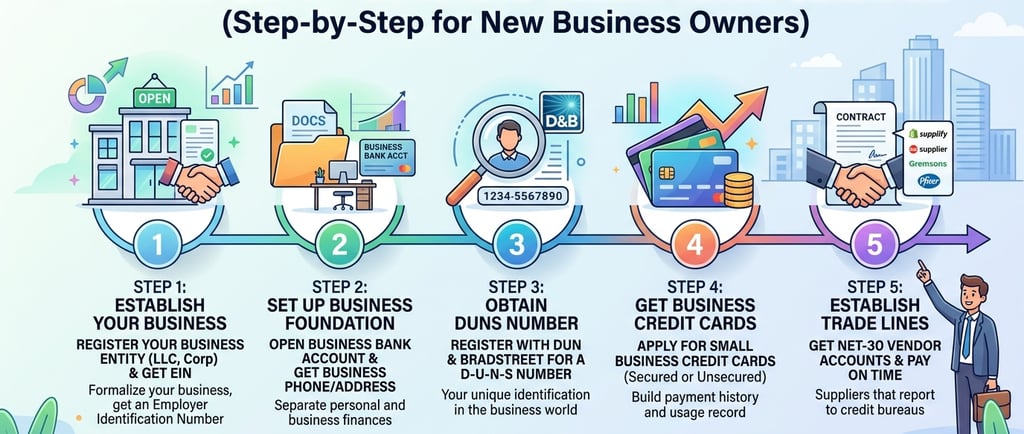

Step 1: Form a Legal Business Entity

This is the first and most important step in any business credit checklist for a new business.

You cannot build real business credit as a sole proprietor using your personal name. You need a legal business structure — most commonly an LLC (Limited Liability Company) or a corporation.

An LLC separates you from your business legally. It gives your business its own identity. Lenders, vendors, and credit bureaus treat it as a real business — not a side project.

If you haven't registered your LLC yet, that's where you start. Go to your state's Secretary of State website and file the paperwork. Costs vary by state — usually between $50 and $500.

Once your LLC is formed, you have the legal foundation to start building business credit.

Step 2: Get Your EIN (Employer Identification Number)

Think of an EIN like a Social Security Number — but for your business.

It's a 9-digit number issued by the IRS. It's free. And it's required to open a business bank account, apply for business credit, and file business taxes.

You can apply for your EIN at IRS.gov in about 5 minutes. It's issued immediately online.

This is one of the most important steps in any business credit starter guide for an LLC. Without an EIN, you can't separate your business identity from your personal one.

Once you have your EIN, use it consistently — on applications, bank accounts, and with vendors.

Step 3: Set Up a Professional Business Address and Phone Number

This sounds small. But it matters more than most beginners realize.

Lenders and credit bureaus verify your business information. If your address is a personal home address that doesn't match your LLC registration — or if you don't have a dedicated business phone number — it can raise red flags.

Use your registered business address. Get a dedicated business phone number. Even a Google Voice number works at the beginning.

Make sure your business name, address, and phone number are consistent everywhere — your website, Google Business Profile, and any applications you submit. This consistency is called NAP consistency (Name, Address, Phone), and it builds trust with lenders and credit bureaus.

Step 4: Open a Business Bank Account

You need a business checking account in your business name before you can do much else.

This is non-negotiable. It shows lenders your business is real and operating. It separates business income from personal income. And it's required by most lenders before they'll even review your application.

Open the account using your LLC documents and EIN. Many banks offer free or low-fee business checking — Chase, Bank of America, Mercury, and Relay are popular options among small business owners.

Once open, run your business transactions through it. Deposits. Expenses. Everything. The longer your account history, the better it looks when lenders review your business bank statements.

Step 5: Open Your Business Credit File

Here's something many beginners don't know — your business credit file doesn't open automatically.

You have to take steps to open it.

The three main business credit bureaus are Dun & Bradstreet, Experian Business, and Equifax Business. Each one tracks your business credit separately.

To start, go to Dun & Bradstreet's website and get your D-U-N-S Number — it's free and it opens your file with D&B. This is how you officially open a business credit file and start building a business credit history.

Experian and Equifax build your file automatically once vendors and lenders start reporting your payment activity. So the sooner you start getting accounts that report — the sooner your file grows.

Step 6: Get Starter Vendor Accounts (Trade Lines)

This is where most beginners get stuck. They want business credit but don't know how to get the first accounts.

The answer is starter vendor accounts — also called net-30 trade lines or vendor credit.

These are suppliers and vendors who will extend your business credit on net-30 terms. That means you order products or services now, and pay within 30 days. They report your payment history to the business credit bureaus.

Some well-known starter vendors that report to business credit bureaus include:

Uline – office and shipping supplies

Grainger – industrial and safety supplies

Quill – office supplies

These vendors are known for approving new businesses with little to no business credit history. The key is to pay on time — every time. That payment history is what builds your business credit score.

Getting 3–5 of these vendor accounts reporting on-time payments is a strong foundation for your business credit basics as a small business.

Step 7: Apply for a Business Credit Card

Once you have a few vendor accounts reporting, you can move toward a business credit card.

A business credit card gives you a revolving credit line — meaning you can use it, pay it off, and use it again. It also adds a different type of credit to your profile, which helps your business credit score grow faster.

Start with cards that are easier to get approved for with a newer business — cards like the Divvy Business Credit Card, Brex, or Sam's Club Business Mastercard are often accessible for newer businesses.

Use the card for regular business expenses. Keep your credit utilization — that's how much of your limit you're using — below 30%. Pay on time every single month.

This behavior builds a strong business credit profile over time.

Step 8: Monitor Your Business Credit

Building business credit is not a set-it-and-forget-it process.

You need to check your business credit reports regularly. Look for errors. Make sure vendors are actually reporting your payments. Confirm your business information is accurate across all three bureaus.

You can monitor your Dun & Bradstreet profile at dnb.com, Experian Business at experian.com/business, and Equifax Business at equifax.com/business.

Catching errors early can save you from problems when you apply for funding later. A wrong address, a missed report, or an error in your file can hurt your approval chances — even if you've been doing everything right.

Common Mistakes to Avoid as a Beginner

A lot of new business owners make the same mistakes. Here's what to watch out for:

Skipping the LLC step — sole proprietors can't build true business credit

Using personal info instead of EIN — always use your EIN on business applications

Inconsistent business information — your name, address, and phone must match everywhere

Not monitoring reports — errors go unnoticed and cause problems later

Giving up too early — business credit takes 6–12 months to build properly

This process is not fast. But every step you take now is setting up your business for better funding access later.

How Long Does Business Credit Setup Take?

For most new businesses, a basic credit profile takes about 3–6 months to establish.

Getting your first business credit card or working capital loan approval usually requires 6–12 months of solid payment history.

The key is starting now. Every month you wait is a month of credit history you don't have.

FAQ: Business Credit Setup for Beginners

Can I build business credit without using my personal SSN? Yes, in many cases. Starter vendor accounts and some business credit cards use your EIN and business information, not your personal SSN. But some lenders — especially for larger loans — will still ask for a personal guarantee.

Do I need an LLC to build business credit? An LLC is the most recommended structure. It separates your personal and business identity legally and professionally.

How do I open a business credit file? Start by getting a free D-U-N-S Number from Dun & Bradstreet. Then open vendor accounts that report to business credit bureaus. Your file grows as payment history is reported.

What credit score does my business need to get funding? It depends on the lender. For most business credit cards and vendor credit, lenders look for a Paydex score of 75+ (D&B). For larger loans, they want a history of on-time payments across multiple accounts.

How many vendor accounts do I need before applying for a business credit card? Most experts recommend 3–5 reporting vendor accounts before applying for your first business credit card. This gives you enough history to get approved.

Start Building Your Business Credit the Right Way

Business credit setup for beginners is not complicated. But it does require the right steps in the right order.

Form your LLC. Get your EIN. Open a business bank account. Start your credit file. Get vendor accounts reporting. Add a business credit card. Monitor everything.

That's the real business credit checklist for a new business. Follow it, stay consistent, and your business credit profile will grow.

If you want expert guidance — someone who can walk you through this process, help you identify the right vendor accounts, and position your business for real funding — Altopex.com is here to help.

We work with US small business owners every day to build strong business credit and access the funding they need to grow. Reach out and let's get started.