Business Credit Basics for Small Business: The Complete Starter Guide

Learn business credit basics for small business. Build a strong credit profile, set up your LLC credit file, and access real funding step by step.

BUSINESS CREDIT

Russel

5/23/20268 min read

Most Small Business Owners Skip This Step

You started your business. You got your LLC. Maybe you even opened a business bank account.

But here's the problem most small business owners run into fast — when it's time to get funding, lenders look at something most people have never built: a business credit profile.

No business credit means no access to business credit cards, trade lines, or working capital loans. It means lenders either deny you or fall back on your personal credit. And that puts your personal finances at risk every time your business needs money.

The good news? Business credit is something you can build. From scratch. Step by step. Even as a brand-new business.

This guide covers the full business credit basics for small business owners who are just getting started — or who realize they've been doing it wrong.

What Is Business Credit and Why Does It Matter?

Business credit is a separate credit profile built in your company's name, not yours personally. It's tied to your business name, your EIN (Employer Identification Number), and your business address — not your Social Security Number.

When you build business credit the right way, your company becomes a separate financial entity in the eyes of lenders, suppliers, and credit bureaus. That means:

You can get approved for funding based on your business profile

Your personal credit stays protected

You can access higher credit limits over time

More lenders and vendors will work with your business

This is why business credit setup for beginners is one of the most important steps any small business owner can take.

Think of it this way. A business with strong credit looks established and trustworthy. A business with no credit profile looks invisible. Lenders don't fund invisible businesses.

Business Credit vs. Personal Credit: What's the Difference?

Many small business owners make one big mistake early on: they mix personal and business finances.

Personal credit is tied to your Social Security Number. It tracks your personal credit cards, mortgages, car loans, and other personal accounts. Your personal credit score ranges from 300 to 850.

Business credit is different. It's tied to your EIN. It tracks business accounts, vendor relationships, and business loans. Business credit scores work on a scale from 0 to 100 (on the Paydex score from Dun & Bradstreet, for example).

When you apply for a business credit card or loan using your SSN, lenders run a personal credit check. That hurts your personal score. It also means any business debt shows on your personal file.

But when your business has its own credit profile, lenders check your business credit. Your personal score stays separate. This is how real business owners protect themselves financially.

Business Credit Checklist for New Business Owners

Before you start applying for any business credit, you need the right foundation in place. Here is a simple business credit checklist for new business that covers the essentials:

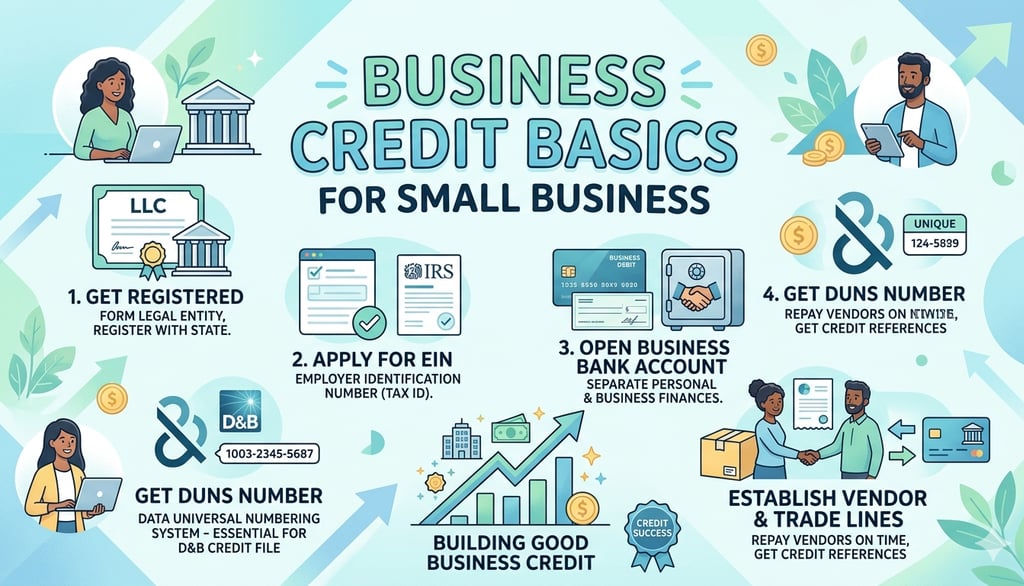

1. Form Your Legal Business Entity

You need a registered business — an LLC (Limited Liability Company) or Corporation. A sole proprietorship won't cut it for serious business credit.

An LLC separates your personal assets from your business. It also lets you open business accounts, apply for an EIN, and start building a credit file in your company's name.

If you haven't formed your LLC yet, that's your first step.

2. Get Your EIN (Employer Identification Number)

Your EIN is your business's tax ID — like a Social Security Number, but for your company. You get it free from the IRS at irs.gov.

Every lender, vendor, and credit bureau uses your EIN to track your business. Without an EIN, your business credit profile simply doesn't exist.

3. Open a Dedicated Business Bank Account

You need a business checking account in your company's name. Use it only for business income and expenses. This separation is something lenders look for when they review your business.

Many banks will check how long your account has been open and your average balance. A well-maintained business bank account adds credibility to your profile.

4. Get a Business Phone Number and Address

Your business needs a real, listed phone number and a professional business address. These get checked when you apply for business credit.

Listing your business phone on sites like 411.com and using a consistent address (not a P.O. Box) shows lenders your business is legitimate.

5. Set Up a Professional Business Website and Email

Lenders actually verify this. A business without a website or with a free Gmail address doesn't look established. Get a domain-based email like yourname@yourbusiness.com and set up a simple website.

This is a small step, but it's part of how lenders and vendors check fundability — the overall picture of how ready your business is to receive credit and funding.

6. Register With Business Credit Bureaus

The three main business credit bureaus are Dun & Bradstreet, Experian Business, and Equifax Business. They track your business credit activity separately.

For Dun & Bradstreet, get a D-U-N-S Number (free at dnb.com). This is a unique nine-digit number that identifies your business and is required by many lenders and government contracts.

Business Credit Starter Guide for LLC Owners

If you have an LLC and want to start building credit, here is the step-by-step process that works.

Step 1: Open Your Business Credit File

Getting your first business credit account is the hardest part. No credit history means most lenders won't approve you yet.

The solution is to start with vendor accounts — also called net-30 accounts or trade lines. These are accounts with suppliers who let you buy products on credit and pay within 30 days.

The key is finding starter vendors who report to business credit bureaus. Examples include:

Uline — packaging and shipping supplies

Quill — office supplies

Grainger — industrial and safety products

When these vendors report your on-time payments to the bureaus, your business credit file starts building.

Step 2: Build a Payment History

Pay every vendor account on time — or early. Your payment history is the biggest factor in your business credit score.

On the Dun & Bradstreet Paydex scale, paying on time gives you a score of 80. Paying early can push your score to 90 or even 100. That is the score range that opens doors to better credit terms and more funding options.

Even two or three vendor accounts, paid consistently, can start building a solid credit profile within 90 to 180 days.

Step 3: Add Business Credit Cards

Once you have a few months of trade line history, you can apply for business credit cards that report to business bureaus.

Look for cards that don't require personal guarantees (once your credit is established) or at least report to business bureaus first. Some well-known options for new businesses include secured business credit cards, which help you build history without needing an existing credit score.

Use the cards for regular business expenses. Keep your credit utilization low — meaning, don't max out your credit limits. Keeping utilization below 30% is a good rule to follow.

Step 4: Monitor and Protect Your Business Credit

Check your business credit reports regularly on Dun & Bradstreet, Experian Business, and Equifax Business. Errors happen, and they can hurt your score.

Look for accounts that aren't yours, inaccurate late payments, or outdated information. Dispute anything incorrect directly with the bureau.

How to Open a Business Credit File the Right Way

One of the most common questions is: how do I actually start a business credit file if I have no history?

Here's what you need to understand. Business credit bureaus don't automatically create a file for your business. You need to take action to get one started.

Here's the fastest way to open your business credit file:

Get a D-U-N-S Number — Go to dnb.com and register your business. This creates your file with Dun & Bradstreet, the most widely used business credit bureau.

Apply for starter vendor accounts — As mentioned earlier, net-30 vendors are the entry point. When you make a purchase and pay on time, those payments get reported. That's the first data in your file.

Stay consistent — Your file grows every time a creditor reports your account activity. The more accounts you have reporting positively, the stronger your profile becomes over time.

This process takes patience. But it works. Many small businesses build a solid business credit profile in 6 to 12 months when they follow the right steps.

Common Mistakes That Slow Down Business Credit Building

Knowing what to avoid is just as important as knowing what to do.

Using your SSN for every business application — This ties everything back to your personal credit. Use your EIN and build business credit separately.

Skipping the foundation steps — Applying for credit before you have a legal entity, EIN, and business bank account means denials. Lenders check these basics first.

Not monitoring your credit file — Errors on your business credit report can silently drag your score down. Check it regularly.

Applying for too much credit at once — Multiple applications in a short time can signal financial desperation. Build steadily.

Mixing personal and business finances — This is one of the biggest mistakes. Keep accounts completely separate from day one.

What Lenders Actually Look for Before Approving Business Funding

When you apply for a business loan or line of credit, lenders review several factors. Understanding these can help you prepare before you even apply.

Time in business — Many lenders want to see at least 6 months to 2 years in business. The longer your track record, the better.

Business revenue — Lenders want to see that your business generates real income. Consistent monthly revenue is a positive signal.

Business credit score — A Paydex score of 80 or higher is what most lenders look for. Higher scores mean better terms.

Business bank account activity — Average daily balances and consistent deposits matter. Some alternative lenders look at your last 3 to 6 months of bank statements.

Fundability factors — This includes your business address, phone listing, website, and whether your business information is consistent across all platforms. Inconsistencies raise red flags.

How Long Does It Take to Build Business Credit?

There is no overnight shortcut. Building real business credit takes consistent effort over time.

Here's a realistic timeline for most small businesses:

Month 1 to 2: Set up legal entity, EIN, business bank account, and register for a D-U-N-S number

Month 2 to 4: Open 3 to 5 starter vendor accounts and start using them

Month 4 to 6: First vendor accounts start reporting positive payment history

Month 6 to 12: Business credit score starts building; qualify for store credit cards and some business credit cards

Month 12 to 24: Stronger profile develops; access to more funding options including revolving credit lines and working capital loans

Patience and consistency are the real keys here.

Frequently Asked Questions

Q: Can I build business credit with no personal credit check? Yes, in the early stages. Starter vendor accounts often don't require a personal credit check. As your business credit grows, some lenders will approve funding based entirely on your business profile. That said, many lenders still request a personal guarantee for newer businesses.

Q: Does my business structure matter for business credit? Yes. An LLC or Corporation is required. Sole proprietors and partnerships don't have the legal separation needed to build a true business credit profile.

Q: What is the fastest way to build business credit? Open vendor accounts that report to credit bureaus, pay every account on time or early, keep your credit utilization low, and monitor your file for errors. Following all foundation steps before applying is also essential.

Q: Do all business credit cards report to business bureaus? No. Some business credit cards only report to personal credit bureaus. Always confirm that the card reports to Dun & Bradstreet, Experian Business, or Equifax Business before applying.

Q: What is a good business credit score? On the Dun & Bradstreet Paydex scale, a score of 80 means you pay on time. A score of 90 to 100 means you pay early. Most lenders look for 75 or above for standard credit approvals.

Q: How many trade lines do I need to build business credit? Start with at least 3 to 5 vendor accounts that report to credit bureaus. This gives the bureaus enough data to create a meaningful credit score for your business.

Conclusion: Build Your Business Credit Before You Need It

The biggest mistake small business owners make is waiting until they desperately need funding to think about business credit.

By then, it's too late. You're behind on rent, short on payroll, or trying to buy inventory — and your business has no credit profile. Lenders won't move fast for a business that has no history.

The smart move is to build your business credit right now, before you need it. Every vendor account you open, every on-time payment you make, every step in this guide you follow brings you closer to having real access to business funding.

Funding that doesn't touch your personal credit. Funding that lets your business grow.

If you want help building your business credit from scratch or getting the right funding for your stage of business, Altopex.com can guide you step by step. Reach out today and let's build something real together.