Business Credit Starter Guide for LLC (2026)

New LLC? Learn how to build business credit step by step — from EIN setup to your first credit account. A practical starter guide for small business owners.

BUSINESS CREDIT

Russel

6/1/20267 min read

Most New LLC Owners Get This Wrong From Day One

You formed your LLC. You got your EIN. You opened a business bank account.

And then you waited for funding to come.

But it didn't.

That's because forming an LLC is just the first step. Building real business credit — the kind that lenders, vendors, and suppliers actually look at — takes a deliberate setup process that most new business owners never learn about.

This business credit starter guide for LLC owners walks you through exactly what to do, in the right order, so you stop wasting time and start building a credit profile that opens real funding doors.

What Is Business Credit and Why Does Your LLC Need It?

Business credit is your company's financial reputation. It's separate from your personal credit score.

When you build business credit, lenders and vendors evaluate your LLC on its own merits — not based on your personal financial history. This means you can eventually access funding, trade lines, and business credit cards using your EIN (Employer Identification Number) instead of your Social Security Number.

Here's why this matters for your LLC:

Higher credit limits — Business credit accounts often have 10x the limits of personal cards

No personal liability — Keep your personal finances protected

Better funding options — More lenders open up as your business credit grows

Vendor relationships — Net-30 vendor accounts report directly to business credit bureaus

The three major business credit bureaus are Dun & Bradstreet, Experian Business, and Equifax Business. They each track your business credit separately from the consumer bureaus most people know.

Business Credit Basics for Small Business: The Foundation You Must Build First

Before you apply for a single credit account, your LLC needs to look legitimate and fundable. This is what most guides skip — and it's exactly why so many business owners get denied.

Lenders don't just check your credit score. They verify your business is real. If your business can't pass a basic legitimacy check, your application gets flagged or rejected before it even reaches the credit review stage.

Here's the business credit checklist for a new business:

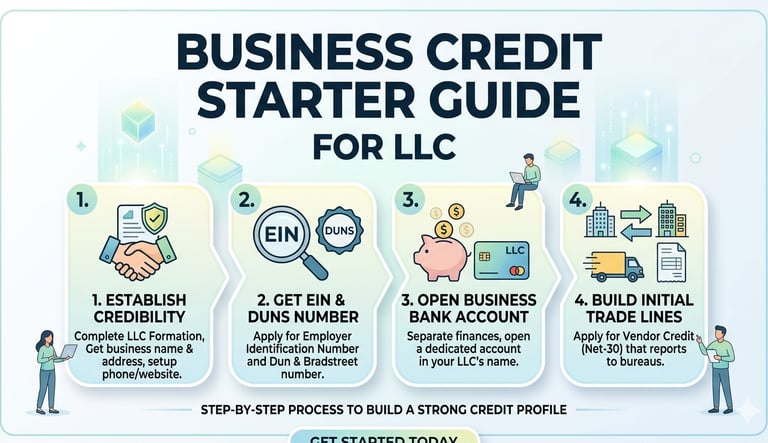

1. Form Your LLC Properly

Make sure your LLC is registered in your state and is in good standing. An active, registered LLC tells lenders you're operating a real legal business entity — not a side gig.

2. Get Your EIN from the IRS

Your EIN is like a Social Security Number for your business. You need it to open a business bank account, apply for credit, and file taxes. Get your EIN free at IRS.gov.

3. Open a Dedicated Business Bank Account

Your business must have its own bank account. Do not mix personal and business finances. A dedicated business checking account is one of the first things lenders check. It shows stability and real business activity.

4. Get a Business Phone Number

Use a dedicated business phone number listed under your company name. Free tools like Google Voice work fine when starting out. What matters is that it's consistent everywhere your business is listed.

5. Get a Business Address

Use a real business address — not a P.O. box and not your home address if possible. A virtual office service works well for this. Your address needs to match everywhere: your website, Google Business Profile, and your credit applications.

6. Build a Basic Business Website

You don't need anything fancy. A clean, professional one-page or five-page website with your business name, services, contact info, and EIN is enough. Many lenders check if your website exists before approving you.

7. Register with 411 and Business Directories

Get listed in 411 directory listings, Google Business, and other online business directories. This makes your business verifiable. Some vendor credit applications actually deny businesses they can't find online.

8. Get a DUNS Number from Dun & Bradstreet

Dun & Bradstreet is the largest business credit bureau. Getting a free DUNS number starts your business credit file with them. Without it, you have no D&B credit history — and many lenders rely on it.

Business Credit Setup for Beginners: The Step-by-Step Path

Once your foundation is in place, it's time to actually start building credit. This part requires patience and the right sequence.

Step 1 — Open Vendor Accounts (Net-30 Accounts)

This is how almost every successful business credit profile starts.

Net-30 vendor accounts give you credit with a supplier and report your payment history to business credit bureaus. You buy products or services, pay the invoice within 30 days, and those on-time payments build your business credit profile.

Some beginner-friendly vendors that report to business credit bureaus include:

Uline — Office and shipping supplies

Grainger — Business tools and safety equipment

Quill — Office supplies (owned by Staples)

Crown Office Supplies — A popular starter vendor

You don't need to spend a lot. Even small purchases paid on time build your file.

Start with 3 to 5 vendor accounts. Pay them consistently and on time. After 3 to 6 months, your business credit score will start forming.

Step 2 — Apply for a Business Credit Card

Once you have a few vendor accounts reporting, look at business credit cards. Some starter-friendly options include:

Secured business credit cards that don't require strong credit history

Credit unions that offer business cards to new LLCs

Store business credit cards from office supply or fuel companies

Use the card for small regular purchases. Keep your credit utilization low — that means don't max out the card. Try to stay below 30% of your limit. Pay the full balance every month if you can.

Step 3 — Monitor Your Business Credit Reports

Check your business credit scores regularly. You can monitor them through:

Nav.com — Shows Dun & Bradstreet, Experian Business, and Equifax Business scores in one place

CreditSafe — Popular with larger businesses

Dun & Bradstreet's own portal

Watch for errors, missing accounts, or anything that could hurt your score. Dispute inaccuracies directly with the bureau.

Step 4 — Keep Your Business Finances Clean

Pay every bill on time. This is the single biggest factor in building a strong business credit profile. Late payments hurt your score fast — and recovery takes time.

Also keep your business bank account balance healthy. When you apply for funding later, lenders will often ask for 3 to 6 months of business bank statements. They want to see consistent cash flow — not a near-zero balance every month.

How to Get Your First Business Credit Account

Getting your first business credit account is often the hardest part. Here's a practical approach that works for new LLCs.

Start with vendors that have easy approval criteria. Some vendors approve new businesses with no established credit history, no personal credit check, and no revenue requirements. These are called starter vendors or tier-1 vendors.

The key is to apply for accounts where you are actually going to buy something. Don't apply for vendor accounts just for the credit line. Buy the supplies your business actually needs, pay on time, and let the reports do the work.

What lenders look for in a new LLC:

Active business bank account (at least 3 months old)

Consistent business address and contact info

DUNS number and at least one active trade line

No major derogatory marks on personal credit (for most early applications)

EIN used instead of SSN on applications where possible

Once you have 3 to 5 trade lines reporting for 6 to 12 months, you become eligible for higher-tier credit accounts, business credit cards, and eventually small business loans and lines of credit.

Common Mistakes That Slow Down Your Business Credit Progress

Knowing what not to do is just as important.

Mixing personal and business finances. This is the fastest way to destroy your business credit strategy. Keep everything separate — bank accounts, cards, expenses.

Applying for too much credit too fast. Multiple applications in a short period can hurt your profile. Space out your applications.

Using the wrong address or contact info. If your business address on your LLC paperwork doesn't match your credit application, it raises red flags. Keep everything consistent.

Ignoring your D&B profile. Many business owners don't realize they have no D&B file at all. Without a DUNS number and active trade lines, you essentially don't exist in the business credit world.

Waiting for credit to "just happen." Business credit doesn't build automatically like personal credit. You have to take deliberate steps to open the right accounts and make them report.

How Long Does It Take to Build Business Credit?

A realistic timeline for most new LLCs:

MilestoneTimelineBusiness credit file opened (D&B)30–60 days after first trade lineFirst business credit score3–6 monthsEligible for business credit cards6–9 monthsEligible for small business loans12–24 monthsStrong fundable business credit profile2–3 years

These are general timelines. Consistent on-time payments and smart account management can speed things up.

FAQs: Business Credit Starter Guide for LLC

Q: Can I build business credit as a new LLC with no revenue? Yes. Many starter vendor accounts don't require revenue or operating history. You can start building business credit from day one of your LLC — as long as your business foundation is set up correctly.

Q: Do I need good personal credit to start building business credit? Not always. Some starter vendors and secured business credit accounts don't require a personal credit check. However, for larger business loans, lenders often review personal credit too — especially for newer businesses.

Q: What credit bureaus track business credit? The main ones are Dun & Bradstreet (D&B), Experian Business, and Equifax Business. Each has its own scoring system. It's important to build history on all three over time.

Q: How many trade lines do I need before applying for a business loan? Most lenders want to see at least 3 to 5 active trade lines with a history of on-time payments. More trade lines with consistent payment history increases your approval chances.

Q: Is a DUNS number free? Yes. You can register for a DUNS number for free directly through Dun & Bradstreet's website at dnb.com.

Q: Should I use my EIN or SSN on business credit applications? Use your EIN wherever possible. This keeps your business credit separate from your personal credit. Some applications still require your SSN for identity verification — but over time, as your business credit profile grows, you can access more options using EIN only.

Final Thoughts: Build It Right From the Start

Building business credit is not complicated. But it does require doing the right things in the right order.

Set up your LLC foundation first. Get your EIN, business bank account, business address, and DUNS number in place. Then open starter vendor accounts, pay them consistently, and monitor your business credit as it grows.

The business owners who struggle with funding are usually the ones who skipped the foundation and jumped straight to loan applications. Don't make that mistake.

Start small, build steady, and your business credit profile will grow into a real financial asset for your LLC.

If you want help building your business credit the right way — from foundation setup to your first credit accounts and beyond — Altopex.com can guide you through every step. Reach out today and let's build your business credit together.