Business Credit Building Timeline Guide (2026)

Learn exactly how long it takes to build business credit, the best steps to follow, and how to fast track business credit building for faster funding access.

Russel

6/9/20268 min read

Most small business owners don't realize they need business credit until they actually need funding. Then they apply, get denied, and wonder what went wrong.

The truth is, business credit doesn't just happen. It takes a clear plan, the right steps done in the right order, and a realistic understanding of timing.

This business credit building timeline guide will show you exactly what to expect, how long each stage takes, and what you can do to speed things up without making costly mistakes.

What Is Business Credit and Why Does It Matter?

Business credit is your company's ability to borrow money or get credit based on its own financial history — not yours.

When your business has strong credit, lenders and vendors look at your EIN (Employer Identification Number) instead of your personal Social Security Number. That means your personal finances stay protected.

Strong business credit gives you access to:

Business credit cards with higher limits

Net-30 vendor accounts (where you buy now and pay in 30 days)

Trade lines — credit accounts that report to business credit bureaus

Working capital loans and lines of credit

Better terms on equipment financing and leases

If your business doesn't have credit yet, you're missing a real financial tool. And the longer you wait to start, the longer you'll wait to get funded.

The Three Main Business Credit Bureaus

Before you understand timing, you need to know who is tracking your business credit.

There are three major business credit bureaus in the US:

1. Dun & Bradstreet (D&B) — Uses a PAYDEX score from 1 to 100. Most lenders and vendors check this one.

2. Experian Business — Tracks payment history and credit activity.

3. Equifax Business — Reports financial strength and credit risk for businesses.

Each bureau works a little differently. Building your score across all three is the goal. And that process takes time — unless you know how to fast track business credit building the right way.

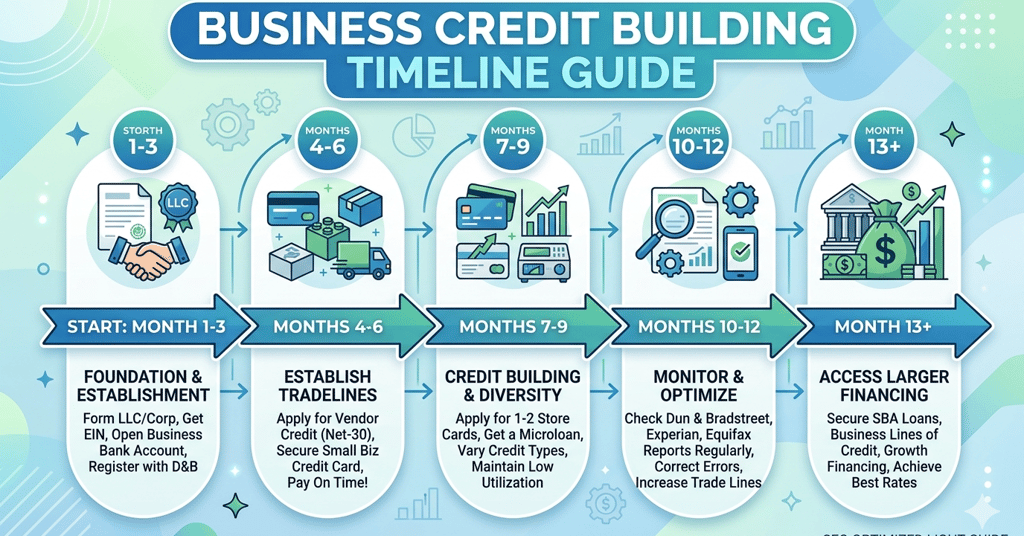

The Business Credit Building Timeline: Stage by Stage

Here's a realistic timeline most business owners go through. This isn't guesswork — this is what actually happens when you do things correctly.

Stage 1: Business Foundation Setup (Weeks 1–4)

Before you can build credit, your business has to look legitimate to lenders and credit bureaus. This stage is often skipped or rushed. That's a mistake.

What you need to set up:

Registered business entity — LLC or corporation. A sole proprietorship won't give you the separation you need.

EIN from the IRS — This is your business's tax ID. It's free and takes minutes online.

Dedicated business address — Not a P.O. Box. Use a physical or virtual office address.

Business phone number — Listed under your business name. Many credit applications verify this.

Business bank account — Opened in your business name, with your EIN.

DUNS Number — Register with Dun & Bradstreet for free. It can take 1–2 weeks to receive.

Business listed in 411 directories — Some lenders check if your business is findable.

This stage takes about 2–4 weeks if you move quickly. Don't skip it. Lenders and credit bureaus use this information to verify your business is real and operating.

Pro tip: Make sure your business name, address, and phone number are consistent everywhere — on your website, on applications, on Google Business Profile. Inconsistency raises red flags.

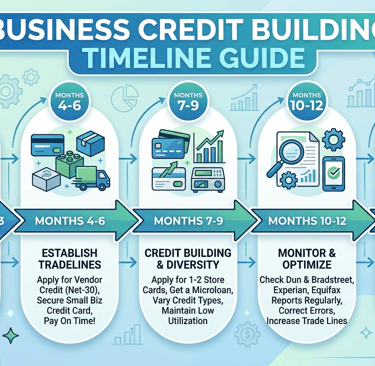

Stage 2: Starter Vendor Accounts and Net-30 Trade Lines (Months 1–3)

Once your business foundation is in place, the next step is opening starter vendor accounts. These are companies that will extend credit to new businesses with no prior credit history.

These are often called Net-30 accounts — meaning you get products or services now and pay within 30 days. When you pay on time, those payments get reported to the business credit bureaus. That's how your credit history starts building.

Common starter vendor types:

Office supply vendors

Business fuel card providers

Shipping and packaging suppliers

Marketing and print service companies

These vendors are known as tier-1 vendors in the business credit world. They approve based on your EIN and business profile, not your personal credit.

Timeline for this stage: After 3–5 on-time payments, most vendors report your account. That gives you 60–90 days to get your first real tradelines showing up on your D&B, Experian, and Equifax business reports.

The key here is consistency. Small purchases made regularly and paid on time are more valuable than one large purchase.

Stage 3: Business Credit Card Access (Months 3–6)

Once you have a few vendor accounts reporting, your business profile starts to develop a real score. At this point, you may qualify for certain business credit cards that don't require strong personal credit.

Some store-branded business credit cards report to business bureaus and have more flexible approval requirements for newer businesses.

At this stage, you're building revolving credit — credit you can use and pay down repeatedly. This is different from trade lines and it signals to lenders that your business can manage credit responsibly.

What to watch:

Keep your credit utilization (the percentage of available credit you're using) below 30%. So if your card limit is $1,000, try not to carry more than $300 in balance.

Always pay on time. Late payments hurt your score more than almost anything else.

Don't apply for too many accounts at once. Multiple applications in a short time can look risky.

By month 6, if you've done this correctly, your business credit score should be developing. Some business owners reach a PAYDEX score of 75+ within this window.

Stage 4: Tier-2 and Tier-3 Credit Access (Months 6–12)

After 6 months of consistent activity, you have enough history to apply for stronger accounts.

Tier-2 vendors typically require some business credit history before approving. These include larger wholesale suppliers, business service providers, and some fleet fuel accounts.

Tier-3 accounts include bank-issued business credit cards with real credit limits, business lines of credit, and some equipment financing options.

At the 9–12 month mark, businesses with a strong credit profile often start getting approved for:

Business credit cards from major banks (Chase Ink, Capital One Spark, American Express Business, etc.)

Business lines of credit from online lenders

SBA microloans or small business loans

This is where the real funding opportunities open up.

Stage 5: Established Credit and Larger Funding Access (12–24 Months)

By the 12–24 month range, a well-managed business credit profile can unlock significant funding opportunities.

This includes:

Higher-limit business credit cards ($10,000–$50,000+)

Working capital loans from banks or alternative lenders

SBA 7(a) loans

Business lines of credit up to $100,000 or more

Net-60 and Net-90 terms from major suppliers

Lenders at this level look at your full credit picture — payment history, utilization, age of accounts, and overall fundability. If you've been consistent since month one, you're in a strong position.

How to Fast Track Business Credit Building Without Cutting Corners

Now you know the timeline. But what if you need to move faster?

Here are the best steps to build business credit faster while staying on solid ground:

1. Set Up Your Business Foundation Correctly the First Time

Redoing the foundation because of mistakes adds weeks to your timeline. Get your LLC registered, EIN applied, and business address set up correctly from day one.

2. Open Multiple Vendor Accounts at Once

Instead of opening one at a time, open 3–5 starter vendor accounts in the same month. This builds your history faster and shows multiple reporting trade lines sooner.

3. Make Small Purchases and Pay Early

Don't wait for the full 30 days to pay. Paying early can improve your PAYDEX score faster. D&B rewards early payments with higher scores.

4. Monitor Your Business Credit Reports

Check your Dun & Bradstreet, Experian Business, and Equifax Business reports regularly. Make sure vendor accounts are reporting. If something isn't showing up, contact the vendor or bureau.

5. Avoid Personal Credit Dependency

Every time you use your SSN for a business application, you're building personal credit, not business credit. Use your EIN wherever possible. This separates your business finances and protects your personal score.

6. Build Your Business Bank History in Parallel

Lenders — especially banks — look at your business bank account history. Consistent deposits, positive balance, and no overdrafts improve your fundability even before you apply for a loan.

Common Mistakes That Slow Down Business Credit Building

These mistakes cost months of progress. Avoid them.

Not having a registered business entity. Sole proprietors can't separate personal and business credit properly.

Using a home address instead of a business address. This reduces lender confidence.

Opening only one vendor account. One tradeline isn't enough. You need at least 3–5 to build a real profile.

Applying for bank credit too early. Banks want to see history. Apply before you're ready and you'll get denied — and waste a hard credit inquiry.

Ignoring your credit reports. Errors and unreported accounts are common. Review them regularly.

Business Credit Building for Beginners: Where to Start

If you're brand new to this, here's a simple starting point:

Register your LLC and get your EIN

Open a business checking account

Get your DUNS number from D&B

Apply for 3–5 starter Net-30 vendor accounts

Make small purchases and pay on time (or early)

Monitor your reports after 60 days

Apply for a basic business credit card once your profile shows activity

That's the foundation. Once those steps are complete, you're on the right track.

How Long Does It Really Take to Build Business Credit?

Here's a quick summary for people looking for a direct answer:

StageTimelineWhat You're BuildingFoundation SetupWeeks 1–4LLC, EIN, DUNS, bank accountStarter Vendor AccountsMonths 1–3First tradelines, credit historyBusiness Credit CardsMonths 3–6Revolving credit, growing scoreTier-2 and Tier-3 AccessMonths 6–12Stronger accounts, bigger limitsEstablished CreditMonths 12–24Full funding access, bank loans

The short answer: You can start seeing results in 3–6 months. But to access significant funding, plan for 12–18 months of consistent credit building.

That said, with the right steps done in the right order, many business owners fast track business credit building and access solid funding well before the 12-month mark.

Frequently Asked Questions

Q: How long does it take to build business credit from scratch? Most businesses can develop a functional credit profile in 3–6 months with the right vendor accounts in place. Full access to bank-level funding typically takes 12–18 months.

Q: Can I build business credit without using my personal credit? Yes. If your business is properly registered with an LLC or corporation and has an EIN, many starter vendors and some credit cards report only to business credit bureaus — not personal ones.

Q: What credit score do I need to get a business loan? It depends on the lender. Many online lenders work with businesses that have a PAYDEX score of 60 or higher. Traditional banks typically want 75+ PAYDEX and 12+ months of business history.

Q: What is a trade line in business credit? A trade line is any credit account that reports payment activity to business credit bureaus. Vendor accounts, business credit cards, and supplier accounts all count as trade lines.

Q: Can a new LLC build business credit? Yes. A new LLC can start building credit immediately by getting an EIN, opening a business bank account, and applying for starter Net-30 vendor accounts. You don't need revenue or prior history to start.

Q: Does a business bank account help with business credit? Not directly with credit bureaus — but yes indirectly. Banks and lenders often look at your business bank history when reviewing loan or credit applications. Healthy bank activity improves your overall fundability.

Final Thoughts

Building business credit the right way takes time. But it doesn't have to feel confusing or overwhelming.

If you follow this business credit building timeline — foundation first, vendor accounts next, then credit cards, then larger funding — you create a path that lenders trust. And that trust turns into real money for your business.

The biggest mistake most owners make is waiting too long to start. Every month you delay is a month your business is working without one of its most powerful financial tools.

If you want help building your business credit step by step — or if you're not sure where you stand right now — Altopex.com can guide you through the entire process. From setting up your business foundation to accessing real funding, we help US small business owners build credit the right way.

Reach out to Altopex.com and take the first step toward stronger business credit today.