Simple Business Credit Building Process: A Step-by-Step Guide for Small Business Owners

Learn the simple business credit building process step by step. Set up your business credit profile, get trade lines, and access real funding — without using your SSN.

Russel

5/26/20269 min read

Most small business owners want funding. But when they apply, lenders say no. Not because the business is failing. But because the business has no credit history.

That is the real problem.

Business credit is not something that builds automatically. You have to set it up the right way, in the right order. And most owners have never been shown how.

This guide breaks down the simple business credit building process from scratch. Whether you just started your LLC or have been in business for a few years, these steps can help you build a real credit profile that lenders and vendors actually recognize.

What Is Business Credit and Why Does It Matter?

Business credit is your company's financial reputation. It is separate from your personal credit score.

When lenders, suppliers, or vendors want to know if your business is trustworthy, they check your business credit profile. Not your personal score.

A strong business credit profile means:

You can get funding without putting your personal finances at risk

Vendors will extend payment terms so you can buy now and pay later

Lenders offer better interest rates and higher credit limits

You do not need to personally guarantee every loan

For small business owners, this is a big deal. It gives you separation between your personal life and your business finances. And it opens doors to more money when you need it.

Why Most Small Businesses Have No Business Credit

Here is why so many small businesses struggle with this.

When you open a business, nothing happens automatically. No credit bureau is automatically tracking your business payments. No lender is automatically building a file for you. You have to take active steps to make it happen.

Most owners skip those early setup steps. They use their personal credit card for business expenses. They pay suppliers from their personal account. They never register with Dun & Bradstreet or Experian Business.

So years go by, and the business still has no credit identity. Then when they need a loan or a credit line, lenders have nothing to look at.

The good news is, you can fix this. And the simple business credit building process is not complicated once you understand the steps.

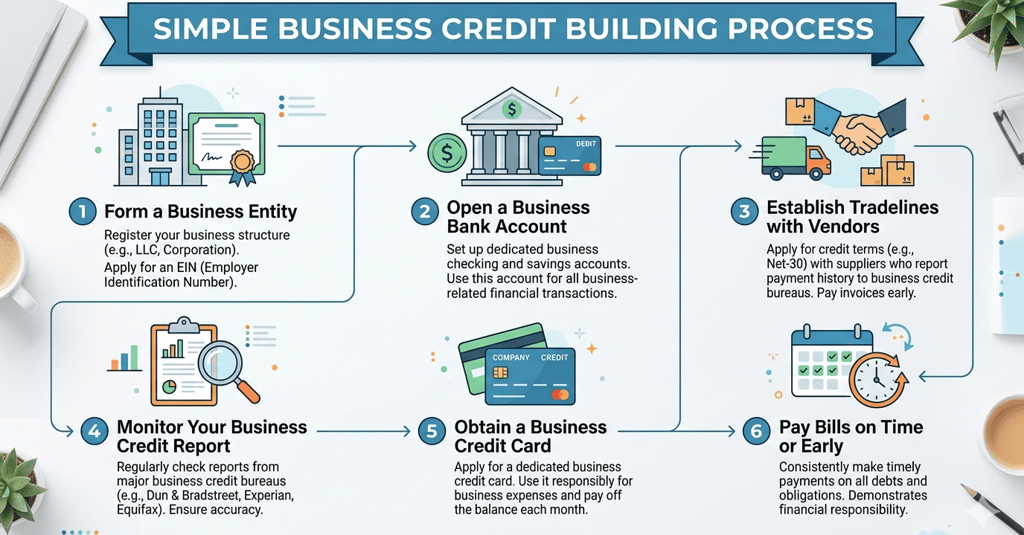

Step 1: Set Up Your Business as a Separate Legal Entity

The first step in any business credit profile setup guide starts here: make your business real in the eyes of lenders and credit bureaus.

That means:

Form an LLC or Corporation. Sole proprietorships are hard to build credit for because they are not truly separate from you as a person. An LLC gives your business its own legal identity.

Get a Federal EIN (Employer Identification Number). This is like a Social Security Number for your business. You apply for it free at IRS.gov. Every business credit application will ask for it. EIN credit — meaning credit built under your EIN rather than your SSN — is the foundation of a real business credit profile.

Open a dedicated business bank account. Keep all business money separate from personal money. This is something lenders specifically look for.

Get a business phone number. List it publicly. Credit bureaus and lenders verify businesses using directory listings. A phone number tied to your business address builds legitimacy.

Set up a professional business address. A real street address looks better than a P.O. box. If you work from home, consider a virtual office address.

These steps might seem basic. But they are non-negotiable. Without them, the rest of the process will not work.

Step 2: Register Your Business With Credit Bureaus

This is a step most small business owners never hear about.

Personal credit bureaus like Equifax and TransUnion automatically track your personal payments. Business credit bureaus do not work the same way. You have to register with them.

The three main business credit bureaus are:

Dun & Bradstreet (D&B) — This is the most important one for business credit. You need a DUNS Number to have a file with them. You can get one free at dnb.com. Most large suppliers and lenders check D&B before making a decision.

Experian Business — Experian tracks business credit separately from personal credit. Lenders and banks often pull your Experian Business report.

Equifax Business — Similar to Experian. Some lenders check Equifax Business reports as part of their approval process.

Once your business is registered, these bureaus can start recording your payment history. But they only record what is reported to them. That brings us to the next step.

Step 3: Start With Starter Vendor Accounts (Trade Lines)

This is how business credit actually gets built.

Trade lines are accounts with vendors or suppliers that report your payment history to business credit bureaus. When you open an account with a vendor, buy something, and pay on time, they report that positive payment. Those reports build your credit file.

Not every vendor reports to credit bureaus. You need to specifically find ones that do.

Some commonly used starter vendors that are known to report to business credit bureaus include:

Uline — office and shipping supplies

Quill — office supplies and equipment

Grainger — industrial and business supplies

Strategic Network Solutions — business technology products

Crown Office Supplies — office products

These vendors often do not require a personal credit check to open an account. They are sometimes called net-30 vendors, meaning you have 30 days to pay after purchase.

When you pay on time — every time — those payments get reported and start building your business credit score.

This is how you build a business credit checklist for new business owners: start small, pay on time, and let the reports stack up.

Step 4: Apply for a Business Credit Card

Once you have 3 to 5 trade line accounts reporting for 60 to 90 days, your business credit profile is starting to take shape.

This is a good time to apply for a business credit card.

Business credit cards are powerful tools. They give you revolving credit — meaning you can use the card, pay it off, and use it again. When used wisely, revolving credit helps raise your business credit scores over time.

Some business credit cards that are easier to get approved for early on include secured business cards and cards from your existing business bank. Secured cards require a deposit, but they report to business credit bureaus and help you build history.

The key with business credit cards is credit utilization. That is the ratio of what you owe versus your credit limit. Keeping this below 30% shows lenders you are not overextending your business. For example, if your card limit is $5,000, try to keep your balance under $1,500.

Pay the full balance on time every month. This builds positive history and avoids interest charges.

Step 5: Monitor Your Business Credit Scores

You cannot fix what you cannot see.

Monitoring your business credit scores regularly is an important part of keeping your profile healthy. It also helps you catch errors, which do happen. An error on your business credit file could be hurting your ability to get approved for funding without you knowing it.

You can monitor your business credit through:

Nav.com — shows both personal and business credit scores

Dun & Bradstreet CreditSignal — free monitoring for your D&B score

Experian Business Credit Advantage — paid monitoring for your Experian business file

When you check your scores, look at your payment history, your number of active accounts, and how long your accounts have been open. These are the main factors that drive your business credit score up or down.

Step 6: Establish Business Credit With Banks

After 6 to 12 months of building trade lines and using a business credit card, you are in a much stronger position.

Now you can start approaching banks for higher-level credit products.

This includes:

Business lines of credit — a revolving credit line you draw from as needed. Useful for covering gaps in cash flow.

Working capital loans — short-term loans for operating expenses, inventory, or equipment. Working capital loans are one of the most common funding options for small businesses.

SBA loans — backed by the U.S. Small Business Administration, these loans often come with lower interest rates. They have more requirements but are worth pursuing once your business credit profile is solid.

When you apply to a bank for any of these, they will check your business credit profile, your time in business, your revenue, and often your business bank account history. Having a strong business credit file significantly improves your chances.

The Business Credit Checklist for New Business Owners

Here is a simple checklist to follow as you go through this process:

Form an LLC or Corporation

Apply for your EIN from IRS.gov

Open a dedicated business bank account

Get a business phone number and address listed in public directories

Obtain your DUNS Number from Dun & Bradstreet

Register with Experian Business and Equifax Business

Open 3 to 5 starter vendor (net-30) accounts that report to business bureaus

Pay vendor accounts on time, every time

Apply for a business credit card after 60 to 90 days of trade line history

Keep credit utilization below 30%

Monitor your business credit scores every 30 to 60 days

Apply for a business line of credit or working capital loan after 6 to 12 months

This is your practical business credit basics for small business guide. Follow these steps in order and you will be building real, reportable business credit.

How Long Does It Take to Build Business Credit?

This is one of the most common questions, and the honest answer is: it depends on how actively you work the process.

Most business owners who follow the steps above can see a solid business credit profile within 6 to 12 months. Some get there faster.

The main factors that affect your timeline:

How quickly you open and use vendor accounts — the sooner you start, the sooner reporting begins

Whether you pay on time — even one late payment can slow your progress

How many accounts you open — more active, reporting accounts build your file faster

Whether your business information is consistent — make sure your business name, address, and phone number are identical across all filings, accounts, and bureau registrations

Inconsistencies — even small ones like abbreviating "Street" vs. spelling it out — can slow down bureau recognition of your business.

Common Mistakes to Avoid

A lot of business owners start this process but make mistakes that slow them down. Here are the ones to watch out for.

Mixing personal and business finances. This is the most common mistake. Always keep them separate.

Opening accounts that do not report to bureaus. Not all vendor accounts report. Before opening an account, confirm that the vendor reports to at least one major business credit bureau.

Applying for too many credit products at once. Each application can trigger a credit inquiry. Too many inquiries in a short period can work against you.

Ignoring your business credit scores. Building credit and not monitoring it is like planting seeds and never watering them. Check your scores regularly.

Using a personal address or personal phone number for your business. These need to be dedicated business contact details.

How to Establish Business Credit Quickly

If you want to move faster, there are a few ways to accelerate your timeline.

First, open multiple starter vendor accounts at once rather than one at a time. If three vendors all start reporting at the same month, your credit file builds faster.

Second, look into becoming an authorized user or getting a credit builder account through your bank. Some banks offer products specifically designed to help new businesses build credit history.

Third, work with a business credit consultant who knows which vendors, lenders, and programs work best for businesses at your stage. A professional can help you avoid wasted time and wrong turns.

FAQs About the Simple Business Credit Building Process

Q: Can I build business credit without using my SSN? Yes. Once your business is properly registered with an EIN, you can apply for vendor accounts and some credit cards using just your EIN. Many starter vendor accounts do not require a personal credit check. As your business credit file grows, more lenders will approve based on your business credit alone.

Q: How is business credit different from personal credit? Personal credit is tied to you as an individual and uses your SSN. Business credit is tied to your company and uses your EIN. They are tracked by different bureaus and scored differently. Building business credit protects your personal credit and gives your company its own financial identity.

Q: What is a good business credit score? Different bureaus use different scoring systems. With Dun & Bradstreet, the main score is called the PAYDEX score. A score of 80 or above is considered good. Experian Business scores range from 0 to 100, with higher being better. Equifax uses a different model. Generally speaking, consistent on-time payments are the fastest way to build a high score with any bureau.

Q: Do I need revenue to start building business credit? No. You can start the foundational steps — forming your LLC, getting your EIN, registering with bureaus, and opening starter vendor accounts — before your business has significant revenue. In fact, the earlier you start, the better.

Q: What is a net-30 vendor account? A net-30 account is a credit arrangement where you receive goods or services now and have 30 days to pay. When you pay on time, the vendor reports that payment to business credit bureaus. These accounts are one of the best starting points for building your business credit profile.

Q: Can a startup build business credit? Absolutely. Startups can follow the exact same process outlined in this guide. The key is starting with the right structure — LLC, EIN, business bank account — and then working your way up through vendor accounts and business credit cards.

Build Business Credit the Right Way

Getting business funding is not something that happens overnight. But it does start with a clear plan.

The simple business credit building process comes down to this: set up your business correctly, register with the right bureaus, open accounts that report your payments, pay on time, and let your credit profile grow over time.

Every step you take now makes it easier to access funding later. A business line of credit, a working capital loan, a higher-limit business credit card — all of these become more accessible as your business credit profile gets stronger.

If you want help going through this process the right way, Altopex.com can guide you step by step. From setting up your business credit profile to finding the right funding options for your stage, we help small business owners across the US build the credit and access the capital they deserve.