How to Open a Business Credit File (2026 Guide)

Learn how to open a business credit file the right way. A simple step-by-step business credit profile setup guide for US small business owners and startups.

BUSINESS CREDIT

Russel

6/8/20268 min read

Most small business owners don't think about business credit until they need funding. Then they apply — and get denied. Or they get approved, but with low limits and high interest rates.

The reason? They never opened a business credit file.

If lenders can't find your business in the credit system, they treat you like a risk. And a risky borrower gets bad terms — or no funding at all.

The good news is that opening a business credit file is not complicated. You just need to know the right steps and do them in the right order. This guide walks you through the entire process, from scratch.

What Is a Business Credit File?

A business credit file is a record that credit bureaus — like Dun & Bradstreet, Experian Business, and Equifax Business — keep on your company.

Think of it like your business's financial reputation. Lenders, suppliers, and vendors check this file before they decide to work with you or extend credit.

When you first start a business, that file doesn't exist. You have to create it. This is what people mean when they talk about how to open a business credit file.

Without a business credit file, your business is invisible to the financial system. That limits your access to business credit cards, vendor accounts, trade lines, and working capital loans.

Why Opening a Business Credit File Matters

Here's something many business owners don't realize. Your business credit is completely separate from your personal credit — when it's set up correctly.

That matters for a few big reasons:

Higher funding limits. Business credit lines are typically larger than personal credit limits.

No personal risk. Lenders don't have to check your personal credit score if your business credit is strong enough.

Better vendor terms. Suppliers are more likely to extend net-30 or net-60 payment terms to businesses with an established credit profile.

More funding options. Banks, credit unions, and online lenders all look at business credit before approving applications.

If you want to grow your business and access real funding, you need to build a solid business credit profile. And it all starts with opening that file.

Business Credit Setup for Beginners: What You Need Before You Start

Before you can open a business credit file, you need to have a few things in place. These are not optional. Lenders and credit bureaus use these to verify your business is real and legitimate.

1. Register Your Business as a Legal Entity

If you're operating as a sole proprietor under your own name, your business doesn't really exist as a separate legal entity. That means it can't build separate credit.

You need to register as an LLC, S-Corp, or C-Corp with your state. Most small business owners choose an LLC because it's simple, affordable, and protects personal assets.

Once you're registered, your business becomes a legal entity that can sign contracts, open bank accounts, and — most importantly — build business credit on its own.

2. Get an EIN (Employer Identification Number)

An EIN is a federal tax ID for your business. It works like a Social Security Number, but for your company.

You apply for one free through the IRS website. It takes about 15 minutes.

Your EIN is critical for opening a business bank account, applying for trade lines, and building EIN credit — which is business credit tied to your EIN instead of your personal SSN.

3. Open a Dedicated Business Bank Account

Your business needs its own bank account. Not a personal account you also use for business. A real, separate business checking account.

Why does this matter? Because lenders want to see that your business operates professionally. A dedicated business bank account shows that. It also makes it easier to track income and expenses, which matters when you apply for working capital loans.

4. Get a Business Phone Number and Address

This sounds small, but it's important for your business credit profile setup.

Your business contact information should be listed consistently everywhere — on your website, your Google Business listing, and any credit applications. Use a real phone number (not just your cell) and a physical or virtual business address.

Credit bureaus use this information to verify your business exists. Inconsistent information can cause delays or errors in your credit file.

5. Build a Basic Online Presence

A professional website and a Google Business profile help establish legitimacy. Lenders and credit bureaus do basic checks. If they can't find your business online, that can raise flags.

You don't need anything fancy. A simple, clean website with your business name, services, and contact information is enough.

How to Open a Business Credit File Step by Step

Now that your foundation is set up, here's how to actually open and build your business credit file.

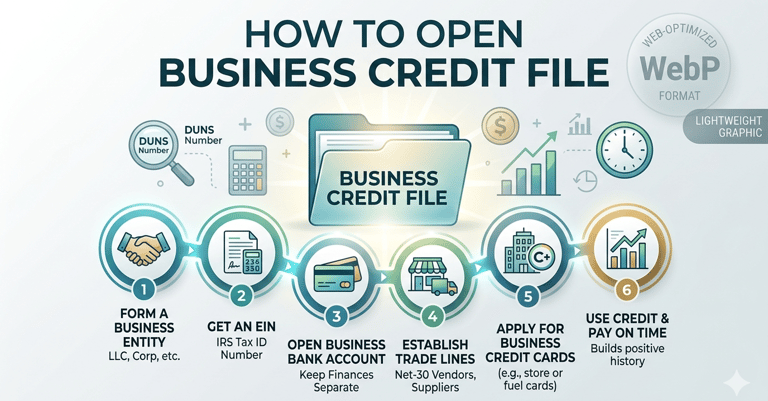

Step 1: Register with Dun & Bradstreet and Get a DUNS Number

Dun & Bradstreet (D&B) is one of the most important business credit bureaus in the US. Most major lenders and suppliers check your D&B credit profile before making decisions.

To start a file with D&B, you need a DUNS Number. It's a unique 9-digit identifier assigned to your business.

You can register for a DUNS Number free at the D&B website. The process typically takes a few business days.

Once you have your DUNS Number, your business credit file at D&B is officially open. But at this point, it's empty. The next steps fill it with positive information.

Step 2: Apply for Vendor Accounts That Report to Business Credit Bureaus

This is one of the most important parts of building a business credit profile — and many business owners skip it.

Vendor accounts (also called trade lines) are credit accounts with suppliers and vendors. When you purchase from them on net terms and pay on time, they report your payment history to the credit bureaus.

That payment history builds your business credit score.

Look for vendors in categories like:

Office supplies (Quill, Uline, Grainger)

Fuel and fleet cards (WEX, Fuelman)

Business services (Crown Office Supplies, Wise Business Plans)

These are often called "starter vendors" because they have easier approval requirements. Many don't require a personal credit check or a long business history. They're designed specifically to help new businesses start building a credit profile.

The key is to actually use the accounts and pay them on time. Even small purchases — paid early — help build your credit profile quickly.

Step 3: Open a Business Credit Card That Reports to Business Bureaus

Once you have a few vendor accounts reporting, you can apply for a business credit card.

Not all business credit cards report to business credit bureaus. Some only report to personal credit bureaus. Make sure you choose one that reports to Dun & Bradstreet, Experian Business, or Equifax Business.

A business credit card does two things:

It adds another trade line to your business credit file.

It gives you a revolving credit account — which credit bureaus view positively when managed well.

Keep your credit utilization low (under 30% of your limit) and pay the balance on time. This builds your business credit score consistently.

Step 4: Monitor Your Business Credit Reports

Once your file is open and you're adding trade lines, you need to monitor your reports regularly.

Check for errors, missing accounts, or outdated information. Errors happen more often than most people realize, and they can hurt your credit score and your ability to get approved for funding.

You can check your business credit reports directly through:

Dun & Bradstreet – D&B Credit Signal or CreditBuilder

Experian Business – Business Credit Advantage

Equifax Business – Business Credit Monitor

Catching errors early and disputing them keeps your profile accurate and strong.

Step 5: Apply for a Net-30 Business Account at Your Bank

Once you've been building trade lines for 3–6 months, go back to your business bank. Ask about a business line of credit or a net-30 account.

Having a history of on-time payments through vendor accounts strengthens your application. The bank can now see that your business is creditworthy, not just assumed.

This is where your business credit profile starts turning into real funding access.

Business Credit Checklist for New Business Owners

Use this as your quick reference when setting everything up:

Register business as LLC or corporation

Get your EIN from the IRS

Open a dedicated business bank account

Set up a professional business address and phone number

Build a basic website and Google Business profile

Register for a DUNS Number at Dun & Bradstreet

Apply for 2–3 starter vendor accounts

Apply for a business credit card that reports to business bureaus

Monitor your business credit reports regularly

Apply for a business line of credit after 3–6 months of positive history

Common Mistakes to Avoid

Even with the right steps, some business owners slow down their progress by making these mistakes.

Using personal credit for business purchases. Every time you use personal credit for business, you mix your finances. This makes it harder to build separate business credit.

Not checking if vendors report to business bureaus. Not all vendors report payment history. Always confirm before applying.

Applying for too many accounts at once. Multiple applications in a short time can look risky to lenders. Space them out by a few weeks.

Inconsistent business information. If your business name is slightly different on different applications, credit bureaus may not match the accounts to your file. Be exact and consistent every time.

Ignoring the credit file after opening it. Opening the file is just step one. You need to actively build it with trade lines and monitor it for accuracy.

How Long Does It Take to Build a Strong Business Credit Profile?

This is one of the most common questions business owners ask.

Realistically, it takes 6 to 12 months to build a solid business credit file from scratch — if you follow the right steps consistently.

Some businesses start qualifying for larger credit lines and working capital loans within 6 months. Others take a full year.

The speed depends on:

How quickly you set up your foundation

How many vendor accounts you open

Whether you pay on time, every time

How consistent your business information is across all applications

There are no shortcuts. But there is a right path. And when you follow it, results do come.

Frequently Asked Questions

Q: Can I open a business credit file with no revenue yet?

Yes. You can start building a business credit profile before your business makes money. The key is to have your legal structure, EIN, and business bank account set up first. Revenue helps when applying for larger funding, but it's not required to open a credit file.

Q: Do I need good personal credit to open a business credit file?

Not necessarily. Many starter vendor accounts don't require a personal credit check. However, for business credit cards and larger loans, some lenders may still review your personal credit — especially in the early stages.

Q: What credit bureaus track business credit?

The main business credit bureaus in the US are Dun & Bradstreet, Experian Business, and Equifax Business. Each has its own scoring system. It's a good idea to build a profile with all three over time.

Q: How is a DUNS Number different from an EIN?

Your EIN is your federal tax ID, issued by the IRS. Your DUNS Number is a separate business identifier used by Dun & Bradstreet to track your credit profile. You need both, and they serve different purposes.

Q: Does opening a business credit file hurt my personal credit?

Opening a business credit file itself does not affect your personal credit. However, applying for certain business credit cards or loans may involve a hard pull on your personal credit, depending on the lender.

Q: What's the fastest way to build business credit from scratch?

The fastest legitimate path is to set up your legal entity, get your EIN, open a business bank account, and apply for 2–3 starter vendor accounts that report to business bureaus. Make small purchases and pay them early. Consistency over 6 months builds a real, usable credit profile.

Final Thoughts

Opening a business credit file is one of the most important things you can do for your company's financial future.

It separates your business from your personal finances. It builds credibility with lenders. And it opens the door to real funding — business credit cards, trade lines, working capital loans, and lines of credit that can help your business grow.

The process takes time. But every step you take now makes future funding easier and more accessible.

If you're not sure where to start or want help setting up your business credit profile the right way, Altopex.com can guide you through every step — from your first vendor account to your first line of credit.

Take the first step today. Your business credit file won't build itself — but with the right guidance, it can grow faster than you think.

Need help with business credit setup or funding access? Contact Altopex.com and let us help you build a strong business credit profile from the ground up.