How to Establish Business Credit Quickly | Altopex

Learn how to establish business credit quickly in 2026. Step-by-step guide for US small business owners to build EIN credit, open vendor accounts, and get funding fast.

BUSINESS CREDIT

Russel

6/13/20267 min read

Most small business owners don't know their business can have its own credit profile — completely separate from their personal credit score.

That means you can qualify for business funding, trade lines, and credit cards using your Employer Identification Number (EIN) — not your Social Security Number (SSN). But here's the problem. If you don't set things up the right way from the beginning, that business credit profile either doesn't exist or works against you when lenders check it.

This guide is going to show you exactly how to establish business credit quickly — in the right order, with the right steps. Whether you're just starting or you've been in business for a while, this works.

Why Business Credit Matters More Than Most Owners Realize

When a lender looks at your business, the first thing they want to know is: does this business have a track record?

They check your business credit profile — not just your personal score. If your business has no credit history, most lenders won't approve you. Or if they do, the limits are low and the terms are bad.

But when your business has a solid credit profile? You can access:

Business credit cards with higher limits

Net-30 vendor accounts (suppliers who give you 30 days to pay)

Working capital loans without heavy personal guarantees

Revolving credit lines for ongoing business needs

That's real financial leverage. And the good news is, you can start building business credit today — even if your business is new.

Step 1: Set Up Your Business the Right Way First

Before you can build credit, your business needs to look legitimate to lenders and credit bureaus. This is called fundability — it just means your business checks all the basic boxes that lenders expect to see.

Here's what you need:

Formal business entity Register your business as an LLC or corporation. Sole proprietorships don't get the same treatment from lenders. An LLC gives you legal separation from your personal finances, and that separation matters when building EIN credit.

Employer Identification Number (EIN) An EIN is basically a Social Security Number for your business. The IRS gives it to you for free at irs.gov. Once you have it, your business can open bank accounts, apply for vendor accounts, and start building a credit profile separate from your SSN.

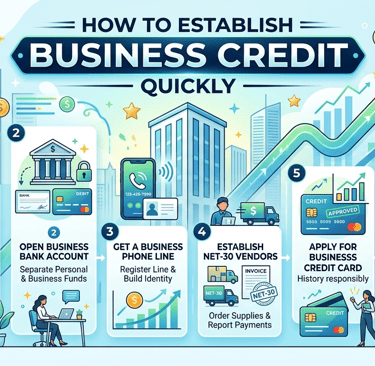

Business bank account Open a dedicated business checking account. Use it only for business transactions. Lenders and credit bureaus look at this. It shows your business is real and operating.

Business phone number and address Use a real business phone number (not a personal cell) and a consistent business address. These need to match across all your filings and applications. Even small inconsistencies can slow down your credit building.

Business listings Make sure your business is listed correctly in 411 directories and platforms like Google Business Profile. Many lenders verify your business through these sources.

If any of these foundational pieces are missing or inconsistent, fix them before you apply for anything. This step alone can save you from unnecessary rejections.

Step 2: Get a D-U-N-S Number from Dun & Bradstreet

Dun & Bradstreet (D&B) is one of the major business credit bureaus in the US — along with Experian Business and Equifax Business. They track your business credit history and generate scores that lenders actually use.

A D-U-N-S Number is your business's unique ID in the D&B system. You need it to start building a D&B credit profile.

Getting one is free at dnb.com. Once you have it, you're visible to lenders who check D&B scores. That's a big step toward being taken seriously for funding.

Step 3: Open Your First Business Credit Account

This is where a lot of business owners get stuck. They try to apply for a business credit card right away and get denied because they have no business credit history yet. It's a classic catch-22.

The way around it? Start with vendor accounts that report to business credit bureaus.

These are sometimes called Net-30 accounts or starter vendor accounts. They work like this: you buy something from the vendor on credit, and you have 30 days to pay. The vendor reports your on-time payment to the business credit bureaus. This starts building your profile.

Some vendors that are known to work well for beginners include office supply companies, packaging suppliers, and shipping service accounts. The key is that they must report to at least one major business credit bureau — D&B, Experian Business, or Equifax Business.

How to get your first business credit account:

Apply with your EIN, business name, and contact details

Make a small purchase on credit

Pay the invoice on time (or early)

Confirm they report to business credit bureaus

Repeat with 2–3 more vendors over the first few months

Five to seven reporting trade lines (that's the technical term for these vendor accounts) is a solid foundation for most credit-building goals.

Step 4: Build a Payment History That Lenders Love

Business credit scores — especially your Paydex score from D&B — are heavily based on how fast you pay your bills.

A perfect Paydex score is 80. That means you pay on time. Scores above 80 mean you pay early. That's where you want to be.

Here's the simple truth: pay every invoice early if you can. Even just a few days early makes a difference. This single habit can push your Paydex score up fast.

Also keep in mind:

Don't apply for too many accounts at once. Spread them out over 2–3 months.

Keep your credit utilization low — that means don't use more than 30% of any credit limit you have.

Make sure every account reports to the credit bureaus. Not all vendors do, so ask before you apply.

Step 5: Apply for a Business Credit Card

Once you have a few vendor accounts reporting and a basic credit history established, you're in a much better position to apply for a business credit card.

Look for cards designed for businesses with limited credit history first. Many credit unions and smaller banks offer these. Some secured business credit cards are also a good option early on — you put a deposit down, use the card, and build a payment record.

When you use a business credit card:

Keep the balance low relative to the limit

Pay in full or early every month

Use it for regular business expenses (supplies, subscriptions, small purchases)

Over time, your credit limit can grow. And that opens the door to larger credit lines and better funding products.

Step 6: Monitor Your Business Credit Reports

A lot of business owners build credit and never check their reports. That's a mistake.

Errors on business credit reports are more common than people think. A wrong payment date, a missing account, or incorrect business information can drag your score down without you even knowing.

Check your business credit reports at least once a quarter with:

Dun & Bradstreet (dnb.com)

Experian Business (experian.com/business)

Equifax Business (equifax.com/business)

If you spot errors, dispute them immediately. Each bureau has a process for this. Don't let bad data sit there and hurt your access to funding.

Step 7: Graduate to Larger Funding Products

Once your business credit profile is solid — usually after 6 to 12 months of consistent, positive activity — you become eligible for more substantial funding options:

Business lines of credit: Revolving credit you can draw from as needed and repay. Great for managing cash flow.

SBA microloans: Small loans backed by the US Small Business Administration, good for early-stage businesses.

Working capital loans: Short-term funding to cover operational costs, payroll, inventory, or growth needs.

Net-60 and Net-90 vendor accounts: Longer payment terms as your profile grows.

The goal is to keep growing your profile over time. Every account you open and pay on time makes your business look more creditworthy to lenders.

How Long Does It Actually Take?

Here's a realistic timeline for fast tracking business credit building:

TimelineWhat You Can ExpectMonth 1–2EIN set up, business entity active, first vendor accounts openedMonth 3–4Paydex score starts forming, 3–5 trade lines reportingMonth 5–6Business credit card approval likely, fundability scores improvingMonth 6–12Eligible for credit lines, working capital, and larger funding products

You don't need years to build usable business credit. With the right setup and consistent payments, many business owners see real progress within 90 to 180 days.

Common Mistakes to Avoid

Using your personal credit for everything. This doesn't build business credit at all. Keep business and personal finances separate.

Applying with inconsistent business information. If your business name is spelled differently on different applications, it can split your credit file or cause rejections.

Opening accounts that don't report to bureaus. Always confirm a vendor reports to at least one major business credit bureau before applying.

Ignoring your business credit reports. Errors happen. Check your reports regularly.

Giving up too early. Building business credit is a process. The first 90 days might feel slow. Stay consistent.

Frequently Asked Questions

How do I establish business credit quickly with no credit history? Start with Net-30 vendor accounts that report to business credit bureaus. You don't need existing credit to get approved for these. After 3–5 accounts report positive payment history, your business credit profile begins to form.

Can I build business credit without using my SSN? Yes. Once your business is properly set up as an LLC with an EIN, many vendor accounts and some credit products can be applied for using your EIN only. However, for larger credit products, some lenders may still require a personal guarantee early on.

What is the fastest way to build business credit? The fastest approach is to open 3–5 vendor accounts that report to D&B, Experian Business, or Equifax Business, pay every invoice early, and monitor your reports monthly. This can establish a working credit profile in 60–90 days.

How do I get my first business credit account? Apply for a starter Net-30 vendor account using your EIN and business details. Many office supply, shipping, or packaging vendors offer these with no credit check required. Once approved, make a purchase and pay early.

Does forming an LLC help build business credit? Yes. An LLC separates your business from your personal finances. It makes your business eligible for EIN-based credit accounts and signals to lenders that your business is a legitimate, separate entity.

What credit score do I need to get business funding? It depends on the lender and product. For starter vendor accounts, there's often no credit check. For business credit cards, a personal score of 650+ is often preferred. For larger working capital loans, lenders typically want a solid business credit profile in addition to revenue history.

Final Thoughts

Building business credit is one of the smartest moves a small business owner can make. It creates a financial identity for your business — completely separate from yours. And that identity is what lenders use to decide whether to give you access to real funding.

The steps aren't complicated. Set up your business correctly. Get your EIN and D-U-N-S number. Open a few vendor accounts. Pay them early. Monitor your reports. And keep growing your profile over time.

You don't need perfect credit to start. You just need to start.