Business Credit Building Strategy 2026 Altopex

Learn the best business credit building strategy for 2026. Step-by-step tips for new companies to build credit fast and get funded.

BUSINESS CREDIT

Russel

6/12/20268 min read

Most small business owners want funding. But when they apply, lenders say no.

Not because the business idea is bad. Not because the owner isn't working hard. The real reason? The business has no credit history.

That's the problem. And it happens to thousands of new companies every year.

Building business credit takes time — but only if you do it the wrong way. With the right business credit building strategy, you can move faster, look credible to lenders, and open doors to real funding within months.

This guide covers the best steps to build business credit in 2026, especially if your company is new or just getting started.

What Is Business Credit and Why Does It Matter in 2026?

Business credit is a credit profile tied to your business — not your personal Social Security Number (SSN). It's based on your EIN (Employer Identification Number), which is basically your business's tax ID.

When your business has strong credit, lenders, suppliers, and banks see you as low risk. That means better approval chances, higher credit limits, and more funding options.

In 2026, lenders are more careful. Banks look at your business profile before they look at your personal credit. If your business has no file — no trade lines, no credit history, nothing — most applications go nowhere.

That's why building business credit is not optional anymore. It's one of the most important things you can do as a small business owner.

Why Most New Businesses Struggle to Build Credit

Here's what usually happens.

You start an LLC. You get an EIN. You open a business bank account. Then you apply for a business credit card or a loan — and you get denied.

The reason is simple: lenders can't find your business.

They look up your EIN and find nothing. No credit history. No business address on file. No DUNS number. Nothing that tells them your business is real, established, and creditworthy.

This is called having a "thin file." And it's one of the biggest barriers for new companies trying to get funding.

The fix is not complicated. But you have to follow the right steps in the right order.

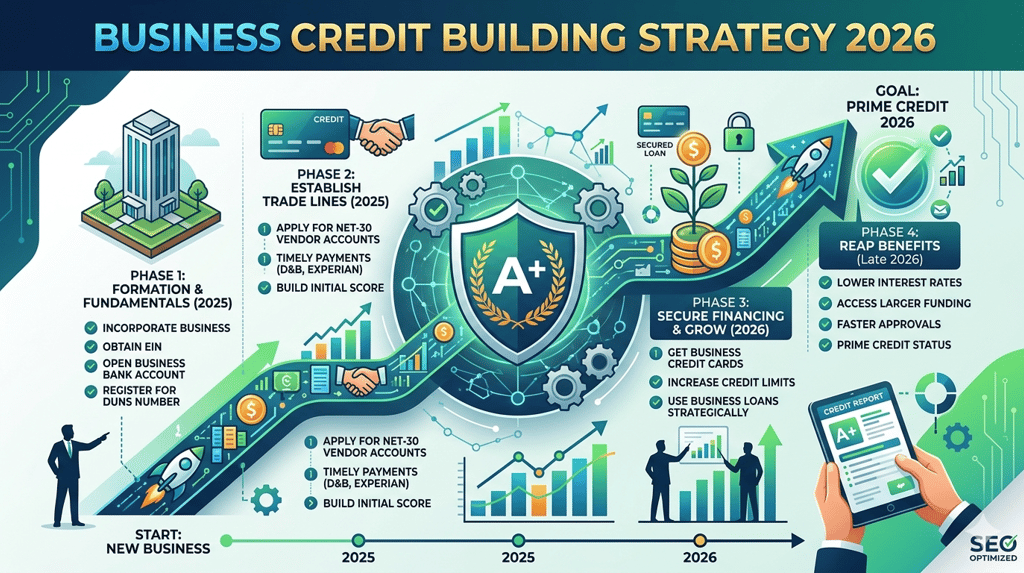

The Business Credit Checklist for New Businesses

Before you start building credit, make sure your business foundation is set up correctly. Lenders and credit bureaus verify your business information. If something doesn't match, it can hurt your credibility.

Here's the basic checklist every new business needs to complete first:

Register your business — Form an LLC or corporation. Sole proprietorships can't build business credit the same way.

Get your EIN — Apply for free at IRS.gov. This is your business identity number.

Open a dedicated business bank account — Don't mix personal and business money.

Get a business phone number — Listed under your business name, not your personal cell.

Set up a business address — A physical or registered address (not a P.O. Box if possible).

Register with D&B (Dun & Bradstreet) — Get your DUNS number. Most lenders use D&B to check business credit.

Register with Experian Business and Equifax Business — These are the main business credit bureaus.

Once these are in place, you're ready to start building.

Business Credit Building Strategy 2026: Step-by-Step

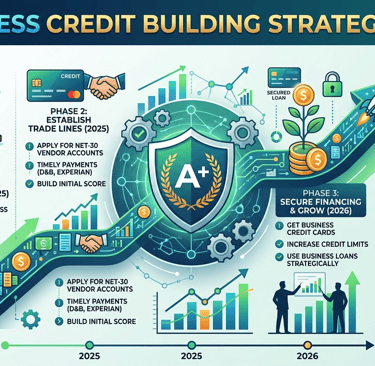

Step 1: Open Vendor Accounts (Trade Lines)

The fastest way to start building business credit is through vendor trade lines. These are accounts with suppliers who report your payment history to business credit bureaus.

Think of companies like Uline, Grainger, Quill, or Fleet Farm. Many of them offer Net-30 accounts — meaning you buy now and pay within 30 days. When you pay on time, they report it to the bureaus. That starts building your credit file.

This is the foundation of every smart business credit checklist for new businesses.

Start with 3 to 5 starter vendor accounts. Use them. Pay on time or early. Your credit file starts growing from there.

Step 2: Build Consistently Over Time

One of the most important business credit tips for new companies is this: consistency matters more than speed.

Lenders want to see a pattern. They want to know you pay on time, every time. Two or three months of clean payment history builds more trust than a rushed approach.

Make small purchases. Pay them off. Keep doing it.

Step 3: Apply for a Business Credit Card

Once you have a few vendor accounts reporting, you can apply for a business credit card. Cards like the Capital One Spark, Divvy, or BILL Divvy are known to approve newer businesses with limited credit history.

Use the card for regular business expenses. Keep your credit utilization low — that means don't use more than 30% of your credit limit. A lower utilization rate signals to lenders that you're managing credit well.

This is a key part of any fast track business credit building plan.

Step 4: Get a Business Line of Credit or Loan

Once you have 6 to 12 months of payment history, you're in a stronger position to apply for a business line of credit or a small working capital loan.

A business line of credit is a revolving credit option — meaning you borrow what you need, pay it back, and borrow again. It works like a credit card but with higher limits and lower interest rates.

Many lenders, including online lenders and credit unions, offer lines of credit for small businesses with at least one year of business history and a solid credit profile.

Step 5: Monitor Your Business Credit Scores

You can't manage what you don't track.

Check your business credit scores regularly on platforms like Nav.com, Dun & Bradstreet CreditSignal, and Experian Business. If something looks wrong — like a missing trade line or incorrect business info — you need to catch it early.

Many business owners lose funding opportunities because of simple reporting errors they never knew about.

How to Fast Track Business Credit Building in 2026

If you want to move faster, here are a few strategies that work well in 2026:

Use a credit-building service. Platforms like Altopex.com help you identify gaps in your credit profile, connect you with the right vendor accounts, and guide you through each step. This removes the guesswork.

Open multiple vendor accounts at once. Instead of one trade line, start with four or five in the first 30 to 60 days. More reporting accounts means your file builds faster.

Keep business finances completely separate. Every business transaction should go through your business bank account and business card. This shows lenders a clean, professional financial picture.

Pay early when possible. Paying before the due date shows lenders you're financially healthy, not just meeting minimums.

Avoid hard inquiries too early. Don't apply for loans or credit cards before your file is built. Multiple rejections can slow down your progress.

Common Mistakes That Slow Down Business Credit Building

Even business owners who are doing the right things sometimes make mistakes that hold them back.

Mixing personal and business finances is the most common one. If you're paying business expenses from your personal account, lenders can't see a clear business financial history.

Not registering with credit bureaus is another big problem. If you're not registered with D&B, Experian Business, or Equifax Business, your payments may not be reported — meaning your credit file doesn't grow.

Applying for too much credit too soon can hurt you. Each hard inquiry on your file can lower your score. Build first, apply later.

Ignoring your business credit scores means problems can pile up without you knowing. Check your scores at least once a month.

What Lenders Look for in 2026

Lenders have gotten smarter. They're not just checking your personal credit score anymore. Before approving business funding, many lenders now review:

Your business credit scores (Paydex, Experian Intelliscore, FICO SBSS)

Time in business and business bank account history

Revenue consistency over the last 3 to 6 months

Existing debt levels and open credit accounts

Whether your business information is consistent across all records

The more of these boxes you check, the better your chances.

A strong business credit building strategy addresses all of these areas — not just one.

Business Credit vs. Personal Credit: Know the Difference

Many small business owners think their personal credit score is enough. It's not.

Personal credit is tied to your SSN. It reflects your personal financial life — mortgage, car loans, personal cards. Lenders look at this for personal loans.

Business credit is tied to your EIN. It reflects your company's financial behavior. This is what business lenders check when you apply for a business line of credit, trade account, or working capital loan.

When you build strong EIN credit, you separate your personal finances from your business. That protects your personal credit and gives your business its own financial identity.

This separation is one of the smartest moves a small business owner can make.

Real Example: How a New LLC Built Credit in 90 Days

Here's a real-world example of how this works.

A new LLC registered in Texas — 3 months old, no credit history — followed these steps:

Registered with D&B and got a DUNS number in week one.

Applied for four Net-30 vendor accounts (Uline, Quill, Crown Office Supplies, and Summa Office Supplies).

Made small purchases with each vendor and paid on time.

After 60 days, applied for a Divvy business credit card and got approved.

At 90 days, the business had a Paydex score of 80 and two open credit accounts.

By month six, the business applied for a $25,000 business line of credit — and got approved.

That's what a smart fast track business credit building plan looks like in practice.

FAQ: Business Credit Building Strategy 2026

Q: How long does it take to build business credit?

You can start seeing results in 60 to 90 days if you follow the right steps. A solid credit profile typically takes 6 to 12 months to build fully.

Q: Can I build business credit with a new LLC?

Yes. In fact, forming an LLC is one of the first steps. You need a registered business entity to build credit under your EIN.

Q: Do I need good personal credit to build business credit?

Not always. Many vendor trade lines and starter business credit cards approve based on your business profile, not personal credit. However, for larger loans, lenders may still check your personal score.

Q: What is a DUNS number and do I need one?

A DUNS number is a unique 9-digit identifier issued by Dun & Bradstreet for your business. Most lenders and vendors use it to check your business credit. Yes — you need one. It's free to register.

Q: What is a Paydex score?

Paydex is Dun & Bradstreet's business credit score. It ranges from 0 to 100. A score of 80 or above means you pay on time. A score of 100 means you pay early. Most lenders want to see at least an 80.

Q: How many trade lines do I need to build business credit?

Starting with 3 to 5 trade lines is enough to begin building your file. Over time, having 7 to 10 active accounts strengthens your profile significantly.

Q: Is it possible to get business funding with no credit history?

It's difficult, but not impossible. Some lenders offer startup loans based on business revenue or personal credit. However, building business credit first puts you in a much stronger position.

Final Thoughts: Start Your Business Credit Strategy Today

Building business credit is one of the smartest investments you can make in your company's future.

It takes some time. It takes consistency. But when it's done right, it gives your business real financial power — higher credit limits, better funding options, and the ability to grow without depending on your personal credit.

The best steps to build business credit are not complicated. Register your business. Set up your profile. Open vendor accounts. Pay on time. Monitor your scores. Repeat.

The key is starting — and staying consistent.

If you're ready to build your business credit the right way and want a clear plan tailored to your situation, Altopex.com can help you get there step by step. From setting up your credit foundation to accessing real funding options, we guide small business owners through the entire process.

Reach out to Altopex.com today and let's build something solid together.

Written for US small business owners by the Altopex.com content team. For more business credit and funding resources, visit Altopex.com.