Business Credit Profile Setup Guide for Small Business Owners

Learn how to set up your business credit profile the right way. Step-by-step guide for US small business owners to open a credit file and start building fundability.

BUSINESS CREDIT

Russel

5/30/20268 min read

Most small business owners don't think about business credit until they need funding — and by then, it's already a problem.

You apply for a business loan or a business credit card. The lender checks your business credit. There's nothing there. No file. No score. No history. So you either get denied or you end up using your personal credit to cover business expenses.

That's not where you want to be.

Setting up your business credit profile the right way — from the very beginning — changes how lenders see your business. It separates your personal finances from your business. And it opens the door to funding that doesn't touch your personal credit score.

This guide walks you through exactly how to do that. Step by step. No fluff.

What Is a Business Credit Profile?

A business credit profile is your business's financial identity. Think of it like a personal credit report — but for your company.

It shows lenders, vendors, and creditors how your business handles money. It includes things like:

Payment history with vendors and suppliers

Business loan repayment records

Credit utilization on business credit cards

Public records like liens or judgments

When lenders evaluate your business for funding, they check this profile. If it's empty or weak, your chances of approval drop — fast.

The good news? You can build it. And you don't need years of business history to get started.

Why Your Business Needs a Separate Credit Profile

Here's something many new business owners get wrong. They assume their personal credit covers everything. It doesn't.

Personal credit and business credit are two separate systems. Two different bureaus track them. Two different scoring models apply.

The major business credit bureaus in the US are:

Dun & Bradstreet (D&B) — tracks your PAYDEX score

Experian Business — tracks business payment and credit history

Equifax Business — monitors business financial behavior

These bureaus don't automatically pull your personal credit history. They build your business credit file based on what gets reported to them — vendor accounts, business loans, credit cards opened under your EIN.

If nothing is reported, your file is blank. And a blank file is almost as bad as a bad one.

Business Credit Profile Setup Guide: Step-by-Step

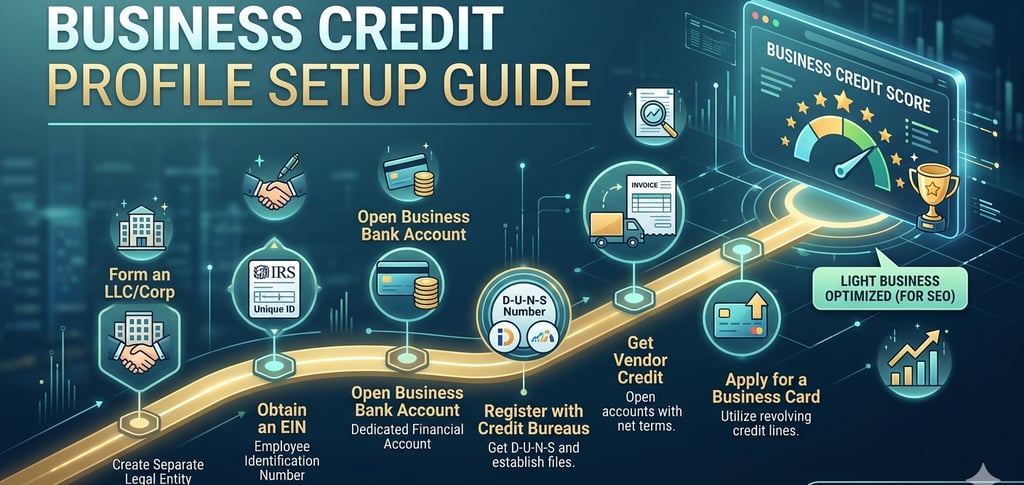

Step 1 — Set Up Your Business as a Legal Entity

This is where everything starts. Your business needs to exist as a real legal entity — not just a name you use.

The most common option for small business owners is an LLC (Limited Liability Company). An LLC gives your business a separate legal identity. That's important because it separates your personal liability from your business debts.

Register your LLC with your state. Each state has its own process, but most can be done online in a few hours.

Once your business is registered, you're ready for the next step.

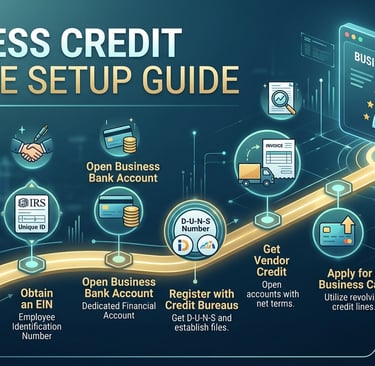

Step 2 — Get Your EIN (Employer Identification Number)

Your EIN is your business's version of a Social Security Number. It's what you use to open a business bank account, apply for business credit, and file business taxes.

Getting an EIN is free. You apply directly on the IRS website at IRS.gov. Most applicants get their EIN the same day.

One important thing: make sure you apply under your business name — not your personal name. This matters when you're building credit under your EIN.

Step 3 — Open a Business Bank Account

Lenders and vendors want to see that your business operates like a real business. One of the first signs is a dedicated business bank account.

Don't use your personal account for business income and expenses. It blurs the line between you and your business — and that can hurt your fundability later.

When opening your account, use your:

Business legal name

Business address

EIN (not your SSN)

Keep the account active. Run your business income through it. Lenders often ask for 3 to 6 months of business bank statements when you apply for funding.

Step 4 — Get a DUNS Number

Dun & Bradstreet is one of the biggest business credit bureaus in the US. To have a file with D&B, your business needs a DUNS number — a unique 9-digit identifier.

Getting a DUNS number is free. You register at Dun & Bradstreet's website. Once registered, D&B creates a basic business credit file for your company.

This is how you officially open a business credit file with one of the major bureaus. Without this step, many vendors and lenders won't even be able to look up your business.

Step 5 — Make Sure Your Business Information Is Consistent

This step is simple but often overlooked. And it causes real problems.

Your business name, address, and phone number must match everywhere. That means:

Your state registration

IRS records (EIN)

Your business bank account

Your business website

Any directories or listings (Google Business, Yelp, etc.)

This consistency is called your business profile credibility. Lenders and bureaus cross-check this information. Inconsistencies can slow down your credit building or raise red flags during a funding application.

Step 6 — Open Vendor Accounts That Report to Business Credit Bureaus

Here's where your business credit profile actually starts to grow.

Vendor accounts — also called net-30 accounts or trade lines — let you buy products or services now and pay within 30 days. When you pay on time, the vendor reports your payment to business credit bureaus. That builds your score.

Not all vendors report. You need to focus on ones that do. Some well-known starter vendors that report include:

Uline (shipping and packaging supplies)

Quill (office supplies)

Grainger (business tools and safety supplies)

Crown Office Supplies

Start with 3 to 5 vendor accounts. Make small purchases. Pay before the due date. Let the positive payment history stack up over time.

Most business owners see their first credit scores appear after 3 to 6 months of consistent reporting.

Step 7 — Apply for a Business Credit Card

Once you have a few vendor accounts reporting, you can start looking at business credit cards.

A business credit card gives your business a revolving line of credit. This is important because it shows lenders that your business can manage an open line of credit responsibly.

When applying, look for cards that:

Report to business credit bureaus (not just personal)

Don't require a personal guarantee (harder to get early on, but worth knowing about)

Offer rewards you can use for your business needs

Use the card for regular business expenses. Keep your credit utilization — that's the percentage of your credit limit you're using — below 30%. Paying it in full each month is even better.

Step 8 — Monitor Your Business Credit Reports

Building credit is one thing. Watching it is another.

Check your business credit reports regularly. You can access them through:

Dun & Bradstreet — for your PAYDEX score

Nav.com — shows all three major bureau scores in one place

Experian Business — for their specific report

Look for errors. Incorrect information can drag your score down. If something is wrong, dispute it through the bureau directly.

Monitoring your profile also helps you know when you're ready to apply for larger funding — like a working capital loan or business line of credit.

Business Credit Checklist for New Business Owners

Use this as your starting point. Check off each item as you complete it.

Business registered as an LLC or Corporation

EIN obtained from IRS.gov

Business bank account opened (using EIN)

Business address and phone number set up

DUNS number registered with Dun & Bradstreet

Business information consistent across all platforms

3 to 5 vendor accounts opened (with reporting to bureaus)

Business credit card applied for and activated

Business credit reports monitored monthly

If you can check all of these off, your business credit profile is moving in the right direction.

Common Mistakes That Slow Down Business Credit Building

Using Personal Credit Instead of Building Business Credit

This is the most common mistake. Every time you use your personal credit for business expenses, you're missing a chance to build your business profile. It also increases your personal debt, which can hurt your personal score.

Skipping the DUNS Number

Some business owners open vendor accounts but never register with D&B. If D&B doesn't have a file on your business, a big chunk of your credit history gets lost.

Inconsistent Business Information

Even small differences — like "LLC" vs "L.L.C." or using a personal address instead of a business address — can cause problems. Bureaus and lenders match records precisely.

Applying for Too Much Credit Too Fast

Applying for multiple credit lines in a short period raises red flags. Build slowly. Let your profile strengthen before you go after bigger funding.

How Long Does It Take to Build a Business Credit Profile?

Realistically, expect 6 to 12 months to build a solid business credit profile from scratch.

Here's a rough timeline:

TimeframeWhat to ExpectMonth 1–2Business setup, EIN, bank account, DUNS numberMonth 3–4First vendor accounts open and reportingMonth 5–6Business credit scores start appearingMonth 6–12Scores strengthen, business credit cards become accessibleMonth 12+Ready to pursue working capital loans and larger credit lines

This is not a fast process. But every month you delay getting started is a month you add to the clock.

What Lenders Actually Look at Before Approving Business Funding

When you apply for a business loan or line of credit, lenders typically check:

Business credit scores (PAYDEX, Experian Business, Equifax Business)

Time in business (most want at least 6 to 12 months)

Business bank account history (average daily balance, revenue deposits)

Business fundability (how complete and verifiable your business profile is)

The stronger your business credit profile, the better your funding options. Many lenders offer lower interest rates and higher limits to businesses with strong credit history.

Frequently Asked Questions

What is a business credit profile setup guide?

A business credit profile setup guide is a step-by-step process that helps business owners create, build, and strengthen their business credit file with major credit bureaus like Dun & Bradstreet, Experian, and Equifax. It covers everything from registering your business to opening vendor accounts that report payment history.

How do I open a business credit file?

To open a business credit file, you need to register your business as an LLC or corporation, get an EIN from the IRS, and register for a DUNS number with Dun & Bradstreet. Once your file exists, you build it by opening vendor accounts and credit lines that report to business bureaus.

What are business credit basics for small business owners?

Business credit basics include understanding that your business has a separate credit identity from you personally. It's built through your EIN, vendor payment history, business credit cards, and business loans — all reported to business credit bureaus, not personal ones.

Can I build business credit with no personal credit check?

Yes. There are starter vendor accounts — like Uline, Quill, and Grainger — that approve new businesses without a hard personal credit pull. These are often the first step for business owners who want to build business credit independently from their personal credit.

How long does it take to build a business credit score?

Most businesses start seeing their first business credit scores after 3 to 6 months of consistent vendor account activity. A strong, fundable business credit profile typically takes 6 to 12 months to develop.

What is a DUNS number and do I need one?

A DUNS number is a unique 9-digit identifier assigned by Dun & Bradstreet. It's free to get and creates your business credit file with one of the largest business credit bureaus. Most serious lenders and vendors check D&B, so having a DUNS number is an important early step.

Final Thoughts

Building your business credit profile is not complicated. But it does require the right steps, done in the right order.

If you skip the foundation — the LLC, the EIN, the DUNS number, the consistent business information — the whole thing falls apart later. Lenders can't verify your business. Vendors won't report your payments. And you'll end up back where you started.

Start now. Even if your business is brand new. The earlier you set this up, the faster you'll have real funding options that don't depend on your personal credit.

If you want help setting up your business credit profile the right way, Altopex.com can guide you through every step — from registering your business to accessing funding that actually fits your goals.

This article was written for US small business owners looking to build business credit and access funding. For personalized guidance, visit Altopex.com.