Simple Steps for Business Credit Approval

Learn the simple steps for business credit approval that most small business owners skip. Build business credit fast and get approved for funding in 2026.

BUSINESS CREDIT

Russel

6/10/20269 min read

Getting approved for business credit is not as hard as most people think. But it does require the right steps in the right order.

Most small business owners apply for business credit cards or funding and get denied — not because their business is failing, but because their business profile is not set up correctly. Lenders look at specific things before approving you. If those things are missing, you don't get approved. It's that simple.

This guide breaks down the simple steps for business credit approval so you can stop guessing and start building.

Why Most Business Credit Applications Get Denied

Before getting into the steps, let's talk about the real reason most applications fail.

It's rarely about revenue alone. Many businesses with solid income still get denied because:

Their business is not legally separated from their personal finances

They have no business credit history at all

Their business contact information doesn't match what's on file with lenders and reporting agencies

They applied too soon — before their business profile was ready

Lenders don't just look at your bank balance. They look at your business identity, your business credit profile, and how long your business has been operating as a legitimate entity.

If those things aren't in order, approval is unlikely — no matter how good your personal credit is.

Step 1 — Set Up Your Business the Right Way

The first of the simple steps for business credit approval starts before you ever apply for anything.

Your business needs to exist as a real, separate entity. That means:

Form an LLC or Corporation A sole proprietorship ties everything back to your personal name. An LLC (Limited Liability Company) or corporation creates a separate legal identity for your business. Most lenders and vendors require this before they extend credit.

Get an EIN from the IRS An EIN — Employer Identification Number — is like a Social Security Number for your business. You use it to open business bank accounts, apply for credit, and file taxes as a business entity. You can get one free from the IRS website. This is a foundational step.

Set Up a Business Address and Phone Number Your business should have a dedicated address (not just your home address mixed in everywhere) and a business phone number. When lenders verify your business, they check public records. If your info is inconsistent or hard to find, that creates doubt.

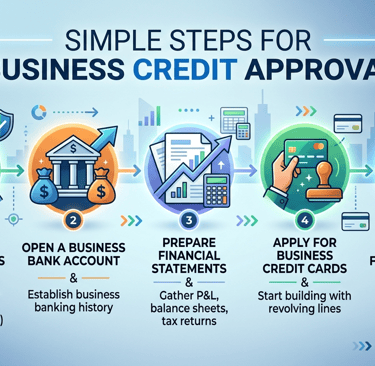

Get a Business Checking Account You need a business bank account in your business name, using your EIN. This separates your personal and business finances and shows lenders your business is operating independently.

These are not optional extras. This is the foundation lenders check before anything else.

Step 2 — Build Your Business Credit Profile from Scratch

Here's something many new business owners don't know: your business starts with zero credit history. No file. Nothing.

Before any lender can approve you for significant funding, they need to see a business credit profile — a record of how your business handles credit obligations. That profile is built over time through specific types of accounts.

Start with Vendor Accounts (Net-30 Accounts) Vendor accounts — sometimes called net-30 accounts — are credit accounts with suppliers and vendors where you buy now and pay in 30 days. Many vendors don't require a personal credit check to open these accounts. When you pay on time, they report that payment history to business credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business.

This is how you start building a real business credit history fast.

Good starter vendor accounts include office supply companies, shipping providers, and business product suppliers that report to credit bureaus.

Apply for a DUNS Number Dun & Bradstreet is one of the main business credit reporting agencies. Your DUNS number is your unique identifier in their system. You can register for one free. Once you have active vendor accounts reporting, your business credit score starts building through D&B.

Monitor Your Business Credit Reports Keep an eye on what's being reported. Check Dun & Bradstreet, Experian Business, and Equifax Business separately. Errors on these reports can hurt your approval chances just like personal credit report errors hurt personal loan applications.

Step 3 — Make Sure Your Business Information Is Consistent Everywhere

This step sounds small. It's actually a big reason why many easy business credit approval steps get skipped — and why applications fail.

Lenders and credit agencies verify your business by checking multiple sources:

Secretary of State records

Google Business listings

411 directories

Business websites

The IRS (through your EIN)

If your business name, address, or phone number is listed differently across these sources, it raises red flags. It looks like your business might not be legitimate, even if it is.

Before you apply for anything, make sure your business information is identical everywhere it appears online and in official records. This is called business credibility — and it matters more than most people realize.

Step 4 — Open Business Credit Accounts Strategically

Once your foundation is solid and you have some vendor account history reporting, you can start applying for business credit cards and other revolving credit.

Here are practical business credit approval tips for beginners:

Start with Store or Gas Cards Business credit cards from gas stations and office supply stores are often easier to get approved for when your business credit is new. Use them for small purchases and pay them off each month.

Apply for Cards That Report to Business Bureaus Not all business credit cards report to business credit agencies. Make sure the ones you apply for report to Dun & Bradstreet, Experian Business, or Equifax Business. That way, your on-time payments keep building your score.

Keep Credit Utilization Low Credit utilization means how much of your available credit you're actually using. If your business card has a $5,000 limit and you're using $4,000 of it, that's 80% utilization — which looks risky to lenders. Try to keep it under 30%. This alone can significantly improve your business credit score.

Don't Apply for Too Many Cards at Once Every time you apply for credit, there's a hard inquiry on your record. Multiple applications in a short time can look desperate to lenders and can actually lower your score temporarily. Be strategic.

Step 5 — Know How to Get Approved for Business Credit Cards

If your question is specifically how to get approved for business credit cards, here's what lenders actually look for:

Business age — Most cards want to see at least 6–12 months of business operation. Some newer fintech lenders work with businesses as young as 3 months.

Business revenue — Even modest monthly revenue helps. Some cards ask for annual revenue figures on the application.

EIN on file — Applying with your EIN instead of your SSN shows you're operating as a real business entity.

Business credit history — Even a short history with a few on-time vendor accounts helps a lot.

Personal credit score — For most business credit cards, especially early on, lenders still check your personal credit. A score above 680 improves your odds significantly.

The goal over time is to build enough business credit history that you can eventually qualify based on business credit alone — without relying on your personal score.

Step 6 — Use a Business Credit Checklist Before Every Application

One of the most practical business credit approval tips is this: don't apply randomly. Run through a checklist first.

Before applying for any business credit card or funding product, confirm:

✅ My business is registered as an LLC or corporation

✅ I have an active EIN from the IRS

✅ My business has a dedicated phone number and address

✅ My business information matches across all public directories

✅ I have a business bank account open and active

✅ I have at least 2–3 vendor accounts reporting to business credit bureaus

✅ My business credit score is active and shows positive payment history

✅ My personal credit score is above 650 (ideally 680+)

✅ I have not applied for multiple credit products in the last 30–60 days

If you can check every one of those boxes, your approval chances improve significantly. If several are missing, it's worth taking a few weeks to fix them before applying.

Step 7 — Scale Up to Larger Funding

Once you've built a solid business credit profile over 6–12 months, you're in a much stronger position to apply for:

Business Lines of Credit A revolving credit line — meaning credit you can use, repay, and use again — gives your business flexible access to working capital. Many lenders offer these to businesses with established credit histories and consistent revenue.

SBA Loans and Working Capital Loans SBA loans (backed by the Small Business Administration) are some of the best funding options for small businesses. They offer lower interest rates and longer repayment terms. But they require a solid business credit profile and a reasonable amount of time in business.

Unsecured Business Loans Once your business credit is strong enough, you may qualify for unsecured funding — loans that don't require collateral. These are harder to get but very valuable for growth.

The key is patience and consistency. Lenders want to see a business that pays on time, operates as a real entity, and has a track record — even a short one.

Common Mistakes That Kill Business Credit Approval

Even when business owners follow most of these steps, a few common mistakes still cause problems:

Mixing personal and business finances — Using personal accounts for business expenses makes it harder to separate your financial identity. Always use business accounts for business spending.

Ignoring business credit reports — Many owners never check their business credit reports. Errors and missing information are more common than you'd expect.

Applying before the foundation is ready — Applying for credit cards or loans before your business profile is set up just results in denials that sit on your record.

Not paying vendor accounts on time — The whole point of vendor accounts is building positive payment history. One missed payment can slow your progress.

Giving up after one denial — A denial doesn't mean no forever. It usually means not yet. Fix what's missing and reapply after 3–6 months.

How Long Does It Take to Build Business Credit?

This is a common question. The honest answer is 6–12 months to build a solid foundation, if you follow the right steps consistently.

Here's a rough timeline:

Month 1–2: Set up your business entity, EIN, bank account, and business profile

Month 2–4: Open 3–5 vendor accounts and start building payment history

Month 4–6: Apply for starter business credit cards, monitor your business credit scores

Month 6–12: Apply for higher-limit cards, business lines of credit, and eventually working capital loans

Some lenders and fintech companies now work with businesses as young as 3 months old if your profile is set up correctly. But for traditional lenders and larger funding amounts, 12+ months of history is more realistic.

Conclusion — Take the Right Steps, Then Take Action

Business credit approval is not about luck. It's about preparation.

When you follow the simple steps for business credit approval — forming your business correctly, building vendor account history, keeping your profile consistent, and applying strategically — the results come. Lenders see a legitimate, creditworthy business and respond accordingly.

Most small business owners skip 2 or 3 of these steps and wonder why they keep getting denied. Now you know what those steps are.

If you want help setting up your business credit profile the right way and getting access to funding faster, Altopex.com is here to guide you. We work with US small business owners at every stage — from brand new LLCs to growing businesses that need serious capital.

Reach out today and let's build your business credit the right way.

Frequently Asked Questions

What are the simple steps for business credit approval? The core steps are: form an LLC or corporation, get an EIN, open a business bank account, set up consistent business contact information, open vendor accounts that report to business credit bureaus, and apply for business credit cards strategically once your profile is active.

How do I start building business credit with no history? Start with net-30 vendor accounts from suppliers that report to Dun & Bradstreet, Experian Business, or Equifax Business. Pay on time every month. After 2–3 active accounts, your business credit profile starts building automatically.

Can I get approved for a business credit card with a new business? Yes, but your options are more limited. Many starter business credit cards still check personal credit. With a personal score above 650–680 and a properly set-up business entity, approval for entry-level business credit cards is possible even in your first year.

Do I need a DUNS number to build business credit? A DUNS number from Dun & Bradstreet is important because D&B is one of the main business credit bureaus. Once you have vendors reporting to D&B, your DUNS number ties all that activity to your business profile. You can register for one free at the D&B website.

How long does it take to get a good business credit score? With consistent effort — active vendor accounts, on-time payments, and low credit utilization — most businesses can reach a solid business credit score within 6–12 months. Some lenders consider newer businesses with strong profiles after just 3–6 months.

What is credit utilization and why does it matter for business credit? Credit utilization is the percentage of your available credit that you're currently using. If you have a $10,000 credit limit and owe $7,000, your utilization is 70% — which looks risky. Keeping it under 30% shows lenders your business manages credit responsibly and can improve your approval chances significantly.

Can I build business credit without using my SSN? Over time, yes. Once your business has enough credit history under its EIN, many lenders will evaluate your business on its own merits. But in the early stages, most business credit cards still use a personal guarantee and check personal credit as a backup.

Published by Altopex.com — Helping US small business owners build business credit and access the funding they need to grow.