How to Fix Business Credit Score Fast (And Actually Get Approved for Funding)

Learn how to fix business credit score fast with simple, proven steps. Improve your score quickly and unlock better funding options for your small business.

BUSINESS CREDIT

Douglas G. Marsh

5/21/20267 min read

Your business credit score is low. Lenders keep saying no. And you need funding to keep things moving.

That's a real problem. And it's more common than most business owners realize.

The good news? You can fix your business credit score faster than you think. Not overnight — but with the right steps, you can see real improvement in 30 to 90 days. Sometimes even sooner.

This guide breaks it all down. Simple steps. No fluff. Just what actually works.

Why Your Business Credit Score Is Hurting You

Before fixing it, you need to understand what's pulling your score down.

Business credit scores work differently from personal credit. Your business has its own credit profile — separate from yours — built with agencies like Dun & Bradstreet, Experian Business, and Equifax Business.

These agencies track how your business pays its bills, how much credit it uses, and how long it's been in operation.

When your score is low, lenders see risk. That means higher interest rates, lower limits, or flat-out denials. Even vendors may hesitate to extend payment terms.

A weak business credit score can quietly block your growth without you even realizing it.

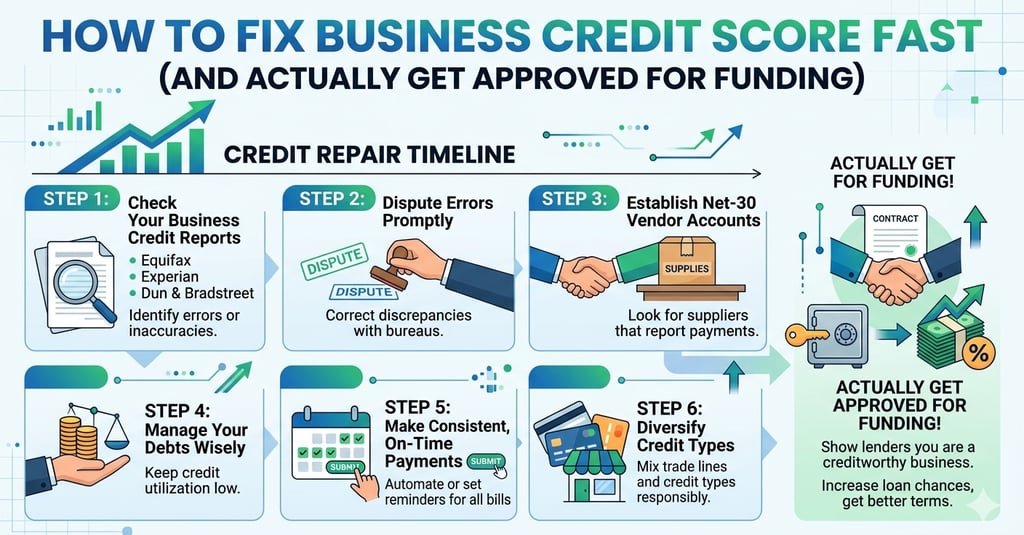

Step 1: Check Your Business Credit Reports First

You can't fix what you don't know about.

Pull your business credit reports from all three major bureaus — Dun & Bradstreet, Experian Business, and Equifax Business. Each one may show different information.

Look for:

Errors or accounts that don't belong to you

Late payment records that are wrong

Old negative items that should have fallen off

Accounts with incorrect credit limits

Mistakes on business credit reports are more common than most people expect. And they directly hurt your score.

If you find errors, dispute them immediately. Write a formal dispute letter to the bureau and include proof. This alone can give your score a noticeable boost if the error is significant.

Don't skip this step. It's one of the fastest ways to get a quick business credit improvement.

Step 2: Make Sure Your Business Is Set Up Correctly

This surprises a lot of business owners.

Your business setup affects your credit score. If your business isn't properly registered, lenders and credit bureaus can't evaluate it correctly.

Here's what you need in place:

An EIN (Employer Identification Number) — This is your business's tax ID, like a Social Security number for your company. All credit should be built under this number, not your personal SSN.

A registered LLC or Corporation — Your business needs to be a legal entity. Sole proprietorships are harder to build business credit under.

A dedicated business bank account — Keep business money completely separate from personal money. This matters to lenders.

A business address and phone number — A real business address (not a P.O. Box) and a listed business phone number signal legitimacy to credit bureaus.

A professional business email and website — These seem small, but they affect how credible your business looks to lenders.

If any of these are missing, fix them now. A properly set-up business is the foundation everything else builds on.

Step 3: Get a D-U-N-S Number (If You Don't Have One)

Dun & Bradstreet is one of the most important business credit bureaus. To have a credit profile with them, your business needs a D-U-N-S number.

It's free. You can register directly on the Dun & Bradstreet website.

Once you have a D-U-N-S number, you can start building credit with D&B vendors and suppliers who report to them. Without it, those payments never show up on your profile.

This is a fast, easy step that many small business owners overlook. Don't be one of them.

Step 4: Open Vendor Accounts That Report to Credit Bureaus

Here's one of the most effective methods for quick business credit improvement — and most business owners don't know about it.

Vendor accounts (also called net-30 accounts or trade lines) let you buy products or services now and pay within 30 days. When you pay on time, the vendor reports that positive payment to the business credit bureaus.

This builds your credit history fast.

Some vendors that are known to report to business credit bureaus include:

Uline (shipping and business supplies)

Quill (office supplies)

Grainger (industrial and business supplies)

Crown Office Supplies

Summa Office Supplies

Start with 3 to 5 of these. Make small purchases. Pay early or on time every single time.

Each on-time payment is a positive mark on your credit profile. Stack enough of them and your score starts moving up.

Step 5: Lower Your Credit Utilization

Credit utilization means how much of your available credit you're using. If you have a $10,000 credit line and you're using $8,000 of it, your utilization is 80%. That's too high.

Business credit bureaus want to see utilization under 30%. Ideally under 15% if you want a strong score.

High utilization signals that your business is stretched thin financially. Lenders see that as a red flag.

To lower your utilization:

Pay down existing balances as fast as possible

Ask your current lenders for credit limit increases

Spread spending across multiple accounts

Even a drop from 70% to 40% utilization can have a meaningful impact on your score fairly quickly.

Step 6: Pay Every Bill on Time — Or Early

This sounds obvious. But payment history is the single biggest factor in your business credit score.

One late payment can drag your score down significantly. And business credit bureaus track this closely.

Set up automatic payments wherever possible. Use calendar reminders. Whatever it takes.

If you have any past-due accounts, get them current immediately. The damage from a late payment starts to fade over time once you establish a strong record of on-time payments after it.

Lenders want to see consistency. Show them you pay your bills. That's how trust gets built.

Step 7: Open a Business Credit Card and Use It Strategically

A business credit card is one of the best tools for building credit fast — as long as you use it the right way.

Use it for regular business expenses. Pay the balance in full each month. Keep utilization low.

Look for cards that report to business credit bureaus (not all of them do). Cards from American Express, Capital One, and similar issuers typically report to business credit agencies.

Over time, responsible use of a business credit card adds positive payment history and increases your available credit — both of which improve your score.

Start with whatever you can qualify for. Even a secured business credit card counts.

Step 8: Don't Apply for Too Much Credit at Once

When you apply for credit, it creates a hard inquiry on your profile. Too many hard inquiries in a short time period tells lenders you might be desperate for credit. That hurts your score.

Be strategic. Apply for one or two accounts at a time. Wait 60 to 90 days before applying for more.

Focus on building a solid foundation first. Once your score improves, better credit products become available anyway.

Step 9: Monitor Your Business Credit Regularly

You can't improve what you're not watching.

Check your business credit reports every 30 to 60 days while you're in improvement mode. Look for new errors, verify that positive accounts are reporting correctly, and track your progress.

Services like Nav, CreditSafe, and the direct bureau portals let you monitor your business credit. Some are free, some charge a small fee.

Staying on top of your credit profile means you catch problems early — before they cause serious damage.

How Long Does It Take to Fix Business Credit?

This is the question everyone asks.

The honest answer: it depends on where you're starting from.

If your score is low because of errors, fixing those can improve things in 30 to 45 days.

If you're starting with no credit history, building a solid profile typically takes 3 to 6 months of consistent positive activity.

If you have serious negative items like collections or charge-offs, those take longer to recover from — but consistent positive behavior still moves the needle over time.

The key is to start now. Every month you wait is a month of positive history you're not building.

What Happens When Your Business Credit Improves?

The real question is: what becomes possible?

When your business credit score moves up, you gain access to:

Higher credit limits from vendors and lenders

Better interest rates on business loans

Easier approval for working capital loans and business credit cards

Net-30 and net-60 payment terms with suppliers

More funding options in general

Strong business credit puts your company in a completely different position. You stop getting told no. You start having choices.

That's the real value of fixing your business credit score fast.

Common Mistakes That Slow Down Business Credit Improvement

Watch out for these. They're more common than you'd think.

Mixing personal and business finances. This creates confusion for lenders and doesn't help build a separate business credit profile.

Only applying to vendors that don't report. If a vendor doesn't report to credit bureaus, those payments don't build your score.

Ignoring errors on your credit report. Small mistakes left uncontested can keep dragging your score down.

Applying for too many accounts too fast. Multiple hard inquiries signal desperation, not growth.

Giving up too early. Business credit building requires consistency. Some business owners quit after a month or two and miss the progress that was coming.

FAQ: How to Fix Business Credit Score Fast

How fast can I improve my business credit score? With the right steps — fixing errors, opening reporting vendor accounts, and lowering utilization — you can see noticeable improvement in 30 to 90 days.

Can I build business credit without using my personal credit? Yes. Once your business is properly set up with an EIN and legal structure, you can build credit under your business identity without relying on your personal SSN.

What's the fastest way to build business credit from scratch? Start with a D-U-N-S number, open 3 to 5 vendor accounts that report to credit bureaus, and pay everything on time. This is the fastest foundation you can build.

Does a business credit score affect loan approval? Absolutely. Most business lenders review your business credit score as part of the approval process. A higher score means better terms and higher approval chances.

What credit score do I need to get a business loan? It depends on the lender. Many traditional lenders want to see a Paydex score of 80 or above (Dun & Bradstreet's scoring system). Alternative lenders may accept lower scores but charge higher rates.

Can I dispute errors on my business credit report? Yes. You can dispute errors directly with each business credit bureau. You'll need to submit documentation to support your dispute.

Take Action Now — Don't Let Your Credit Score Hold Your Business Back

Low business credit is a fixable problem. It's not permanent. And it doesn't have to keep blocking your growth.

The steps in this guide work. They're the same methods used by business owners who went from getting denied to getting approved — for working capital loans, business credit cards, vendor lines, and more.

Start today. Fix the errors. Set up your business correctly. Build your vendor accounts. Pay on time.

Every step you take now is an investment in your business's financial future.

If you want expert guidance on improving your business credit score and accessing the right funding, Altopex.com is here to help. We work with US small business owners at every stage — from brand-new startups to established businesses that just need a stronger credit profile. Reach out and let's map out the right plan for your business.