Business Credit Checklist for New Business (2026 Guide)

Follow this simple business credit checklist for new business owners. Set up your credit profile the right way and improve your chances of getting funding.

Russel

6/3/20269 min read

Most New Business Owners Skip This — And It Costs Them Later

You started your business with a plan. You got clients. Maybe you are already making money.

But when you go to apply for funding — a business credit card, a working capital loan, a vendor account — you hit a wall.

"We couldn't find a credit profile for your business."

That one sentence stops a lot of small business owners cold. And the frustrating part is, it did not have to happen.

The truth is simple: business credit does not build itself. You have to set it up the right way, from the very beginning. And most new business owners never get a clear checklist showing them exactly what to do.

This guide fixes that.

Below is a complete business credit checklist for new businesses — from the basics of business credit to building a real credit profile that lenders and vendors can actually find.

What Is Business Credit (And Why It Matters for Funding)?

Before we get into the checklist, let's make sure we are on the same page about what business credit actually is.

Business credit is a credit profile tied to your business — not to you personally. It is built under your business name, your Employer Identification Number (EIN), and your business address.

When your business has strong credit, lenders see it as a separate financial entity. That means you can potentially get:

Business credit cards with higher limits

Trade lines from vendors (net-30 accounts that report to credit bureaus)

Working capital loans without needing to put your personal credit on the line

Better approval odds on business funding in general

If your business has no credit profile, most lenders either deny you outright or fall back to your personal credit. That is not ideal — especially if your personal credit is not perfect, or if you simply do not want to mix business and personal finances.

Building business credit the right way takes time. But following a clear setup process gives your business the best possible foundation.

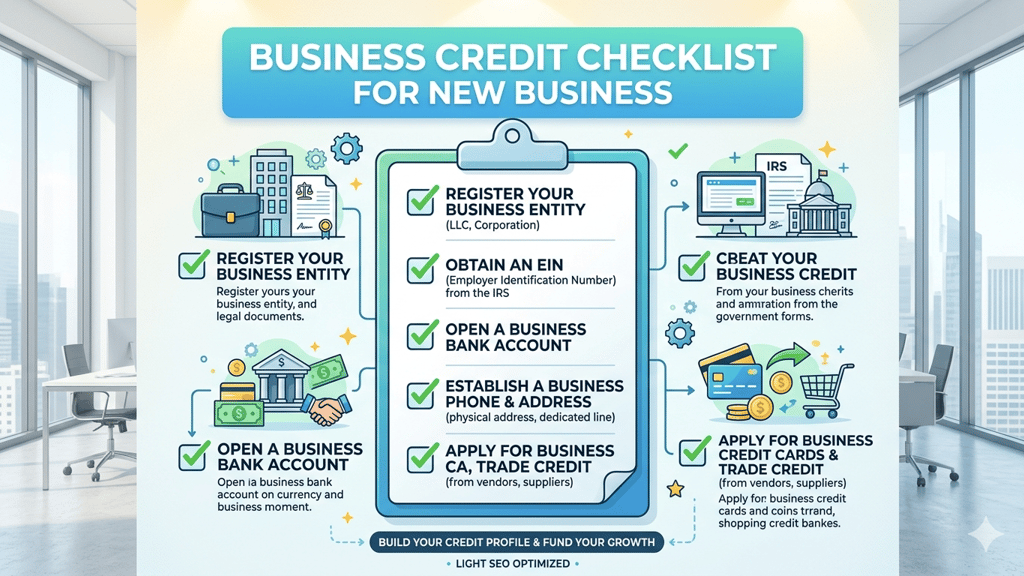

Business Credit Checklist for New Business

Work through these steps in order. Each one builds on the last.

Step 1: Form Your Business as a Legal Entity

Business credit starts with a legitimate business structure.

If you are operating as a sole proprietor with no formal registration, you do not have a business entity — you have a business activity. Lenders and credit bureaus need a real, registered business to attach a credit profile to.

Your best options:

LLC (Limited Liability Company) — most popular for small business owners

Corporation (S-Corp or C-Corp) — more formal, used for larger operations

Register your LLC or corporation with your state. The filing fee is typically $50–$500 depending on your state.

This step protects your personal assets and separates you from your business. Both are important for funding.

Step 2: Get Your EIN (Employer Identification Number)

An EIN is like a Social Security Number for your business. It is a 9-digit number issued by the IRS.

You need it to:

Open a business bank account

Apply for business credit

File business taxes

Work with vendors who report credit

Getting an EIN is free and takes about 5 minutes. Apply directly on the IRS website at irs.gov.

Once you have your EIN, use it consistently for all business applications. This is the identifier that ties everything together on your business credit profile.

Step 3: Set Up a Dedicated Business Address and Phone Number

This sounds like a small thing. It is not.

Credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business verify business legitimacy partly through consistency of information. If your address or phone number changes across applications — or if you are using your home address and personal phone — it can flag your business as unreliable.

Set up a dedicated business address. A registered agent address or a local mailbox service works fine.

Get a business phone number listed in national directories. Services like Yelp, Google Business, and 411.com are where many lenders verify your business exists. Make sure your name, address, and phone number are consistent everywhere.

This consistency is called your NAP profile — Name, Address, Phone. It matters more than most new business owners realize.

Step 4: Open a Business Checking Account

You cannot build business credit if all your money flows through a personal account.

Open a dedicated business checking account as soon as your LLC or corporation is registered. Use it for all business income and expenses.

This does a few important things:

It shows financial separation between you and your business

Some banks will eventually offer business credit cards or credit lines based on your account history

It builds your banking relationship, which lenders look at during the underwriting process

Go with a bank that offers business credit products. Larger banks like Chase, Bank of America, or Wells Fargo have full small business product lines. Credit unions are another solid option.

Step 5: Register with the Major Business Credit Bureaus

Business credit does not automatically get reported like personal credit does. You have to be proactive about it.

The three main business credit bureaus are:

Dun & Bradstreet (D&B) — the most widely used by lenders and vendors

Experian Business — tracks business payment history and financial data

Equifax Business — used by many lenders for business credit decisions

For Dun & Bradstreet, the first thing you need is a D-U-N-S Number. This is a unique 9-digit identifier for your business. You can get one free at dnb.com. Some applications take a few days to process.

Once you have your D-U-N-S Number, make sure your business information is accurate and up to date on the D&B profile. Errors in your listing can hurt your scores.

Step 6: Open Vendor Accounts That Report to Credit Bureaus

This is where many new business owners get stuck.

You need payment history to build a business credit score. But to get payment history, you need accounts that report to the bureaus. And to get those accounts, you feel like you need credit already.

The way to break this cycle is through starter vendor accounts — also called net-30 accounts or trade lines.

Trade lines are vendor accounts where you buy now and pay within 30 days. When you pay on time, the vendor reports that positive payment history to the business credit bureaus. Over time, this builds your credit profile from scratch.

Some vendors are well known for working with new businesses that have little or no credit history. Categories to look at include:

Office and supply vendors

Fuel and fleet accounts

Business service providers

Start with 3 to 5 vendor accounts. Use them regularly. Pay every invoice on time or early. This is the core engine of the business credit setup process.

Step 7: Monitor Your Business Credit Reports

Once you start building, you need to check your progress.

Pull your business credit reports from Dun & Bradstreet, Experian Business, and Equifax Business regularly. Look for:

Errors or outdated information

Accounts that should be reporting but are not

Negative marks from unpaid invoices or collections

Your Paydex Score from D&B is one of the most commonly used scores by lenders. It ranges from 0 to 100. A score of 80 or above is generally considered good. You reach 80 by consistently paying on time or early.

Experian Business and Equifax Business have their own scoring models. The logic is similar — pay on time, keep accounts in good standing, and your scores will grow.

Catching errors early matters. A wrong address or incorrect payment status can drag your scores down for no reason. Dispute anything inaccurate directly with the bureaus.

Step 8: Apply for a Business Credit Card

Once you have a few trade lines established and at least 90 days of payment history, you can start looking at business credit cards.

Business credit cards do a few things for your profile:

They add revolving credit to your mix (revolving credit means you borrow and repay on an ongoing basis, like a credit card with a limit)

They show lenders that your business can manage credit responsibly

Many report to business credit bureaus, adding to your profile

Start with a card that is easier to get approved for — secured business cards or cards from your business bank. Use it for normal business expenses. Keep your credit utilization low. That means do not use more than 30% of your available limit. High utilization signals financial stress to lenders.

Pay the full balance every month if you can. This builds a strong payment history while avoiding interest charges.

Step 9: Keep Your Business Information Consistent Everywhere

This step is ongoing, not a one-time task.

Every time your business appears online — on a vendor application, on a listing directory, on a credit bureau profile — the information needs to match exactly.

Business name, address, phone number, EIN. All of it.

Inconsistent information confuses credit algorithms and can lower your business credit scores. It can also cause lenders to question whether your business is legitimate.

Audit your business information every few months. Update any profiles that have old addresses, old phone numbers, or slight variations in your business name.

Step 10: Build Toward Fundability

After 6 to 12 months of following this process, your business should start to look fundable — meaning it meets the basic criteria lenders check before approving business financing.

A fundable business profile generally includes:

A registered LLC or corporation

An EIN

A business bank account with at least 3 months of history

An established business credit profile with multiple trade lines

A Paydex Score of 75 or higher

Consistent business information across all platforms

When these things are in place, your chances of getting approved for business funding improve significantly. You are no longer starting from zero with every lender — your business has a track record they can review.

Quick Reference: Business Credit Setup Checklist

Here is the full checklist in summary form:

Form your LLC or corporation

Get your EIN from the IRS

Set up a dedicated business address and phone number

Open a business checking account

Get a D-U-N-S Number from Dun & Bradstreet

Register your business with Experian Business and Equifax Business

Open 3–5 starter vendor accounts (net-30 trade lines)

Pay all invoices on time or early

Monitor your business credit reports quarterly

Apply for a business credit card after 90 days of payment history

Keep all business information consistent across platforms

Review your fundability every 6 months

How Long Does It Take to Build Business Credit?

A common question — and a fair one.

The honest answer: you can see initial results in 3 to 6 months if you follow the steps above. A solid profile with multiple trade lines and a decent Paydex Score usually takes 12 months of consistent effort.

There are no shortcuts that actually hold up. Businesses that try to rush the process by getting too many accounts at once or applying for funding too early often end up with rejected applications and hard inquiries that hurt their scores.

Slow and steady is genuinely the right approach here. Build the foundation well and the funding access follows.

Common Mistakes New Business Owners Make With Business Credit

Avoid these. They are easy to fall into and slow down your progress.

Using a personal address for the business. It muddles the separation between you and your business entity.

Getting vendor accounts that do not report to credit bureaus. Not all vendors report. If they do not report, the payment history does not build your profile. Always confirm a vendor reports before opening an account for credit-building purposes.

Applying for too much credit too soon. Multiple applications in a short window create hard inquiries and signal financial desperation to lenders.

Ignoring errors on your credit reports. Errors are common. An uncorrected error can keep your score artificially low for months.

Mixing business and personal finances. Even after forming an LLC, some owners continue using personal accounts for business expenses. This weakens the argument that your business is a separate financial entity.

Frequently Asked Questions

What is the first step in building business credit for a new business?

The first step is forming a legal business entity — an LLC or corporation — and getting an EIN from the IRS. Without these two things in place, there is no business entity to attach a credit profile to.

How do I start building business credit with no credit history?

Start with net-30 vendor accounts (trade lines) that report to business credit bureaus. Pay them on time. After 3 to 6 months of consistent payment history, you will have a starting score that lenders can see.

Does getting a D-U-N-S Number automatically build my business credit?

No. Getting a D-U-N-S Number creates a record in the Dun & Bradstreet system, but it does not build credit on its own. You need active accounts reporting positive payment history to generate a Paydex Score.

Can I build business credit without using my SSN?

In the early stages, some lenders and vendors will ask for a Social Security Number for identity verification. However, as your business credit profile grows, many lenders shift their focus to your EIN and business credit scores rather than personal credit. The goal of this process is to get to that point.

How many trade lines do I need to get a good business credit score?

Starting with 3 to 5 trade lines is a reasonable foundation. More accounts with consistent on-time payments generally produce better scores over time. The quality and consistency of your payments matters more than the raw number of accounts.

What credit score do I need to get a business credit card?

It depends on the card. Some secured business credit cards have very low requirements. Standard business credit cards often look at a combination of your personal credit score and your business credit profile. As your business credit grows, you become less dependent on personal credit for approvals.

How do I check my business credit score for free?

You can check your D-U-N-S profile and limited Paydex information at dnb.com. Experian Business and Equifax Business offer paid reports. Some third-party platforms offer limited free business credit monitoring as well.

Start Building Your Business Credit the Right Way

Building business credit is one of the most practical things you can do for your company's long-term financial health. It takes time. It takes consistency. But the payoff — real funding access without leaning on personal credit — is worth it.

The checklist above gives you a clear, step-by-step path. Follow it in order. Do not skip the foundation steps. And track your progress as you go.

If you want hands-on guidance building your business credit profile, getting your first trade lines set up, or improving your business's fundability before applying for working capital — Altopex.com can help you navigate the process step by step.

Published by Altopex.com — Business Credit & Funding Guidance for U.S. Small Business Owners