How to Establish Business Credit Quickly (2026 Guide)

Learn how to establish business credit quickly with proven steps. Start building business credit today and unlock funding, higher limits, and real growth.

BUSINESS CREDIT

Russel

6/11/20267 min read

Your Business Deserves Its Own Credit Identity

Getting funding as a small business owner is hard.

Most banks and lenders want to see a track record. They want to know your business can handle credit. But when your business is new, that record does not exist yet.

That is the problem.

And here is the real issue — most business owners wait too long to start building business credit. They run everything through their personal accounts, use their personal SSN for financing, and never separate their business identity from their own.

This makes funding harder. It keeps your limits low. And it puts your personal credit at risk every time your business needs money.

The good news? You can fix this. You can start building business credit today, even if your business is brand new. And when you do it the right way, you can establish business credit quickly — faster than most people think.

This guide walks you through every step. Simple, clear, and practical.

What Is Business Credit and Why Does It Matter?

Business credit is your company's financial reputation.

Just like your personal credit score tells lenders how you manage personal debt, your business credit profile tells lenders how your company manages money. It is tied to your business — not your personal SSN.

When your business has strong credit, lenders and vendors look at your company's history, not your personal finances. That means:

Higher credit limits

Better loan terms

Funding without a personal credit check

More separation between your personal and business finances

The three main business credit bureaus — Dun & Bradstreet, Experian Business, and Equifax Business — track your business credit activity. Each one issues a score based on how your business handles payments, credit usage, and financial obligations.

Building a strong profile with all three bureaus should be one of your top priorities as a business owner.

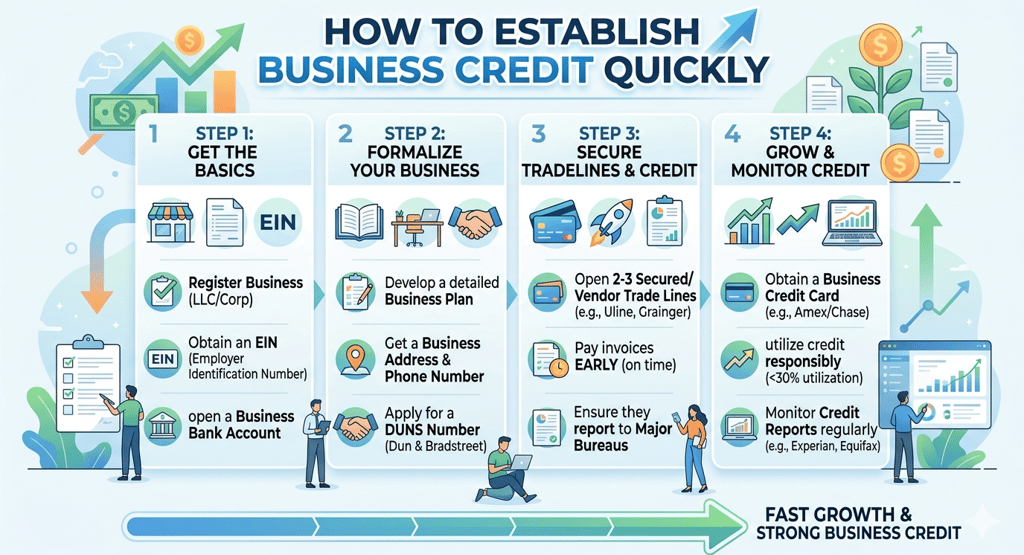

Step 1: Set Up Your Business the Right Way

Before you can establish business credit quickly, your business needs to look like a real, separate entity.

That means completing a few key steps that many owners skip.

Form an LLC or Corporation

If you are operating as a sole proprietor, you are invisible to business credit bureaus. Lenders also see sole proprietors as higher risk because there is no legal separation between you and your business.

Forming an LLC (Limited Liability Company) or corporation creates a separate legal identity for your business. This is the foundation for everything else.

Get an EIN (Employer Identification Number)

An EIN is like a Social Security Number for your business. The IRS issues it for free at IRS.gov, and it takes minutes to get.

You need an EIN to open a business bank account, apply for credit, and build a credit file under your business name. Without it, you are still using your SSN — and that keeps your business credit invisible.

Get a Business Address and Phone Number

Lenders and credit bureaus verify your business information. Use a real business address (not a P.O. box for all applications) and a dedicated business phone number. This builds legitimacy.

Build a Basic Business Website

You do not need a complex site. Even a simple professional website with your business name, services, and contact info makes your business look established. Many lenders quietly check for this.

Step 2: Open a Business Bank Account

This is non-negotiable.

A dedicated business bank account separates your personal and business finances. It also creates a paper trail that shows lenders your business is actively operating.

Open a business checking account in your business name using your EIN — not your personal SSN. Use it consistently for all business income and expenses.

After a few months of steady activity, your bank may offer you a business credit card or small line of credit. That is your first credit account under your business name.

Step 3: Get a DUNS Number from Dun & Bradstreet

Dun & Bradstreet is one of the most important business credit bureaus. Many lenders and vendors check your D&B profile before extending credit.

Your DUNS number is a unique 9-digit identifier for your business on the D&B system.

Getting one is free and straightforward at Dnb.com. Once you have it, D&B begins tracking your business credit activity.

This is one of the fastest ways to start building a credit file — and it costs nothing to set up.

Step 4: Open Vendor Accounts (Net-30 Accounts)

This is one of the best strategies to fast track business credit building, especially when your business is new.

Vendor accounts, also called net-30 accounts or trade lines, are accounts where a supplier gives you products or services and gives you 30 days to pay.

When you pay on time, they report that positive payment history to business credit bureaus. Each payment builds your credit file.

Some vendors approve new businesses with no prior credit history. A few that are commonly used to start building include:

Uline — packaging and shipping supplies

Quill — office supplies

Grainger — industrial and safety products

Crown Office Supplies — office products

The CEO Creative — business services

Start with 3 to 5 vendor accounts. Make small purchases. Pay early or on time. Let the positive reports stack up.

This is how you get your first business credit accounts when you have no history yet.

Step 5: Apply for a Business Credit Card

Once you have a few vendor accounts reporting and your business bank account is active, you are ready to apply for a business credit card.

Business credit cards do two important things:

They report to business credit bureaus (building your score)

They give you revolving credit — a line of credit you can use, pay down, and use again

Look for starter business credit cards that accept newer businesses. Some options have low revenue requirements. Others are secured cards that require a deposit.

Use the card for regular business expenses. Keep your credit utilization — that is the percentage of your limit you are using — below 30%. Paying your balance in full each month is even better.

This consistent activity builds your business credit file faster than almost anything else.

Step 6: Monitor and Manage Your Business Credit

Building credit is not a one-time event. It is an ongoing process.

Check your business credit reports regularly with:

Dun & Bradstreet (Nav.com gives free access to your D&B score)

Experian Business

Equifax Business

Look for errors. If a vendor is not reporting your payments, contact them. If incorrect information appears on your report, dispute it directly with the bureau.

Your goal is to have multiple positive accounts reporting consistently. Over time, your scores will rise and lenders will start seeing your business as a reliable borrower.

How Long Does It Take to Establish Business Credit?

This is the question everyone asks.

Here is the honest answer: you can have a basic business credit file in as little as 30 to 60 days if you move quickly on the foundation steps. Getting to a strong, fundable credit profile typically takes 6 to 12 months of consistent activity.

The timeline depends on:

How fast you set up your LLC, EIN, and bank account

How many vendor accounts and credit cards you open

How consistently you pay on time

Whether your accounts are reporting to the right bureaus

The fastest path is to do the setup right from the beginning and stack positive payment history from multiple accounts as quickly as possible.

Common Mistakes That Slow Down Business Credit Building

Many business owners unintentionally hurt their chances. Here are the biggest mistakes to avoid:

Using your personal SSN for everything. This keeps your business credit profile invisible. Always use your EIN when applying for business accounts.

Applying for too many accounts at once. Multiple applications in a short window can trigger hard inquiries. Space them out.

Missing payments or paying late. Payment history is the most important factor in your business credit score. One late payment can set you back significantly.

Skipping the setup steps. If your business does not have a complete and verified profile — proper address, phone, website — lenders and bureaus may not take your applications seriously.

Not checking your credit reports. Errors happen. Accounts stop reporting. You need to monitor your profile consistently.

What Happens When Your Business Credit Is Strong?

This is what you are working toward.

When your business credit profile is well-established, doors open that were closed before:

Business credit cards with limits of $10,000 to $50,000 or more

Working capital loans without a personal guarantee

Trade lines with higher credit limits from suppliers

Net-30 or net-60 accounts with better vendors

Revolving credit lines you can use as needed

SBA loans and conventional bank financing become more accessible

Lenders look at your business as a real financial entity with its own track record. Your personal credit becomes less of a factor. And you have access to the capital you need to grow.

Business Credit Setup for Beginners: Quick Checklist

If you are just starting out, use this checklist to get moving today:

Form an LLC or corporation

Apply for an EIN at IRS.gov

Get a business address and dedicated phone number

Open a business bank account using your EIN

Register for a DUNS number at Dnb.com

Open 3 to 5 vendor accounts (net-30)

Apply for a starter business credit card

Pay all accounts on time, every time

Monitor your business credit reports monthly

Each step builds on the last. Do not skip any of them.

Frequently Asked Questions

How long does it take to establish business credit quickly? You can have a basic credit file in 30 to 60 days. A strong, fundable profile with multiple accounts reporting typically takes 6 to 12 months of consistent activity.

Can I build business credit with no personal credit check? Yes. Once your business has established accounts that report to business credit bureaus, many lenders will approve business credit based on your business profile alone — without a personal credit inquiry.

What is the first business credit account I should get? Start with vendor accounts (net-30 accounts) from suppliers like Uline, Quill, or Grainger. These are easiest to get for new businesses and many report to business credit bureaus.

Do I need an LLC to build business credit? You do not technically need an LLC, but it is strongly recommended. An LLC separates your personal and business identity, which is essential for building a distinct business credit profile.

What credit score do I need to get a business credit card? Some starter business credit cards and secured cards are available with limited business history or fair personal credit. Requirements vary by lender, but building your business credit profile alongside your personal profile improves your odds significantly.

Is building business credit worth it for small businesses? Absolutely. Strong business credit gives you access to funding at better terms, protects your personal finances, and positions your business for long-term financial growth.

Conclusion: Start Building Business Credit Today

Building business credit is not complicated. But it does require the right steps, done in the right order, with consistency.

Many small business owners put this off until they urgently need funding. By then, it is too late to build the profile quickly. The best time to start is now — before you need the credit.

Follow the steps in this guide. Set up your business the right way. Open your first accounts. Pay on time. Monitor your progress.

Over time, your business will have a strong financial identity that opens doors to real funding — credit cards, working capital loans, revolving credit lines, and more.

If you want help building your business credit and getting your business fundable, Altopex.com can guide you through the entire process. We work with US small business owners to set up the right foundation, open the right accounts, and access the funding their businesses deserve.

Ready to start? Reach out to Altopex.com today.

Word Count: ~1,800 words | Primary Keyword: how to establish business credit quickly | Supporting Keywords: start building business credit today, fast track business credit building, how to get first business credit account, business credit setup for beginners