Business Credit for New LLC Owners | Starter Guide

New LLC owner? Learn how to build business credit fast, access funding, and grow your business without using your personal credit.

BUSINESS CREDIT

Russel

6/11/20268 min read

Most New LLC Owners Get This Wrong From Day One

You formed your LLC. You got your EIN. You opened a business bank account.

Now you're ready to get funding, right?

Not yet.

Most new LLC owners think forming the company is enough to access business credit. But lenders don't look at your LLC formation date. They look at your business credit profile — and if you haven't built one, you're invisible to them.

That's the problem no one tells you about upfront.

Building business credit for new LLC owners is a process. It takes the right steps, in the right order, starting from day one. When you do it right, you can separate your personal finances from your business, qualify for real funding, and grow without putting your personal credit at risk.

This guide will walk you through every step.

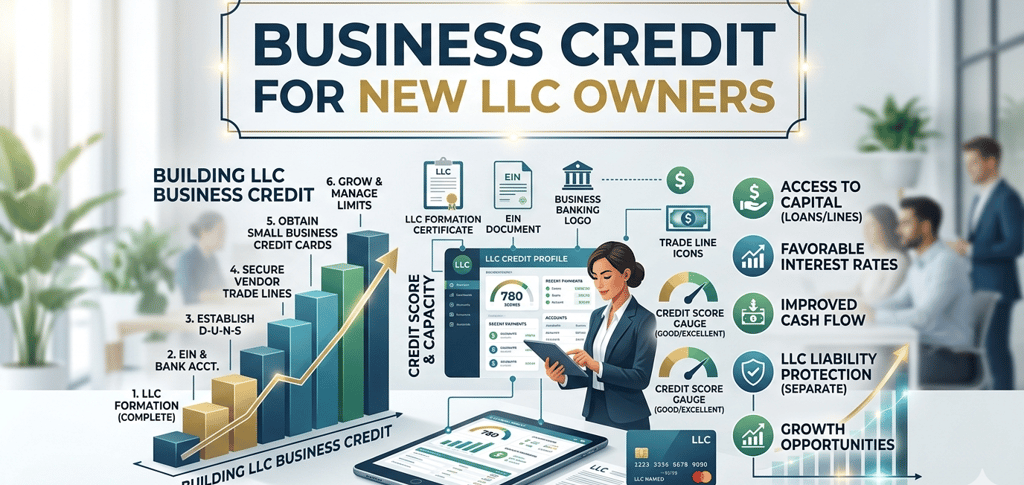

Why Your LLC Needs Its Own Business Credit

Your LLC is its own legal entity. That means it can have its own credit profile — completely separate from your personal credit score.

This matters a lot.

When your business has strong credit, you can:

Get approved for business credit cards with higher limits

Access trade lines and vendor accounts without a personal guarantee

Qualify for working capital loans and lines of credit

Build long-term financial strength for your business

Without business credit, lenders fall back on your personal credit score. That limits your options and puts your personal finances on the line every time you need funding.

Separating the two is one of the smartest moves you can make as a new LLC owner.

Step 1: Make Your LLC Look Legitimate to Lenders

Before you apply for anything, your business needs to pass what's called a fundability check. Lenders run quick verifications to see if your business is real, established, and trustworthy.

Here's what you need to have in place:

Business name: Use the exact same name everywhere — your LLC filing, your bank account, your website, your applications. Inconsistencies raise red flags.

EIN (Employer Identification Number): This is your business's tax ID. It's free from the IRS. Use it on all business accounts — not your SSN. This is how you start building credit under your EIN, not your personal identity.

Business address: Use a real street address, not a P.O. box. If you work from home, a virtual office address works. Lenders want to see a stable business location.

Business phone number: Get a dedicated business phone number listed under your business name. Many vendors verify this before extending credit.

Business bank account: This is non-negotiable. You need a business checking account in your LLC's name. It shows financial activity and is required by most lenders.

DUNS Number: This is a free identifier from Dun & Bradstreet — one of the main business credit bureaus. Register at their website to start a credit file with them.

Getting these basics right is the foundation of your business credit setup for beginners. Skip these steps and you'll hit walls at every stage.

Step 2: Open Accounts That Report to Business Credit Bureaus

This is where most new LLC owners get stuck.

They open a business bank account and think that builds credit. It doesn't.

To build business credit, you need accounts that actually report to the business credit bureaus — Dun & Bradstreet, Experian Business, and Equifax Business.

The best way to start is with vendor accounts and net-30 accounts.

What Are Vendor Accounts?

Vendor accounts are credit accounts with suppliers who let you buy now and pay later — usually in 30, 60, or 90 days. This is called trade credit or a trade line.

Many vendors will approve new businesses with no credit history. They report your payment history to the bureaus, which starts building your business credit score.

Some beginner-friendly vendors that report to credit bureaus include office supply companies, packaging suppliers, and business service providers. Look specifically for net-30 vendors that work with new LLCs.

How to Use Vendor Accounts to Build Credit Fast

Start with 3 to 5 vendor accounts. Make small purchases. Pay the full balance before or on the due date. Do this consistently for 60 to 90 days.

That payment history starts showing up on your business credit file. Your score begins to build.

This is one of the fastest legal ways to establish business credit quickly as a new LLC.

Step 3: Apply for a Business Credit Card

Once you have some vendor account history — even just 60 days — you can start looking at business credit cards.

Business credit cards are a powerful tool. They:

Report to business credit bureaus

Give you access to a revolving credit line

Help you manage cash flow month to month

Some offer rewards, 0% intro APR periods, and other perks

When you're just starting, look for cards designed for new businesses or startups. Some don't require a long business history. A few may still check your personal credit at first, but over time, your business credit takes over.

Important rule: Keep your credit utilization low. Credit utilization means how much of your available credit you're using. Try to stay below 30% of your limit. For example, if your card limit is $5,000, keep your balance under $1,500.

High utilization hurts your score. Low utilization builds it.

Step 4: Understand the Business Credit Bureaus

Unlike personal credit — where most lenders check FICO through Experian, TransUnion, or Equifax — business credit has its own bureaus. And they work differently.

The three main business credit bureaus are:

Dun & Bradstreet (D&B): The largest and most commonly used. Your D&B score is called a PAYDEX score. It's based entirely on how fast you pay your bills. A score of 80 or higher is considered good.

Experian Business: Pulls data from lenders and vendors. Scores range from 1 to 100.

Equifax Business: Also widely used by commercial lenders. They have their own scoring model.

Each bureau collects data from different sources. That's why it's important to have multiple accounts reporting across all three bureaus — not just one.

Check your business credit reports regularly. You can do this through each bureau's website. Look for errors and dispute anything that's incorrect. Wrong information on your file can hurt your approval chances.

Step 5: Build a Strong Business Credit Score Over Time

There's no shortcut to a great business credit score. But there is a fast track — if you follow the right system.

Here's what moves your score in the right direction:

Pay on time, every time. Payment history is the biggest factor in your business credit score.

Keep balances low on any revolving accounts.

Open new accounts gradually. Don't apply for 10 things at once. Build in stages.

Keep accounts active. Old accounts with good history actually help your score. Don't close them unless necessary.

Monitor your profile. Catch errors before they become a problem.

Most new LLC owners can build a solid business credit score within 6 to 12 months of consistent effort. Some get there faster when they start with the right vendor accounts and stay disciplined with payments.

What Types of Funding Can You Access With Business Credit?

Once your business credit is established, the funding options expand significantly.

Here's what becomes available to you:

Business Credit Cards

Higher limits, better terms, and some cards offer 0% intro periods for up to 12–18 months. Great for short-term cash flow.

Business Lines of Credit

A revolving credit line you can draw from as needed. You only pay interest on what you use. This is one of the most flexible funding options for small businesses.

SBA Loans

The Small Business Administration backs loans with favorable terms. Strong business credit — along with time in business and revenue — improves your chances significantly.

Working Capital Loans

Short-term loans designed to cover day-to-day business expenses. Lenders look at business bank statements, credit history, and revenue to approve these.

Trade Lines and Vendor Financing

Once you have a credit profile, more vendors will extend net-30 or net-60 terms. This helps you manage inventory, supplies, and services without tying up cash.

The stronger your business credit, the better the terms you get. Lower interest rates, higher limits, and less reliance on personal guarantees.

Common Mistakes New LLC Owners Make With Business Credit

Knowing what to do is important. So is knowing what not to do.

Mixing personal and business finances. This is the most common mistake. Use your business bank account for all business transactions. Never run business expenses through personal accounts.

Using your SSN when you don't need to. Build the habit of using your EIN from the start. The goal is to establish credit under your business identity, not your personal one.

Skipping the fundability setup. Applying for credit before your business address, phone, and bank account are in order will get you denied — and those denials can hurt your file.

Not monitoring your business credit. Errors on your file can quietly lower your score. Check your reports at least quarterly.

Applying for too much credit too fast. Too many applications in a short period can look risky to lenders. Build in stages.

Avoiding these mistakes puts you well ahead of most new LLC owners trying to figure this out on their own.

Business Credit for LLC Funding: A Realistic Timeline

Here's what a typical fast-track business credit building timeline looks like for a new LLC:

Month 1–2: Set up business address, EIN, DUNS number, business bank account, and phone. Open 3–5 net-30 vendor accounts.

Month 3–4: Make purchases on vendor accounts and pay on time. Business credit file starts populating.

Month 4–6: Apply for a starter business credit card. Keep utilization low. Continue paying vendor accounts on time.

Month 6–9: Score improves. More vendors willing to extend credit. Consider a second business card or a small line of credit.

Month 9–12: Strong business credit profile in place. Eligible for larger credit lines, working capital loans, and potentially SBA-backed products.

This is not overnight. But it's not years away either. With the right steps, you can build real business credit within your first year — and that changes what's available to you.

FAQ: Business Credit for New LLC Owners

Can a brand new LLC get business credit? Yes. You don't need years in business to start. You do need the right setup — EIN, business bank account, and vendor accounts that report to the bureaus. Starting from day one puts you ahead.

Do I need good personal credit to build business credit? Not always. Some vendor accounts and net-30 suppliers approve new LLCs without checking personal credit at all. As your business credit grows, you rely less on your personal score for approvals.

How long does it take to establish business credit? Most businesses can build a solid credit profile in 6 to 12 months. The key is consistency — paying on time and keeping accounts active.

What business credit bureaus should I focus on? All three matter: Dun & Bradstreet, Experian Business, and Equifax Business. Different lenders check different bureaus. Spread your accounts to report across all three.

What is a PAYDEX score? A PAYDEX score is your D&B business credit score. It ranges from 1 to 100. An 80 or above means you pay on time, which is what lenders want to see.

Can I get a business credit card with no business credit history? Some business cards are designed for startups and new businesses. A few may do a personal credit check initially. But once you have a credit history under your EIN, options improve significantly.

Is an LLC better for building business credit than a sole proprietorship? Yes. An LLC is a separate legal entity, which means it can have its own credit profile completely separate from your personal credit. A sole proprietorship doesn't give you that separation.

Final Thoughts: Build Credit Now, Fund Your Business Later

Every month you delay building business credit is a month of missed opportunity.

Your business credit profile doesn't build itself. It needs accounts, payment history, and time. The good news is that once you start, it moves faster than most people expect.

If you're a new LLC owner, the right time to start is right now — not after you need funding.

Get the basics in place. Open vendor accounts. Pay on time. Monitor your file. And take it one step at a time.

If you want help building your business credit the right way — from LLC setup to funding access — the team at Altopex.com can guide you through every step. We work with small business owners across the US to build strong credit profiles and connect them with the funding their business deserves.

Reach out today and let's build something real.