Fast-Track Business Credit Building in 2026

Discover the ultimate beginner's guide for small business owners in 2026 to fast-track your business credit building. Learn how to get funded, establish EIN credit, and accelerate your growth today!

BUSINESS CREDIT

Russel

6/15/20268 min read

Most Small Business Owners Start in the Wrong Place

Most small business owners struggle to get funding — not because their business is bad, but because their business credit isn't set up the right way.

If you've ever applied for a business loan or business credit card and got denied, this guide is for you.

The truth is, building business credit isn't complicated. But there's a right way to do it — especially if you're starting from zero.

This is a beginner's guide to business credit funding. We'll walk through a real business credit building strategy for 2026, step by step, so you can get your business ready to access real funding.

What Is Business Credit and Why Does It Matter?

Business credit is a financial profile that belongs to your business — separate from your personal credit.

When lenders, suppliers, or vendors check your business, they look at this profile. A strong business credit profile means better chances of getting approved for business credit cards, trade lines, working capital loans, and larger funding options.

Here's the key benefit: when your business credit is strong, many lenders won't need to pull your personal credit. That means you protect your personal score and keep your business finances completely separate.

For small business owners, LLC owners, and startups in the US, this separation is one of the most powerful financial moves you can make.

Why Business Credit Building Is Different in 2026

The lending landscape has shifted. In 2026, lenders look at more than just credit scores. They look at:

How long your business has been active

Whether your business information is consistent everywhere

Your relationship with vendors and suppliers

Your business bank account history

Your EIN credit history (more on this below)

If any of these elements are weak or missing, it slows down your ability to get approved. That's why having a real business credit building strategy matters more than ever.

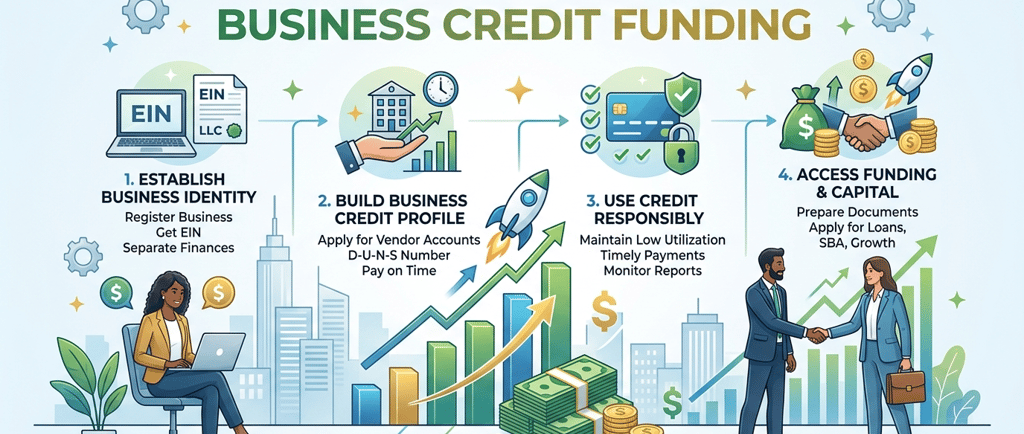

Step 1: Set Up Your Business the Right Way

Before you can build business credit, your business needs to look credible — both to lenders and to credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business.

Here's what you need in place first:

Register your business as an LLC or Corporation.

Sole proprietors can struggle to get business credit because there's no legal separation between the owner and the business. An LLC creates that separation and makes your business a real entity in the eyes of lenders.

Get an EIN (Employer Identification Number).

An EIN is basically a Social Security Number for your business. You get it free from the IRS. It's required to open business bank accounts, apply for credit, and file business taxes. This is the starting point for building EIN credit — which is credit tied to your business tax ID, not your personal SSN.

Get a dedicated business phone number and address.

Your business needs to have consistent contact information. Use a real business address (not a PO box) and a phone number listed under your business name. Lenders and credit bureaus verify this.

Open a dedicated business checking account.

This is non-negotiable. A business bank account separates your finances, builds transaction history, and is required by most lenders before they'll approve any funding.

These steps form the foundation. Without them, the rest of your business credit starter guide won't work the way it should.

Step 2: Get Listed with Business Credit Bureaus

Here's something most beginners don't know: your business credit profile doesn't build itself automatically.

You need to get listed with the major business credit bureaus:

Dun & Bradstreet — Get a D-U-N-S Number (free, takes a few days)

Experian Business

Equifax Business

Dun & Bradstreet is especially important. Most lenders and vendors check your Paydex score, which is Dun & Bradstreet's business credit score. A Paydex score of 80 or above is considered good.

Getting listed is step one. Building a positive payment history with those bureaus is what comes next.

Step 3: Start with Starter Vendor Accounts (Trade Lines)

This is one of the fastest ways to start building business credit — and most beginners skip it entirely.

Vendor accounts, also called trade lines, are accounts with suppliers who sell you products or services on net terms. For example, "Net 30" means you have 30 days to pay the invoice.

When you pay on time, these vendors report your payment history to the business credit bureaus. This builds your credit profile from the ground up — without needing a strong credit score to get started.

Some well-known vendors that report to business credit bureaus include:

Uline (shipping and packaging supplies)

Quill (office supplies)

Grainger (industrial supplies)

Crown Office Supplies

Summa Office Supplies

You don't need to use all of them. Start with 3 to 5 vendor accounts. Order small amounts you actually need. Pay on time or early. Let the payment history build your profile over 3 to 6 months.

This is often called a business credit setup for beginners — because it's low risk, easy to qualify for, and it lays the foundation for everything else.

Step 4: Get Your First Business Credit Account

Once you have some payment history from vendor accounts, you're ready to apply for your first business credit account — usually a business credit card.

Here's what to look for as a beginner:

Business credit cards that don't require a personal guarantee — These cards are approved based on your business credit profile, not your personal credit. They typically come after 6 to 12 months of active business credit history.

Secured business credit cards — If your profile is still new, a secured card (where you deposit money as collateral) can help you build history while you use the card responsibly.

Store or gas cards — Some business store cards are easier to get approved for and still report to business credit bureaus. These are good stepping stones.

The key rule: keep your credit utilization low. Credit utilization means how much of your available credit you're using. Try to keep it below 30%. If you have a $1,000 credit limit, don't carry a balance over $300. This signals to lenders that you manage credit responsibly.

Step 5: Build Fundability — What Lenders Actually Check

Fundability is a term used in business credit circles. It means how "ready" your business looks to get approved for funding.

Lenders don't just look at your credit score. They check your entire business profile. Here's what they want to see:

Consistent business information across all platforms (Google, Yelp, bank accounts, tax filings, loan applications)

Active business checking account with regular deposits and transactions

At least 6 months of business history (some lenders require 12+ months)

Business phone and address that match your legal filings

No major red flags like tax liens, judgments, or derogatory marks on your business profile

Many small business owners get denied not because of bad credit — but because their business information is inconsistent or incomplete. Fixing these gaps can significantly improve your chances of getting approved.

Step 6: Access Real Business Funding

Once your foundation is built, you can start going after real funding options. Here's what becomes available as your business credit grows:

Business credit cards with higher limits — With a solid credit profile, you can qualify for cards with $10,000 to $50,000+ limits, often without using your personal credit.

Net 30 and Net 60 trade lines — As your Paydex score grows, more suppliers will extend you higher credit limits and better terms.

Working capital loans — These are short-term loans used to cover daily business expenses, inventory, or cash flow gaps. Lenders look at your business credit, bank statements, and revenue.

SBA loans — The Small Business Administration backs loans that offer lower interest rates and longer repayment terms. These typically require 1 to 2 years of business history and a solid credit profile.

Business lines of credit — A revolving credit option (like a credit card but with a higher limit and more flexibility). You draw funds when you need them and pay back what you use. Many business owners use these for ongoing operational needs.

The path from zero to real funding typically takes 6 to 18 months when done consistently. The businesses that get there fastest are the ones that treat credit building as a real strategy — not an afterthought.

Common Mistakes That Slow Down Business Credit Building

Even with the right strategy, these mistakes can hold you back:

Mixing personal and business finances. This is the most common mistake. If you use your personal bank account or personal card for business expenses, lenders can't see clean business financial activity.

Not monitoring your business credit reports. Errors happen. Check your Dun & Bradstreet, Experian Business, and Equifax Business reports regularly and dispute anything incorrect.

Applying for too many accounts at once. Multiple credit inquiries in a short period can signal risk. Build slowly and strategically.

Missing payments. Even one late payment can drop your Paydex score. Set up automatic payments wherever possible.

Not having consistent business information. If your business name is spelled differently on your bank account versus your tax filing, it creates confusion in your credit profile.

How Long Does It Take to Build Business Credit?

Here's a realistic timeline:

MilestoneTimelineBusiness setup complete (LLC, EIN, bank account)Week 1–2D-U-N-S Number registeredWeek 2–4First vendor accounts activeMonth 1–2First business credit cardMonth 3–6Paydex score of 80+Month 6–9Access to working capital loansMonth 9–18Business line of credit or larger fundingMonth 12–24

This timeline can move faster or slower depending on how consistently you follow the strategy. But most business owners see real progress within 6 months if they stay consistent.

Conclusion: Your Business Credit Building Strategy for 2026 Starts Now

Building business credit isn't something that happens overnight. But it's absolutely possible — even if you're starting from zero.

The businesses that access real funding and grow faster are the ones that took the time to build the right foundation. That means setting up your LLC correctly, getting listed with credit bureaus, opening the right accounts, and building a payment history that lenders can trust.

You don't have to figure this out alone.

If you want help building your business credit the right way and getting access to real funding options, Altopex.com can guide you step by step. We work with small business owners across the US to build strong business credit profiles and connect them with the funding their business needs.

Frequently Asked Questions (FAQs)

What is the fastest way to build business credit?

The fastest way is to set up your LLC and EIN, open a business checking account, register with Dun & Bradstreet, and start with starter vendor accounts (trade lines) that report to business credit bureaus. Paying these on time builds your Paydex score within 3 to 6 months.

Can I build business credit without using my personal credit?

Yes. Once your business credit profile is established with positive payment history, many lenders and vendors will approve your business without pulling your personal credit. This is one of the main benefits of building strong EIN credit.

How do I get my first business credit account?

Start with Net 30 vendor accounts from suppliers like Uline, Quill, or Grainger. These are easy to qualify for and report to business credit bureaus. After 3 to 6 months of positive history, you can apply for a business credit card or secured business credit line.

What credit score do I need for a business loan?

It depends on the lender. For SBA loans, most require a personal credit score of 650+ and solid business financials. For working capital loans and business credit cards, a Paydex score of 75 to 80+ improves your approval chances significantly.

How is business credit different from personal credit?

Business credit is tied to your EIN and your business entity, not your personal Social Security Number. It's tracked by separate bureaus (Dun & Bradstreet, Experian Business, Equifax Business) and scored differently. Building strong business credit protects your personal credit and allows your business to borrow independently.

Do I need an LLC to build business credit?

You don't technically need an LLC, but it helps significantly. An LLC separates your personal and business finances legally and makes your business look more credible to lenders. Most business credit experts recommend forming an LLC as the first step.

What is a Paydex score?

A Paydex score is Dun & Bradstreet's business credit score. It ranges from 0 to 100. A score of 80 means you consistently pay on time. A score above 80 means you sometimes pay early. Most lenders prefer a Paydex score of 80 or higher.

Ready to build your business credit the right way? Contact Altopex.com and let us help you create a clear path to funding.