Business Credit Building Guide for LLC Owners (2026 Edition)

Most new LLC owners make the same mistake. They think forming an LLC automatically gives them business credit. It doesn't. Your LLC is a new entity. It has no credit history. No lenders know it. No vendors trust it yet.

BUSINESS CREDIT

Russel

5/22/20267 min read

Most new LLC owners make the same mistake. They think forming an LLC automatically gives them business credit. It doesn't. Your LLC is a new entity. It has no credit history. No lenders know it. No vendors trust it yet.

That's not a problem — it's a starting point.

This business credit building guide for LLC owners will show you exactly how to go from zero credit to a strong business credit profile. Step by step. No fluff.

Why Building Business Credit for Your LLC Matters

When you run a business, you will need funding at some point. Maybe it's to buy inventory. Maybe it's to hire someone. Maybe it's just to cover a slow month.

If you don't have business credit, your only option is personal credit. That means using your Social Security Number. It means lenders checking your personal credit score. It means your personal finances getting tied to your business risk.

Business credit changes that.

With a strong business credit profile, you can:

Get business funding using your EIN (Employer Identification Number), not your SSN

Access higher credit limits than most personal cards offer

Qualify for business credit cards, trade lines, and working capital loans

Keep your personal credit score protected from business activity

For LLC owners, this is not optional if you want serious growth. It's a foundation.

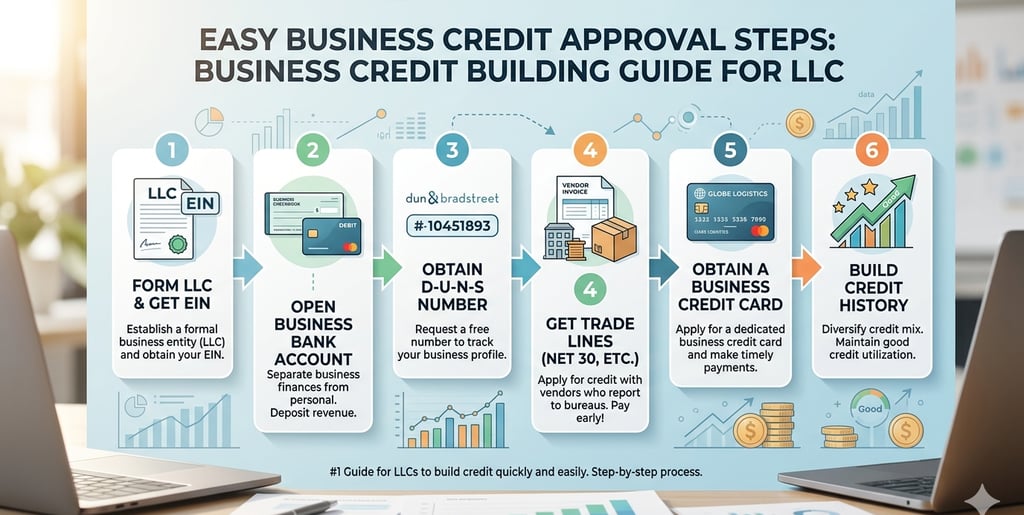

Step 1 — Make Your LLC Look Real to Lenders

Before any lender or creditor looks at your business credit, they check something else first. They check whether your business looks legitimate.

This is called fundability. Think of it as your business's professional image.

Here's what lenders actually verify:

Business name and address — Your LLC should have a real business address, not just a home address. A virtual office address or a registered agent address works for many businesses.

Business phone number — It should be listed in 411 or a business directory. Don't use your personal cell phone as the primary line.

Business email — Use a professional email tied to your domain. Not a Gmail or Yahoo account.

Business website — Even a simple site matters. Lenders Google your business.

EIN — Your Employer Identification Number is the business version of an SSN. You need one. Get it free from the IRS at IRS.gov.

These steps sound basic. But many business owners skip them. When a lender can't verify your business information, they don't approve funding.

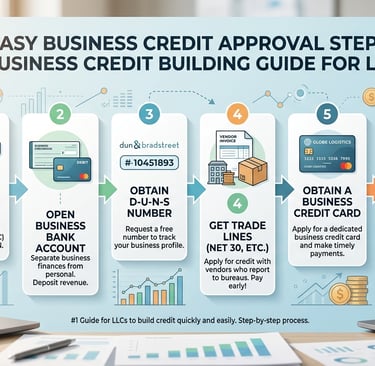

Step 2 — Open a Dedicated Business Bank Account

This is non-negotiable when building business credit for a new LLC.

Your business needs its own bank account. Not a personal account used for business. A real, separate business checking account.

Why does this matter? Because lenders check how long your business bank account has been open. They look at average daily balances. Some lenders won't approve funding unless your account has been active for at least 3 to 6 months.

Open your business bank account early. Keep some balance in it consistently. Don't let it go to zero every month.

This single step builds what's called bank credit — one of the most important factors in getting business loans and working capital approved.

Step 3 — Register With the Business Credit Bureaus

Personal credit has Equifax, Experian, and TransUnion. Business credit has its own bureaus.

The three main business credit reporting agencies are:

Dun & Bradstreet (D&B) — Get a D-U-N-S Number for free at dnb.com. This is required to build a D&B Paydex score.

Experian Business — Tracks business payment history and credit activity.

Equifax Business — Monitors business financial data and credit behavior.

Many new LLC owners don't know these exist. They don't register. So even when they pay vendors on time, it never gets reported. That means no credit history builds up.

Registering with these bureaus is how you make sure your positive payment activity actually counts toward your business credit score.

Step 4 — Start With Starter Vendor Accounts (Trade Lines)

This is where building business credit actually begins.

Trade lines are accounts with vendors or suppliers that report your payment history to business credit bureaus. When you buy on net terms and pay on time, your credit score grows.

Some vendors offer starter accounts to businesses with no credit history. These are called Tier 1 vendors. They approve based on your business information, not your personal credit.

Common examples include:

Office supply stores that offer Net-30 accounts

Business product distributors with vendor credit terms

Wholesale suppliers who report to D&B or Experian Business

The strategy is simple. Apply for two to five of these starter accounts. Use them. Pay within the terms. Let the positive history report.

After three to six months of on-time payments, you'll have a real business credit profile. That's when you can move to stronger credit options.

Step 5 — Apply for Business Credit Cards With EIN Only

Once you have a few trade lines reporting, you can start applying for business credit cards.

Some business credit cards allow you to apply using just your EIN and business information, without a hard pull on your personal credit. These are especially valuable for new LLC owners who want to protect their personal credit score.

Look for:

Secured business credit cards (great for starting out)

Store-based business credit cards with easier approval

Cards from banks where you already have a business checking account

Keep your credit utilization low — that means don't use more than 30% of your available limit at any time. Credit utilization is just how much of your credit limit you're using. If you have a $1,000 limit, keep the balance under $300. This shows lenders you manage credit responsibly.

Step 6 — Pay Everything On Time, Every Time

Business credit scoring is heavily based on payment history. This is true across D&B, Experian Business, and Equifax Business.

Late payments hurt your score fast. On-time payments build it steadily.

Dun & Bradstreet uses a scoring system called the Paydex Score. It goes from 1 to 100. A score of 80 means you pay on the exact due date. A score above 80 means you pay early.

Paying early is one of the fastest ways to build a strong business credit score. Set up reminders or auto-pay for all vendor accounts and business credit lines.

How Long Does It Take to Build Business Credit for an LLC?

Here's a realistic timeline:

Months 1–2: Set up your LLC structure, EIN, business bank account, and business address. Register with credit bureaus.

Months 2–4: Open two to five starter vendor accounts. Use them and pay on time.

Months 4–6: Your first business credit profile appears. Paydex score and Experian Business score start building.

Months 6–12: Apply for business credit cards. Expand trade lines. Apply for small business financing if needed.

Year 1+: Access larger funding options — business lines of credit, working capital loans, SBA-backed products.

This isn't a get-rich-quick system. It's a real credit-building process. But it works, and it compounds over time.

Common Mistakes New LLC Owners Make

Mixing personal and business finances. This makes it harder to establish your LLC as a separate credit entity.

Not registering with business credit bureaus. Your payments go unreported and your credit score stays at zero.

Applying for too many accounts at once. Multiple hard inquiries in a short window can hurt your approval chances.

Ignoring the business address and phone setup. Lenders verify this information before they approve anything.

Giving up too early. Business credit takes time. Six to twelve months is normal before you see strong results.

What Lenders Look for When You Apply for Business Funding

When you apply for a business loan or line of credit, lenders don't just check your credit score. They look at a full picture.

Here's what most lenders evaluate:

Time in business (older is better — but you can start early)

Business credit scores across D&B, Experian, and Equifax

Business bank account history and average balance

Annual business revenue

Existing debt obligations

Industry type and associated risk

The more boxes you check, the stronger your application looks. That's exactly why building business credit as early as possible gives you a long-term advantage.

FAQs About Business Credit Building for LLC Owners

Q: Can I build business credit without using my SSN? Yes. Once your business has an established credit profile, many lenders and vendors will approve accounts using your EIN only. However, some lenders — especially for larger funding — may still do a personal credit check during early stages.

Q: How do I establish business credit quickly as a new LLC? The fastest path is: get your EIN, open a business bank account, register for a D-U-N-S Number, and open two to three starter vendor accounts that report to business credit bureaus. Pay early, not just on time.

Q: Does forming an LLC automatically create business credit? No. Forming an LLC just creates a separate legal entity. Business credit is built through activity — vendor accounts, payment history, and business credit products that report to business credit bureaus.

Q: What is a Paydex score and why does it matter? The Paydex Score is Dun & Bradstreet's business credit score. It ranges from 1 to 100 and measures how quickly you pay your bills. A score of 80 or above shows strong payment behavior and can help you qualify for better funding terms.

Q: How many trade lines do I need to build a business credit profile? Most credit experts recommend at least three to five trade lines reporting before applying for larger credit products. The goal is to show a pattern of responsible credit use over time.

Q: Can a brand-new LLC get business funding? Some startup business funding options exist — like secured credit cards or starter vendor accounts. For larger loans or lines of credit, lenders typically want to see at least 6 to 12 months of business history and some credit activity.

Start Building Your LLC Business Credit Today

Building business credit is not complicated. But it does require the right steps, in the right order, done consistently.

Most small business owners skip this process entirely — and that's why they struggle to get funding when they actually need it.

If you start now, even with a brand-new LLC, you can have a solid business credit profile within six to twelve months. That opens doors to real funding: business credit cards, trade lines, working capital loans, and more.

If you want help building your business credit the right way and setting your LLC up for serious funding access, Altopex.com can guide you through the entire process, step by step.