Quick Business Credit Improvement Methods (2026 Guide)

Discover proven quick business credit improvement methods to boost your business credit score fast. Practical steps for US small business owners.

BUSINESS CREDIT

Russel

5/28/20268 min read

Most small business owners think building business credit takes years.

The truth? Some of the most effective moves can show results in 30 to 90 days. You just have to know what to do — and in what order.

This guide breaks down the real quick business credit improvement methods that lenders and credit bureaus actually respond to. No fluff. No outdated advice. Just practical steps you can take starting today.

Why Your Business Credit Score Matters More Than You Think

If you are running a small business in the US, your business credit score is one of the most important numbers you have. It affects whether you get approved for funding, what interest rates you pay, and how much credit you can access.

But here is what many business owners miss: business credit is separate from personal credit. It is tied to your EIN — your Employer Identification Number — not your Social Security Number.

That means you can build a strong business credit profile without touching your personal credit at all. And when you do it right, lenders see your business as a real, credible entity worth funding.

The 3 Major Business Credit Bureaus You Need to Know

Before we get into the quick business credit improvement methods, you need to understand where your score comes from.

The three main business credit bureaus in the US are:

Dun & Bradstreet — uses the PAYDEX score (0–100)

Experian Business — uses Intelliscore Plus (1–100)

Equifax Business — tracks payment history and credit usage

Each one scores your business differently. The good news is that the improvement strategies below help across all three.

Quick Business Credit Improvement Methods: Step-by-Step

1. Make Sure Your Business Is Set Up Correctly First

This is the foundation. If your business is not properly registered, no credit-building strategy will work well.

Here is what lenders and bureaus look for:

LLC or Corporation structure — not a sole proprietorship

EIN from the IRS — your business tax ID

Business bank account — separate from personal accounts

Business phone number listed in directory services

Business address — not a P.O. box if possible

Professional business email (not Gmail or Yahoo)

If any of these are missing, fix them first. This is called fundability. Many business owners skip this step and wonder why their credit applications get denied.

Getting your business listed on data aggregator sites like 411, Yelp, and Google Business is also part of the setup. Lenders and credit bureaus use these sources to verify your business is real.

2. Get a D-U-N-S Number (Free and Essential)

Dun & Bradstreet is one of the most widely used business credit bureaus. But your business does not automatically get listed there.

You need to apply for a D-U-N-S Number — Dun & Bradstreet's unique identifier for businesses. It is free and takes a few business days.

Once you have your D-U-N-S Number, your business credit history can start being tracked through D&B. Without it, you basically do not exist in that system.

This is a quick win. It costs nothing and opens the door to building a real credit profile.

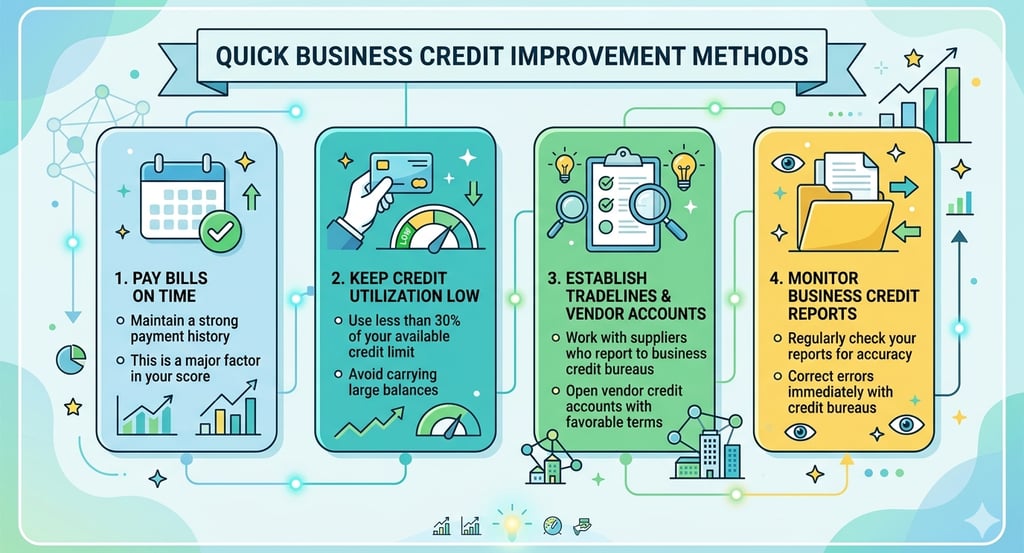

3. Open Vendor Accounts That Report to the Bureaus (Starter Trade Lines)

This is one of the fastest and most underrated quick business credit improvement methods available.

Vendor accounts — also called trade lines — are accounts with suppliers who extend you credit and then report your payment history to the bureaus. When you pay on time, it shows up as positive data on your business credit report.

Some vendors that are known to offer starter accounts to new businesses include:

Uline — office and shipping supplies

Grainger — industrial and safety products

Quill — office products

Crown Office Supplies

Summa Office Supplies

These vendors typically do not require a personal guarantee or strong credit history upfront. You apply using your EIN and business details.

The key is to use the account, pay on time (or early), and let the positive payment history stack up. Even 3 to 5 of these accounts reporting consistently can start moving your score in weeks.

4. Pay Early, Not Just On Time

Here is something most people do not know about business credit:

On the D&B PAYDEX scale, paying on time gets you an 80 out of 100. But paying before the due date can push your score up to 90 or even 100.

That is a significant difference when a lender is reviewing your file.

Early payment signals to lenders that your business manages cash flow well. It is one of the simplest ways to improve your business credit score fast without opening new accounts or taking on debt.

If you currently have trade accounts or vendor relationships, start paying a few days early. It is a small habit that makes a big difference over time.

5. Keep Your Business Credit Utilization Low

Credit utilization is the percentage of your available credit that you are using at any given time.

For example, if you have a $10,000 business credit card limit and you are carrying a $7,000 balance, your utilization is 70%. That is too high. It signals risk to lenders and hurts your score.

The general rule: keep business credit utilization below 30%. Below 10% is even better.

This applies to:

Business credit cards

Business lines of credit

Net-30 accounts

If your utilization is high right now, focus on paying down balances as a priority. Reducing utilization is one of the fastest ways to improve your business credit score because the change shows up as soon as the balance is reported.

6. Dispute Any Errors on Your Business Credit Reports

This is one of the most overlooked steps — and it can be one of the fastest.

Errors on business credit reports are more common than most people realize. Wrong payment history, accounts that do not belong to you, outdated negative information — all of these can be dragging your score down for no reason.

Here is what you should do:

Pull your reports from D&B, Experian Business, and Equifax Business

Review each one carefully for errors

File a dispute directly with the bureau showing proof of the error

Follow up until the correction is made

Some business owners have seen significant score improvements just from getting errors corrected. It takes some time and documentation, but it is worth it.

7. Open a Business Credit Card and Use It Strategically

A business credit card that reports to the business credit bureaus is a powerful tool for building credit.

A few things to keep in mind:

Use the card for regular business expenses (supplies, subscriptions, software)

Pay the balance in full every month if possible

Never let utilization go above 30%

Choose cards that report to D&B, Experian Business, or Equifax Business

Not all business credit cards report to business bureaus. Some only report to personal credit bureaus. So check before you apply.

Cards from larger issuers like American Express, Chase Ink, and Capital One Spark are commonly used by business owners building credit in the US.

8. Build Relationships With Net-30 Vendors Over Time

A net-30 account is a type of trade line where you purchase goods or services and have 30 days to pay the invoice.

When you consistently pay these invoices on time — or early — it adds positive data to your business credit file. The more accounts you have reporting, the stronger your profile becomes.

Over time, having multiple net-30 accounts from different vendors creates a diverse credit history. This is called trade line depth, and lenders look for it when evaluating business credit applications.

Start with three to five vendor accounts, pay them consistently, and add more as your credit profile grows.

9. Separate Business and Personal Finances Completely

This is not just good accounting advice. It directly impacts your ability to build business credit.

When you mix business and personal expenses, lenders cannot clearly evaluate your business's financial health. It also makes it harder to show consistent revenue and cash flow.

Open a dedicated business bank account. Get a business debit card. Keep all business transactions in the business account.

This separation also helps when you apply for business loans, lines of credit, or SBA funding. Lenders want to see clean, organized business financials — not a mix of personal and business spending.

10. Monitor Your Business Credit Regularly

You cannot improve what you are not tracking.

Once you start taking these steps, monitor your business credit reports at least once a month. Check for:

New accounts being reported

Payment history updates

Changes in score

Any errors or unfamiliar entries

D&B CreditSignal offers free alerts. Experian and Equifax both have business credit monitoring options too.

Staying on top of your reports keeps you informed and allows you to respond quickly if something changes.

How Fast Can You Improve Your Business Credit Score?

With the right strategy, here is a realistic timeline:

ActionPotential TimelineSet up business properly (LLC, EIN, address)1–2 weeksGet D-U-N-S Number2–5 business daysOpen and use vendor accounts30–60 days to reportPay early on existing accountsShows on next reporting cycleReduce credit utilizationShows within 30–60 daysDispute credit report errors30–45 days for corrections

Combining multiple strategies at once gives you the best results. Businesses that are consistent with these steps often see meaningful score improvements in 60 to 90 days.

Common Mistakes to Avoid When Building Business Credit

These mistakes slow down your progress:

Applying for too much credit at once. Multiple applications in a short period create inquiries that can hurt your score. Build a foundation first.

Using personal credit when business credit is available. Every time you use personal credit for business expenses, you are missing a chance to build your business profile.

Not paying early. On time is good. Early is better. This is especially true for your PAYDEX score.

Ignoring your credit reports. Many business owners never check their business credit. Errors go uncorrected. Opportunities are missed.

Skipping the setup steps. Trying to build credit before your business is properly set up is like building a house without a foundation.

FAQ: Quick Business Credit Improvement Methods

How long does it take to fix a business credit score?

With consistent action, you can see improvement in 30 to 90 days. Getting vendor accounts set up and reporting, combined with early payments and low utilization, produces the fastest results.

Can I build business credit without using my personal credit?

Yes. Using your EIN instead of your SSN, and working with vendors that do not require a personal guarantee, allows you to build business credit independently of your personal profile.

What is the fastest way to increase my business credit score?

Opening starter vendor accounts that report to the bureaus, paying early, and keeping credit utilization below 30% are among the fastest-acting strategies available.

Do all business credit cards report to business bureaus?

No. Some report only to personal credit bureaus. Always check before applying. Cards from major issuers that specifically offer business credit cards typically report to D&B, Experian Business, or Equifax.

What is the minimum credit score needed for a business loan?

It depends on the lender and loan type. Many SBA loans require a business credit score of 75+ on the PAYDEX scale and a personal credit score of 640+. Building your business credit profile improves your chances of approval and better rates.

Is it possible to build business credit for a new LLC?

Yes. Even a brand new LLC can start building credit by setting up the business correctly, getting a D-U-N-S Number, and opening net-30 vendor accounts. Many lenders will work with a business that has 6+ months of history and a growing credit profile.

Build Your Business Credit With the Right Help

Improving your business credit does not have to be confusing.

The steps above are proven. They work for real small business owners across the US — from startups building their first trade lines to established LLCs trying to access larger funding.

But knowing the steps and executing them correctly are two different things. The timing, the vendor selection, the account sequence — getting these right can make a significant difference in how fast you see results.

If you are ready to take your business credit seriously and want guidance through the entire process — from business setup to vendor accounts to funding access — Altopex.com can help you every step of the way.

Reach out today and let's build a business credit profile that opens real doors for your business.

Published by Altopex.com — Helping US small business owners build strong business credit and access the funding they deserve.