Business Credit Report Setup Process Guide

Learn the exact business credit report setup process step by step. Build your business credit profile, open your credit file, and access funding faster.

BUSINESS CREDIT

Russel

6/8/20269 min read

Most small business owners skip the business credit report setup process entirely. They run their business for years using personal credit — personal credit cards, personal loans, personal guarantees on everything. Then one day they need serious funding, and lenders pull a business credit report that doesn't exist.

That's the problem.

No business credit file means no funding history. No funding history means lenders see you as a risk. And being seen as a risk means smaller loan amounts, higher interest rates, or flat-out denials.

The good news? Setting up your business credit profile from scratch is not complicated. But you have to do it in the right order. Skip steps, and the whole thing falls apart.

This guide walks you through the exact business credit report setup process — from getting your foundation right to making your first credit file appear with the major business credit bureaus.

What Is a Business Credit Report and Why Does It Matter?

A business credit report is a financial profile of your business. It's completely separate from your personal credit history.

It shows lenders, suppliers, and vendors how your business handles money. Things like: do you pay on time? How much credit do you use? How long have you been in business? Do you have active trade lines?

The three main business credit bureaus are Dun & Bradstreet (D&B), Equifax Business, and Experian Business. Each one collects data differently, but all three matter when you're trying to access serious funding.

When a lender runs your business credit, they want to see a file with positive history. If there's nothing there, they'll either deny you or fall back on your personal credit — which means your personal finances are now on the hook.

That's why the business credit profile setup guide matters. Build it right. Build it early.

Business Credit Basics for Small Business: Who Needs This?

Here's a simple answer. Every business owner needs this.

Whether you run a one-person LLC, a small retail shop, a service company, or a startup with five employees — you benefit from having a strong business credit file.

The business credit basics for small business come down to this:

Your business needs its own credit identity

That identity is tied to your EIN (Employer Identification Number), not your Social Security Number

Lenders, suppliers, and landlords check it

A strong profile means better funding terms, higher limits, and more options

If you've been in business even six months and haven't started this process, you're already behind. But it's never too late to start. The sooner you begin, the faster your file builds.

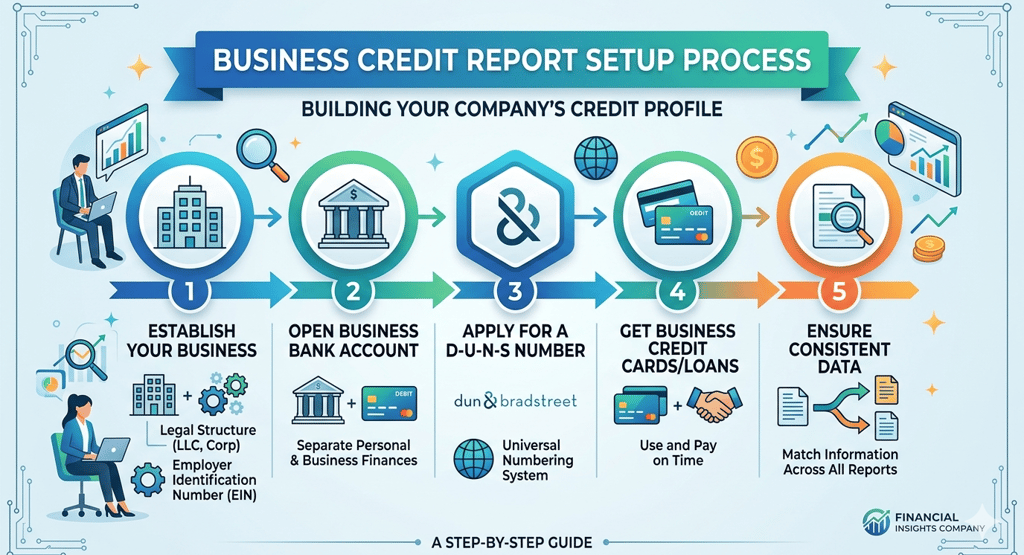

Step-by-Step: How to Open a Business Credit File

Step 1: Get Your Business Legally Set Up

Before anything else, your business needs a legal structure. Most business owners go with an LLC (Limited Liability Company) or corporation. This separates your personal assets from your business assets.

This isn't just a legal formality. Lenders and credit bureaus treat an LLC or corporation differently than a sole proprietorship. A registered business entity signals that you're serious — and it protects your personal credit from your business activity.

If you haven't formed your LLC yet, this is the first step. You register with your state, pay a small filing fee, and get your Articles of Organization or Incorporation.

Step 2: Get Your EIN (Employer Identification Number)

Your EIN is your business's tax ID number. It's free, and you get it from the IRS website in minutes.

Think of your EIN like a Social Security Number for your business. It's what your business uses to open bank accounts, apply for credit, and file taxes.

Every single credit account, vendor application, and funding application you fill out should use your EIN — not your personal SSN. This is how you separate your business credit history from your personal credit history.

Step 3: Get a Dedicated Business Address and Phone Number

This might sound minor. It's not.

Credit bureaus verify your business information across multiple databases. If your business address is a PO box or the same as your home address, some lenders and bureaus may not take your file seriously.

Get a real business address — even a virtual office address works fine. Make sure it matches across your LLC filing, your website, your bank account, and any applications you fill out.

Same with your phone number. Get a dedicated business phone line and list it in 411. Yes, the old-school business directory. Many business credit applications run a 411 verification check. If your business isn't listed, it can flag your application.

Step 4: Open a Business Bank Account

This is non-negotiable.

A business bank account does two things. First, it keeps your business finances separate from personal — which is critical for credit building. Second, it starts establishing your business as a real, active entity.

Open your account in your business name, using your EIN. Use it regularly — pay business expenses through it, keep a decent balance, and don't mix personal transactions in.

Some lenders look at your average business bank balance when making lending decisions. Three to six months of consistent activity helps your case significantly.

Step 5: Register With Dun & Bradstreet and Get a DUNS Number

Dun & Bradstreet is the largest and most widely used business credit bureau. They assign every business a DUNS number — a unique nine-digit identifier that tracks your credit history on their platform.

To start the business credit report setup process with D&B, go to their website and apply for a free DUNS number. It can take a few weeks to process.

Once you have a DUNS number, your business credit file with D&B officially opens. Now you need to start adding positive information to it.

Step 6: Open Vendor and Trade Accounts That Report to Business Credit Bureaus

This is where most small business owners get stuck. They have an EIN and a bank account, but nothing is actually showing up on their business credit report.

The reason? Most regular purchases don't automatically get reported to business credit bureaus. You have to specifically open accounts with vendors and suppliers who report to D&B, Equifax Business, or Experian Business.

These are called trade lines — accounts where a vendor extends credit to your business and reports your payment history to the bureaus.

Some well-known vendors that report to business credit bureaus include office supply stores, fuel card companies, and business-focused wholesale suppliers. When you open these accounts, use your business name and EIN. Pay your invoices on time — early is even better. Positive payment history builds your credit profile quickly.

Step 7: Apply for a Business Credit Card

Once you have a few trade lines reporting, you can apply for a business credit card.

A business credit card from a major bank adds another layer to your credit profile. It shows borrowing capacity and, more importantly, responsible use of revolving credit — meaning credit you can borrow, repay, and borrow again.

Keep your credit utilization low. That's the percentage of your available credit you're actually using. Staying under 30% of your credit limit signals to lenders that you're not over-extended.

Pay the full balance every month if you can. On-time payment history is the single biggest factor in building a strong business credit score.

The Business Credit Checklist for New Businesses

Use this as your quick reference before applying for any funding:

Foundation Setup:

LLC or Corporation registered in your state

EIN obtained from the IRS

Business address (not a PO box)

Business phone number listed in 411

Business bank account opened in company name

Credit File Setup:

DUNS number registered with Dun & Bradstreet

Registered with Experian Business and Equifax Business

At least 3–5 vendor/trade accounts opened and reporting

Business credit card applied for and actively used

Ongoing Maintenance:

All bills paid on time or early

Credit utilization kept below 30%

Business information consistent across all applications and accounts

Business credit reports monitored regularly

How Long Does the Business Credit Report Setup Process Take?

Realistically, 3 to 6 months to build a solid foundation.

In the first 30 days, you can get your LLC, EIN, bank account, and DUNS number in place. That's your infrastructure.

In months two and three, your vendor trade lines start reporting payment history. Your file starts showing positive activity.

By month four or five, with consistent on-time payments and low utilization, you can start qualifying for better business credit cards and small funding products.

By six months, many lenders will look at your business favorably — especially if your file is clean and active.

It's not instant. But it's also not years. A focused 6-month effort can open a lot of funding doors that were closed before.

Common Mistakes That Slow Down Your Business Credit Profile Setup

Using your SSN instead of your EIN. Every credit account, vendor application, and funding form should use your EIN. Mixing the two confuses your credit history.

Inconsistent business information. If your address on your bank account is different from your LLC registration, it can cause verification issues. Keep everything consistent.

Skipping the 411 listing. Small detail, big impact. Some lenders and credit issuers verify that your business phone number is listed in 411. If it's not, applications can be flagged or denied.

Applying for too many accounts too fast. Building business credit is a process, not a race. Opening 10 accounts in one week looks suspicious. Pace yourself.

Not monitoring your credit reports. Errors happen. A supplier might report incorrect data. Check your D&B, Experian Business, and Equifax Business reports regularly and dispute anything wrong.

What Happens After Your Business Credit File Is Open?

Once your file is active and reporting, you have access to a whole new range of funding options.

Business lines of credit — revolving credit that lets you borrow what you need, repay, and borrow again. Great for managing cash flow gaps.

Working capital loans — short-term loans to cover operating expenses, inventory, or payroll. Many lenders look at your business credit profile before approving.

SBA loans — the Small Business Administration offers several loan programs with favorable terms. A strong business credit file improves your application.

Vendor net terms — suppliers extend 30, 60, or 90-day payment terms to businesses with good credit. This is essentially interest-free short-term financing.

Business credit cards with higher limits — as your credit score builds, you qualify for cards with higher spending limits and better rewards.

Each of these options becomes more accessible — and comes with better terms — when your business credit profile is solid.

FAQs About the Business Credit Report Setup Process

How do I start a business credit file from scratch? Start by forming an LLC or corporation, getting your EIN from the IRS, opening a business bank account, and registering for a DUNS number with Dun & Bradstreet. Then open vendor trade accounts that report to business credit bureaus. Payment history on these accounts builds your file.

Does opening a business credit file affect my personal credit? Setting up the foundation — LLC, EIN, bank account — does not affect personal credit. Some vendor accounts do a soft pull, which also has no impact. Certain business credit cards may run a hard inquiry on personal credit during the application. Always confirm before applying.

What is a DUNS number and do I need one? A DUNS number is a free nine-digit identifier issued by Dun & Bradstreet. It's how your business is tracked in their credit system. Many lenders, government contractors, and suppliers require a DUNS number before doing business with you. Yes, you need one.

How many trade lines do I need to build business credit? A minimum of three to five trade lines reporting positive payment history is a good starting point. More accounts with clean payment history means a stronger, more established credit profile.

Can I build business credit with bad personal credit? Yes. Business credit is built on your EIN, not your SSN. If you focus on vendor trade lines that don't require a personal credit check, you can build a strong business credit file regardless of your personal credit score. However, some premium credit products may still check personal credit, so improving both is the long-term goal.

How do I check my business credit score? You can check your business credit score directly through Dun & Bradstreet, Experian Business, and Equifax Business. Some offer free monitoring options; others charge for full reports. It's worth checking all three because different lenders use different bureaus.

What is the fastest way to build business credit? Open multiple vendor trade accounts that report to credit bureaus, pay every bill early or on time, keep credit utilization low, and make sure your business information is consistent everywhere. Three to six months of disciplined activity builds a solid foundation faster than most people expect.

Build Your Business Credit the Right Way — Starting Today

The business credit report setup process isn't complicated. But most business owners either don't know where to start or skip steps and wonder why their funding applications keep getting denied.

Getting the foundation right — LLC, EIN, business bank account, DUNS number — takes less than a month. Then consistently adding trade lines and managing your accounts responsibly does the rest.

Business credit is one of the most powerful financial tools available to small business owners. It lets you borrow using your business identity, protect your personal credit, and access larger funding amounts with better terms as your profile grows.

Start with the checklist. Follow the steps in order. And don't rush the process — steady, consistent activity over 3 to 6 months produces real results.

If you want personalized guidance on setting up your business credit profile or accessing the right funding for your business, Altopex.com can help you build it step by step. We work directly with US small business owners to get their credit foundation right and open doors to real funding opportunities.

Ready to start your business credit journey? Reach out to Altopex.com and let's build your business credit profile the right way.