Business Credit Building Mistakes Small Owners Must Avoid

Avoid the most common business credit building mistakes. Learn the simple business credit building process that helps US small business owners get funded faster.

BUSINESS CREDIT

Russel

6/5/20267 min read

Most small business owners start thinking about business credit only after a lender says no.

That's the first mistake.

Business credit is not something you build overnight. It takes time, the right steps, and a lot of consistency. And when you make avoidable mistakes along the way, you push funding further out of reach.

This guide breaks down the most common business credit building mistakes new and growing businesses make — and exactly what you should do instead. If you are just starting or trying to fix your current credit profile, this is for you.

Why Business Credit Matters More Than Most Owners Realize

Business credit is your company's financial reputation. Lenders, suppliers, and vendors use it to decide how much to trust your business.

When your business has strong credit, you can:

Get approved for higher-limit business credit cards

Access working capital loans without relying on your personal credit

Open vendor accounts and net-30 trade lines (these are accounts where you buy now and pay in 30 days — they help build your credit history)

Qualify for better interest rates and terms

When it's weak or nonexistent, your options shrink fast. You end up paying more, getting less, or getting rejected entirely.

The good news? Most mistakes are fixable. But first, you need to know what they are.

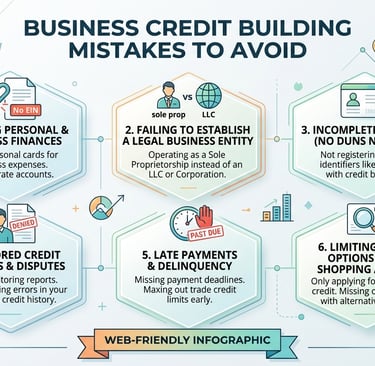

Mistake #1: Not Separating Your Business From Your Personal Finances

This is the most common mistake. And it quietly holds back thousands of small business owners.

If you are using your personal bank account for business expenses, or signing vendor agreements in your own name, you are not building business credit — you are building personal credit. Those are two very different things.

Lenders who review business funding applications look at your EIN (Employer Identification Number) — that's the tax ID your business gets from the IRS, separate from your Social Security Number. They check what's attached to that EIN, not just to you personally.

What to do instead:

Get an EIN from the IRS (it's free and takes about 10 minutes online)

Open a dedicated business checking account in your business name

Register your business as an LLC or corporation — this creates legal separation between you and the business

Use your business address and phone number, not your personal ones

This is the foundation. Without it, the rest of your credit-building work loses value.

Mistake #2: Skipping the Business Credit Basics for Small Business Setup

A lot of business owners try to jump straight to business credit cards or loans before their business is properly set up. Then they wonder why they keep getting denied.

Lenders and business credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business check whether your business looks legitimate. If your business can't be verified easily, your application gets flagged or rejected.

The simple business credit building process starts with:

Registering your business name with your state

Getting a physical business address (not a P.O. box — some lenders reject those)

Setting up a dedicated business phone number listed in 411 directories

Getting a DUNS number from Dun & Bradstreet (free, and important for building a business credit file)

Building a basic business website with your company information

This process takes a few weeks to complete. But once it's done, your business looks real and credible to anyone who checks.

Mistake #3: Ignoring Vendor Trade Lines at the Start

Most new business owners want to go straight to a business credit card or bank loan. That's understandable — but it's skipping an important step.

Trade lines are vendor accounts that report your payment history to business credit bureaus. Think of them as your business's first credit references.

Vendors like Uline, Quill, and Grainger offer what's called net-30 accounts. You order supplies, and you have 30 days to pay. When you pay on time, they report it. That builds your business credit profile early — without a hard credit check on most accounts.

This is especially useful if you're building EIN credit and don't want lenders pulling your personal credit score yet.

Business credit tips for new companies:

Start with 3 to 5 vendor trade line accounts

Pay every invoice before the due date

Give it 60 to 90 days for accounts to report

Check your Dun & Bradstreet and Experian Business reports to confirm they are showing up

Once you have active trade lines reporting, it becomes much easier to qualify for business credit cards and small business loans.

Mistake #4: Applying for Too Much Credit Too Fast

When a business is new and hungry for funding, the temptation is to apply everywhere at once. This is a mistake that can actually damage your credit profile.

Every time you apply for credit, many lenders do what's called a hard inquiry — they pull your credit report, and that pull leaves a mark. Too many inquiries in a short period signals desperation to lenders and can lower your score.

Beyond that, applying for accounts your business isn't ready for almost always results in rejection. And multiple rejections on your record make future applications harder.

What to do instead:

Follow the right sequence: business setup first, then vendor accounts, then secured business credit cards, then unsecured cards and loans

Only apply for credit products that match your current profile

Space out applications — give at least 60 to 90 days between major credit applications

Research approval requirements before applying, not after

Patience here saves you a lot of setbacks.

Mistake #5: Not Monitoring Your Business Credit Reports

Here's something most small business owners don't know: errors on business credit reports are common. And unlike personal credit reports, no one automatically notifies you when something incorrect shows up.

If a vendor reports a late payment incorrectly, or if a judgment ends up on your file by mistake, it stays there until you dispute it. Lenders looking at your profile will see it and may deny your application — without you even knowing why.

Build this habit:

Check your Dun & Bradstreet Paydex score regularly (this is a business credit score from 0 to 100; 80 or higher is considered good)

Review your Experian Business and Equifax Business reports at least quarterly

Dispute any errors directly with the reporting bureau

Keep records of all payments and vendor accounts so you can back up disputes

Monitoring your credit is part of the business credit checklist for new businesses that too many owners skip. Don't make that mistake.

Mistake #6: Using Personal Credit to Cover Business Expenses

This one is easy to fall into, especially in the early months when the business account is tight.

The problem is that mixing personal and business credit creates two issues. First, it can hurt your personal credit score if business expenses push your credit utilization too high. (Credit utilization is how much of your available credit you're using — keeping it under 30% is generally recommended.) Second, it does nothing to build your business credit profile.

Every dollar you spend on a personal card for business purposes is a missed opportunity to build business credit history.

Instead:

Open a secured business credit card as early as possible — many require minimal time in business

Use it for regular, recurring business expenses like software subscriptions or supplies

Pay the balance in full every month

As your credit grows, apply for unsecured business credit cards with higher limits

This is a simple but powerful step in the simple business credit building process that compounds over time.

Mistake #7: Treating Business Credit as a One-Time Task

Business credit is not a box you check once and forget. It's an ongoing profile that grows and changes based on your activity.

Owners who get a few trade lines, open a credit card, and then go quiet often find that their credit profile stagnates — or that inactive accounts get closed, which can actually lower their score.

Lenders want to see recent, consistent activity. Not just old accounts with no movement.

Keep your credit profile active:

Use your business credit cards regularly — even small purchases count

Pay everything on time, every time

Add new trade lines as your business grows

Review your credit strategy every six months

Think of business credit like a garden. You can't plant the seeds and walk away. It needs regular attention to grow.

Your Business Credit Checklist for New Business Owners

If you are just getting started, here's a clear action plan:

Register your business — LLC or corporation, in your state

Get your EIN — from IRS.gov, free of charge

Open a business bank account — separate from all personal accounts

Get a business address and phone number — list them publicly

Register for a DUNS number — through Dun & Bradstreet

Open 3 to 5 vendor trade line accounts — net-30 vendors that report to credit bureaus

Pay every account early or on time — no exceptions

Check your business credit reports — quarterly at minimum

Apply for a secured business credit card — use it and pay it off monthly

Graduate to unsecured credit and small business loans — once your profile is established

This is the same sequence that works for business owners across different industries and business sizes. It's not flashy, but it works.

Frequently Asked Questions

How long does it take to build business credit from scratch? Most business owners start seeing a solid business credit profile within 6 to 12 months of following the right steps. The key is consistency — paying on time and keeping your accounts active throughout that period.

Can I build business credit without using my personal credit? Yes. By setting up your business correctly with an EIN, opening vendor trade line accounts, and using a secured business credit card, you can build EIN credit that is separate from your personal profile. Many vendor accounts don't require a personal credit check at all.

What is a good Paydex score for business funding? A Paydex score of 80 or higher (on a scale of 1 to 100) is generally what lenders and suppliers look for. Scores at this level show that your business consistently pays on time. Scores above 80 can improve your chances of getting better terms and higher credit limits.

How many trade lines do I need before applying for a business loan? Most lenders want to see at least 3 to 5 reporting trade lines before considering your business for a loan. Some lenders may require more. The more verified payment history you have, the stronger your application looks.

Does opening too many business credit accounts hurt my credit? Too many applications in a short period can hurt your score due to hard inquiries. However, having multiple accounts that are well-managed and paid on time will actually strengthen your credit profile over time. The key is spacing out applications and only applying when your business is ready.

What's the fastest business credit building mistake to fix? Separating your personal and business finances. If you haven't done this yet, it's the single most impactful change you can make today. Everything else in business credit building depends on having a properly set up business entity with its own EIN and bank account.

Final Thoughts

Building business credit the right way takes time. But avoiding these common mistakes cuts down the learning curve significantly.

You don't need a perfect credit score or years of business history to start. You need the right foundation, the right steps, and the discipline to follow through.

Most lenders are not looking for perfection. They are looking for a business that shows it can manage money responsibly and pay its debts on time. That's entirely within your reach — regardless of where you are starting from.

If you want help building your business credit the right way or need guidance on accessing funding for your small business, Altopex.com is here to walk you through it step by step. Reach out and let us help you build the financial foundation your business deserves.